In today’s fast-paced world, managing a family budget is essential for financial stability. Learn how to create and effectively stick to a family budget to achieve your financial goals.

Importance of a Family Budget

A family budget is an essential tool for financial stability and success. It allows you to track your income and expenses, ensuring you are spending less than you earn and working towards your financial goals. Here’s why a family budget is so important:

1. Achieve Financial Goals

Whether it’s buying a home, saving for retirement, or taking a dream vacation, a budget helps you allocate money towards your aspirations. By outlining your financial goals and tracking your progress, a budget provides a roadmap to achieve them.

2. Reduce Debt and Stay Out of Debt

A budget helps you identify areas of overspending and make necessary adjustments to live within your means. This conscious spending can significantly reduce the chances of accumulating debt or falling into a cycle of debt.

3. Make Informed Financial Decisions

Having a clear picture of your income and expenses empowers you to make informed decisions about your finances. From major purchases to everyday spending, a budget allows you to evaluate your options and make choices that align with your financial priorities.

4. Prepare for Emergencies

Unexpected events like medical emergencies or job losses can strain your finances. A budget, particularly one with an emergency fund, acts as a safety net during such times, providing financial security and peace of mind.

5. Improve Communication and Reduce Financial Stress

Creating and maintaining a budget encourages open communication about finances within a family. By involving everyone in the process, you foster a shared understanding of financial goals and responsibilities, reducing potential conflicts and stress related to money.

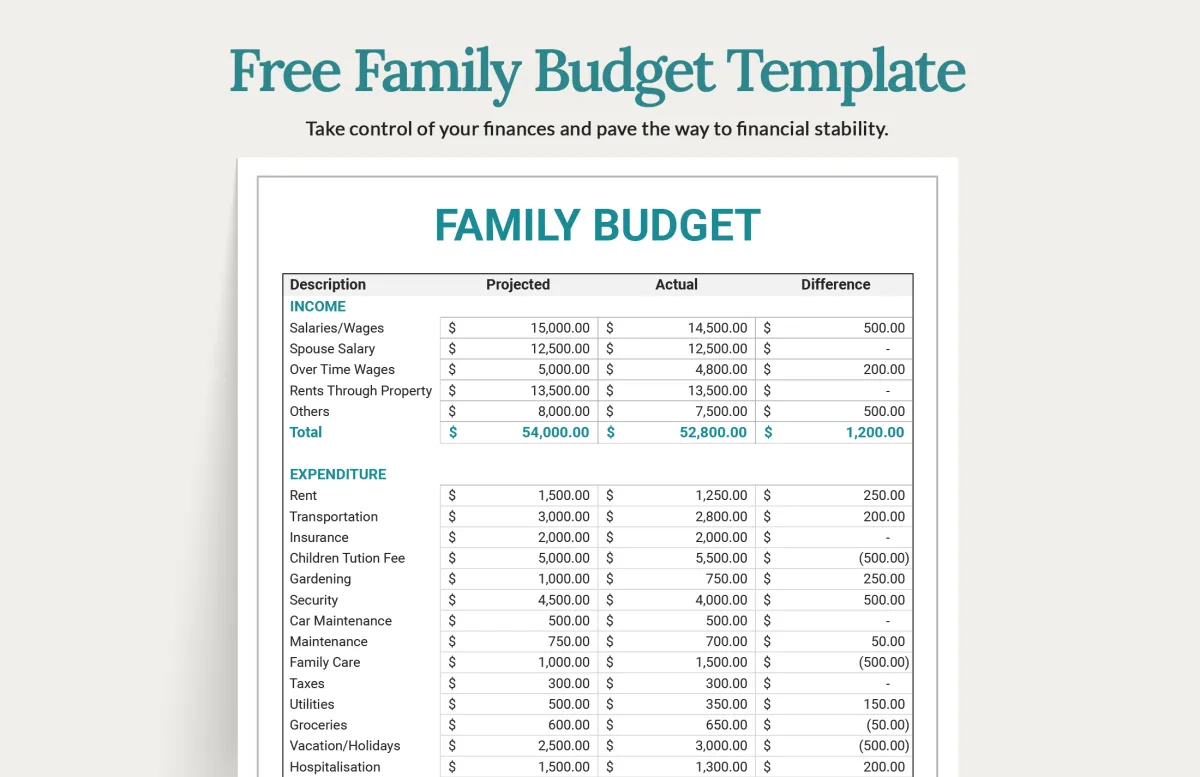

Steps to Create a Family Budget

Creating a family budget is the cornerstone of achieving financial stability and reaching your financial goals. It provides a roadmap for your money, ensuring that your income is allocated effectively to cover essential expenses, build savings, and work towards your aspirations. Here’s a step-by-step guide to help you craft a comprehensive and effective family budget:

1. Track Your Income and Expenses

The first step towards financial control is understanding where your money comes from and where it goes.

- Identify Income Sources: List down all sources of income, including salaries, wages, business income, investments, and any other regular inflows.

- Monitor Expenses: Keep track of every dollar you spend. This can be done using budgeting apps, spreadsheets, or even a simple notebook. Categorize your expenses (e.g., housing, groceries, transportation, entertainment) for a clearer picture.

2. Set Realistic Financial Goals

Having clear financial goals provides direction and motivation for your budget. Determine your short-term, mid-term, and long-term objectives.

- Short-Term: Building an emergency fund, paying off credit card debt, saving for a vacation.

- Mid-Term: Saving for a down payment on a house, funding a child’s education, buying a new car.

- Long-Term: Retirement planning, investing for future financial security.

3. Create a Budget Plan

With a clear understanding of your income, expenses, and goals, you can now create your budget plan. There are several budgeting methods you can use, choose one that resonates with you:

- 50/30/20 Budget: Allocate 50% of your income to needs, 30% to wants, and 20% to savings and debt repayment.

- Zero-Based Budget: Assign a purpose to every dollar of your income, ensuring that your income minus expenses equals zero.

- Envelope System: Divide your cash into envelopes designated for specific categories, limiting your spending to the amount in each envelope.

4. Review and Adjust Regularly

A budget is not a static document; it needs regular review and adjustments to remain relevant and effective. Life is dynamic, and your financial situation can change due to various factors.

- Monthly Reviews: Analyze your income and expenses at the end of each month. Identify areas of overspending and opportunities for savings.

- Life Events: Adjust your budget to accommodate significant life events such as marriage, childbirth, career changes, or relocation.

Tracking Family Expenses

Keeping track of where your money goes is a fundamental part of successful budgeting. Without knowing your spending habits, it’s nearly impossible to identify areas where you can save and redirect funds. Here’s how to get started:

Choose a Tracking Method

Select a tracking method that fits your lifestyle and preferences. The key is to choose a system you’ll use consistently:

- Spreadsheet/Budgeting Apps: Leverage technology with spreadsheets or budgeting apps. Many apps link directly to your bank accounts for automatic transaction updates.

- Notebook and Pen: Go old-school with a dedicated notebook to manually log your expenses. This tactile approach works well for some.

- Envelope System: Allocate cash into designated envelopes for different budget categories. Once an envelope is empty, spending in that category stops.

Record Every Dollar

Make it a habit to track every expense, no matter how small. Even a daily cup of coffee adds up over time. This helps you gain a comprehensive view of your spending patterns.

Categorize Your Expenses

Group similar expenses into categories (e.g., housing, groceries, transportation, entertainment). This allows you to see where the bulk of your money is going and identify potential areas for adjustment.

Review Regularly

Don’t wait until the end of the month to review your expenses. Set aside time weekly or bi-weekly to analyze your spending. This helps you stay on top of your budget and make necessary adjustments in real-time.

Saving for Family Goals

Setting family goals is a great way to get everyone excited and working together towards something special. Whether it’s a dream vacation, a down payment on a home, or saving for your children’s education, having shared financial objectives can bring everyone closer and create lasting memories.

Here are some tips on how to save effectively for your family goals:

1. Define Your Goals Together

Hold a family meeting to discuss what everyone wants to save for. Make sure the goals are specific, measurable, achievable, relevant, and time-bound (SMART). For example, instead of “go on vacation,” aim for “a week-long trip to Disneyland in two years.”

2. Set a Budget, Find Extra Money

Once you know how much you need and by when, incorporate this savings goal into your overall family budget. Look for areas where you can cut back on expenses or find extra income to reach your goals faster.

3. Make Saving Automatic

Treat your savings goals like regular bills. Set up automatic transfers to your savings account each month. This “pay yourself first” approach ensures that saving becomes a priority.

4. Break Down Big Goals

Large goals can feel overwhelming. Divide a big goal like a down payment into smaller, more manageable monthly or weekly savings targets. This makes it easier to track progress and stay motivated.

5. Celebrate Milestones

Acknowledge and celebrate your family’s saving successes along the way! When you reach a significant milestone, find a fun and affordable way to reward yourselves. This helps reinforce positive saving habits.

Tips for Cutting Household Costs

Trimming your household expenses is a surefire way to gain control over your finances. It’s not about deprivation, but making mindful choices that align with your family’s needs and values. Here are some areas to explore:

Groceries:

- Meal planning: Plan your meals for the week and build a shopping list around those meals. This reduces impulse buys and food waste.

- Cook at home: Eating out less often can save a substantial amount of money.

- Embrace leftovers: Repurpose leftovers into new meals to stretch ingredients further.

- Compare prices and shop sales: Check flyers and use coupons strategically.

- Buy in bulk (wisely): Stock up on non-perishable items when they are on sale, but only if you have the space and will use them before they expire.

Entertainment:

- Explore free activities: Take advantage of free community events, parks, and libraries.

- Have family game nights: Instead of expensive outings, enjoy quality time at home.

- Cut cable or streaming services: Consider whether you can reduce the number of subscriptions you have.

Utilities:

- Lower thermostat: Adjusting your thermostat by a few degrees can make a difference in your heating and cooling bills.

- Conserve energy: Turn off lights when you leave a room and unplug electronics when not in use.

- Be water-wise: Take shorter showers and fix any leaky faucets promptly.

Transportation:

- Walk or bike: Opt for active transportation for short trips whenever possible.

- Carpool or use public transportation: Reduce fuel costs and wear and tear on your vehicle.

- Combine errands: Plan your outings strategically to avoid unnecessary driving.

Involving the Whole Family

Creating a family budget isn’t just about crunching numbers—it’s a team effort that works best when everyone participates. Getting your family involved, even the littlest members, fosters a sense of ownership and understanding about money matters. Here’s how to make budgeting a family affair:

Family Budget Meetings

Hold regular family budget meetings to discuss finances. These meetings don’t have to be stuffy or formal. Keep them short, age-appropriate, and even fun!

Age-Appropriate Involvement

Tailor your approach based on your children’s ages:

- Young Children: Introduce basic concepts like needs vs. wants. Use visuals like piggy banks to show how saving works.

- Older Children: Involve them in tracking spending and setting savings goals. Let them help with price comparisons while shopping.

- Teenagers: Give them more responsibility, like managing a portion of their allowance or a part-time job income.

Open Communication

Encourage honest conversations about money. Explain the family’s financial goals and the importance of sticking to the budget. Answer questions openly and age-appropriately.

Compromise and Collaboration

Budgeting often requires making choices. Involve everyone in deciding where to cut back or where to allocate funds. This teaches valuable lessons about prioritization and compromise.

Adjusting the Budget as Needed

Life is unpredictable, and your family budget needs to be flexible enough to roll with the punches. Here’s how to adjust your budget when necessary:

1. Review and Reassess

Regularly review your budget to see how well it’s working. Are you consistently overspending in certain categories? Are your income or expenses different than you anticipated?

2. Identify Areas for Adjustment

Pinpoint areas where you can cut back or reallocate funds. Maybe you can reduce dining out expenses or explore more cost-effective grocery shopping strategies.

3. Prioritize Essential Expenses

When making adjustments, prioritize your needs over your wants. Ensure essential expenses like housing, utilities, food, and debt payments are covered first.

4. Be Realistic and Flexible

Adjustments might require some lifestyle changes. Be prepared to make compromises and find creative solutions to stay within your budget.

5. Embrace Unexpected Expenses

Life throws curveballs. Build an “emergency fund” into your budget to cushion the blow of unexpected expenses like car repairs or medical bills.

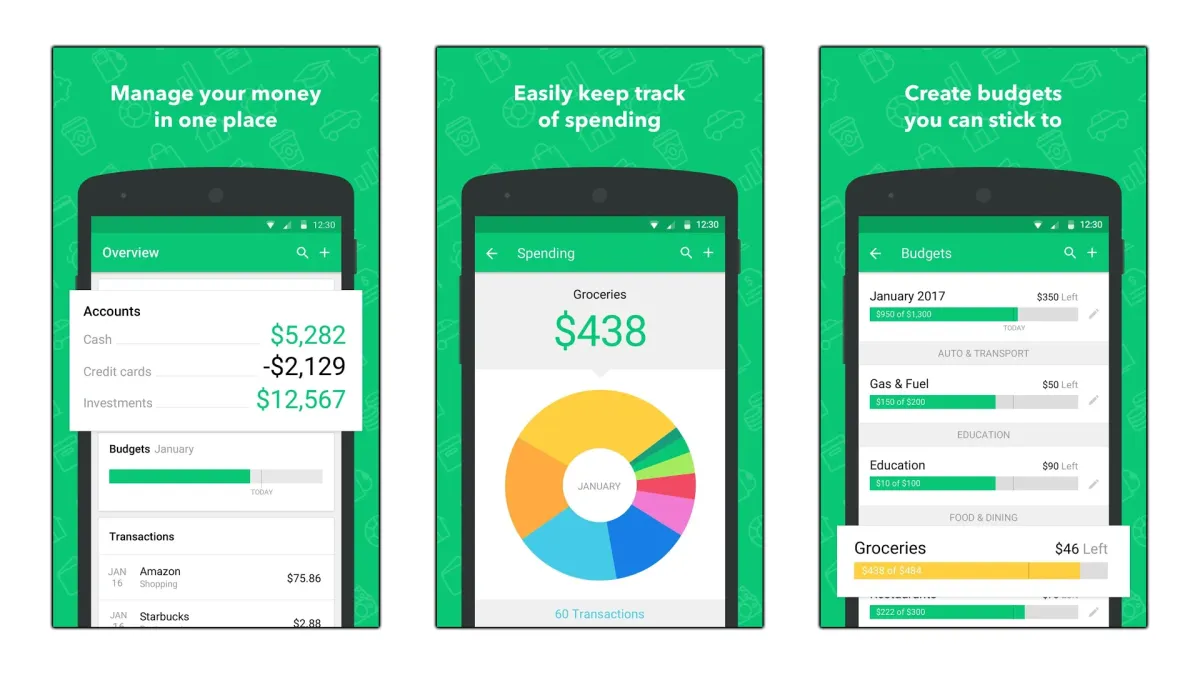

Tools and Apps for Budgeting

Creating a budget is one thing, but sticking to it is another. Thankfully, countless tools and apps can help you track spending, categorize expenses, and stay on top of your financial goals. Here are some popular options:

Budgeting Apps

Budgeting apps offer a convenient way to manage your money on the go. They often connect directly to your bank accounts, allowing for real-time tracking and automatic categorization of expenses. Some popular choices include:

- Mint: A comprehensive app that offers budgeting, bill payment reminders, and credit score tracking.

- YNAB (You Need A Budget): This app follows a unique “envelope budgeting” method, where you allocate every dollar to a specific category.

- Personal Capital: Ideal for those with investments, Personal Capital provides budgeting features alongside investment tracking and analysis.

- EveryDollar: Based on Dave Ramsey’s financial principles, EveryDollar offers a zero-based budgeting approach.

Spreadsheets

For those who prefer a more hands-on approach, spreadsheets are a powerful tool for creating and managing a budget. You can customize them to fit your specific needs and preferences. Templates are readily available online for various budgeting methods.

Envelope System

A classic budgeting method, the envelope system involves allocating cash to specific spending categories in physical envelopes. This tactile approach can help curb overspending by providing a visual reminder of your budget limits.

Other Helpful Tools

- Bill Reminder Apps: These apps help you avoid late fees by sending reminders for upcoming bills.

- Coupon and Deal Websites/Apps: Websites and apps like Groupon, RetailMeNot, and Honey can help you save money on purchases, freeing up more funds within your budget.

The best tool for you will depend on your individual preferences and tech savviness. Experiment with different options to find what works best for your family’s needs.

Conclusion

In conclusion, creating and sticking to a family budget is crucial for financial stability and goal achievement. By prioritizing needs, tracking expenses, and adjusting as necessary, families can achieve financial wellness.

{kind=link}