Building a diversified investment portfolio is essential for minimizing risks and maximizing returns. In this article, we will explore the key strategies and tips on how to create a well-balanced investment portfolio to achieve your financial goals.

What is Diversification?

In the world of investing, diversification is like the old adage, “Don’t put all your eggs in one basket.” It’s a risk management strategy that involves spreading your investments across a variety of assets with the aim of reducing the impact of any single investment performing poorly.

Imagine investing your entire savings in a single company. If that company experiences a downturn, your entire portfolio suffers. However, if you had diversified by investing in a mix of stocks, bonds, and real estate, the poor performance of one company would have a significantly smaller impact on your overall portfolio.

Diversification doesn’t guarantee profits, and it won’t protect you from losses in a downturn. However, it can help to smooth out the ups and downs of the market and potentially improve your long-term returns by reducing your exposure to the poor performance of any single asset.

Benefits of a Diversified Portfolio

A diversified investment portfolio is essential for any investor, regardless of their risk tolerance or investment goals. Diversification involves spreading your investments across a range of asset classes, such as stocks, bonds, and real estate. This strategy helps to mitigate risk and potentially enhance returns over the long term. Here are some key advantages of a diversified portfolio:

1. Reduced Risk

Perhaps the most significant benefit of diversification is its ability to reduce overall portfolio risk. By investing in assets that are not perfectly correlated, meaning they don’t move in the same direction at the same time, you can cushion the impact of losses in any one asset class. For example, if the stock market experiences a downturn, a diversified portfolio with exposure to bonds or real estate may help offset some of those losses.

2. Potential for Enhanced Returns

While diversification is primarily a risk management tool, it can also contribute to potentially higher returns over time. Different asset classes tend to perform well in different economic conditions. By diversifying your investments, you can capture potential gains from various sectors and capitalize on market opportunities as they arise.

3. Reduced Volatility

A well-diversified portfolio can lead to smoother investment returns. When one asset class is experiencing volatility, others may be performing more steadily. This can provide a sense of stability and reduce the emotional impact of market fluctuations.

4. Flexibility and Liquidity

Diversification can also enhance portfolio flexibility and liquidity. By holding a range of assets, you have more options to adjust your portfolio in response to changing market conditions or personal circumstances. Additionally, a diversified portfolio with liquid assets can provide easier access to funds when needed.

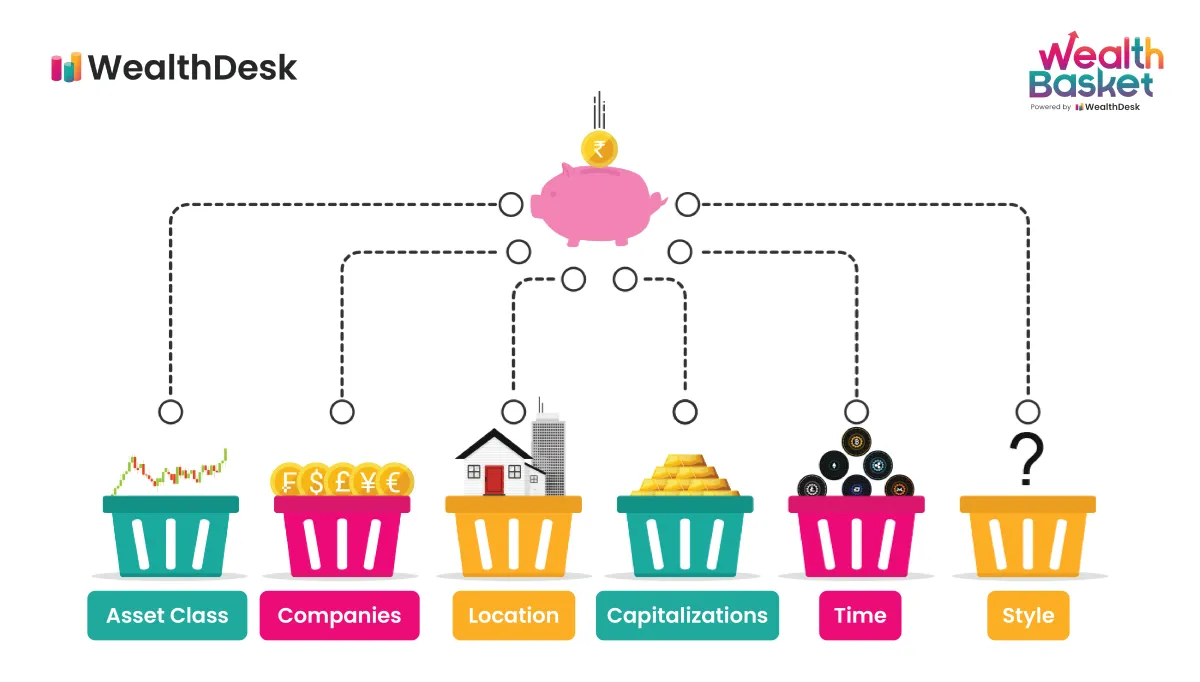

Types of Assets to Include

A diversified investment portfolio should contain a mix of different asset classes, each with its own risk and return characteristics. The goal is to create a balance that minimizes risk while maximizing returns over the long term. Here are some of the most common asset classes to consider:

Stocks

Stocks represent ownership in publicly traded companies. They offer the potential for high returns, but also come with higher risk. Stocks can be further diversified by:

- Market capitalization: Large-cap (large companies), mid-cap, and small-cap.

- Sector: Technology, healthcare, financials, etc.

- Geography: Domestic, international, emerging markets.

Bonds

Bonds are debt securities issued by governments and corporations. They typically offer lower returns than stocks, but also come with lower risk. Bonds can be diversified by:

- Maturity date: Short-term, intermediate-term, long-term.

- Credit quality: Investment-grade, high-yield.

- Issuer: Government, corporate, municipal.

Real Estate

Real estate includes residential, commercial, and industrial properties. It can provide diversification and potential for long-term appreciation, but can also be illiquid.

Commodities

Commodities are raw materials such as oil, gold, and agricultural products. They can provide a hedge against inflation, but prices can be volatile.

Cash and Cash Equivalents

This category includes savings accounts, money market funds, and short-term treasury bills. While they offer low returns, they provide liquidity and stability to the portfolio.

The specific allocation to each asset class will depend on your individual financial goals, risk tolerance, and time horizon. It’s essential to consult with a financial advisor to create a personalized investment strategy.

How to Allocate Your Investments

Allocating your investments is a crucial step in building a diversified portfolio. It involves dividing your capital among different asset classes, such as stocks, bonds, and real estate, based on your financial goals, risk tolerance, and time horizon. Here’s a breakdown of key considerations:

1. Determine Your Risk Tolerance

Your risk tolerance refers to your ability to withstand fluctuations in the value of your investments. Consider factors such as your age, income stability, and investment goals. Younger investors with a longer time horizon may be more comfortable with higher-risk investments, while older investors approaching retirement may prefer more conservative options.

2. Consider Your Time Horizon

Your time horizon is the length of time you plan to invest your money. Longer time horizons allow for greater risk-taking as you have more time to recover from potential market downturns. Conversely, shorter time horizons may necessitate a more conservative approach.

3. Understand Asset Allocation Strategies

Several asset allocation strategies can guide your investment decisions. Some common ones include:

- Rule of 100: Subtract your age from 100 to determine the percentage of your portfolio to allocate to stocks. The remaining portion goes to bonds.

- 60/40 Portfolio: This classic strategy allocates 60% to stocks and 40% to bonds, aiming for a balance between growth and stability.

- Target-Date Funds: These funds automatically adjust their asset allocation as you approach your target retirement date, becoming more conservative over time.

4. Rebalance Regularly

Over time, your portfolio’s asset allocation may drift from its original target due to market fluctuations. Rebalancing involves selling assets that have performed well and buying assets that have underperformed to restore your desired allocation. This helps manage risk and maintain your investment strategy over the long term.

5. Seek Professional Advice

Consider consulting with a qualified financial advisor who can help you determine your risk tolerance, set appropriate investment goals, and create a personalized asset allocation strategy tailored to your specific needs and circumstances.

Risk Management Strategies

Building a diversified portfolio isn’t just about spreading your investments across different asset classes. It’s also about actively managing the inherent risks associated with investing. Here’s how to incorporate risk management into your diversification strategy:

1. Understand Your Risk Tolerance

Before you invest a single dollar, determine how much risk you’re comfortable taking. This involves understanding your financial goals, time horizon, and emotional capacity to handle market fluctuations. Are you investing for retirement in 20 years? You might tolerate higher risk. Need the money in a year? Your risk tolerance is likely much lower.

2. Set Stop-Loss Orders

Consider setting stop-loss orders, which are instructions to automatically sell a security when it hits a certain price. This can help limit your potential losses, though it’s not foolproof (rapid market drops might execute the sale at a much lower price than you set).

3. Regular Portfolio Rebalancing

Over time, some assets in your portfolio will outperform others. This can create an imbalance and expose you to more risk than you initially planned. Regularly rebalancing involves selling a portion of your winning investments and reinvesting in underperforming areas to maintain your desired asset allocation.

4. Diversification Beyond Asset Classes

Don’t stop at just stocks and bonds. Explore diversification within asset classes:

- Stocks: Invest across different sectors (technology, healthcare, energy) and market capitalizations (large-cap, small-cap).

- Bonds: Consider varying maturities (short-term, long-term) and credit qualities (government, corporate).

- Alternatives: Look into real estate, commodities, or precious metals to further diversify.

5. Stay Informed and Seek Advice

Markets are constantly evolving. Stay informed about economic trends, geopolitical events, and industry news that could impact your investments. When in doubt, consulting with a qualified financial advisor can provide personalized guidance tailored to your risk tolerance and financial goals.

Regularly Rebalancing Your Portfolio

Rebalancing is the process of realigning the asset weightings of your investment portfolio. As asset classes perform differently over time—some growing faster than others—your initial strategic asset allocation will drift. This can increase your exposure to risk, as investments performing well begin to represent a larger percentage of your holdings. Rebalancing involves buying or selling assets to restore your portfolio to its target asset allocation.

How often should you rebalance? There’s no magic number, but a common approach is to rebalance your portfolio annually or semi-annually. Alternatively, you can rebalance whenever your asset allocation deviates significantly from your target (e.g., a 5% or 10% drift).

Benefits of Rebalancing:

- Maintains your risk profile: Rebalancing ensures your portfolio’s risk level remains aligned with your investment goals and risk tolerance.

- Enhances long-term returns: While not guaranteed, historically, rebalancing has been shown to potentially improve returns over the long run by forcing you to “buy low and sell high.”

- Instills discipline: Regular rebalancing encourages a disciplined approach to investing, helping you avoid making emotional decisions based on market fluctuations.

Monitoring Your Investments

Building a diversified investment portfolio is a crucial first step towards achieving your financial goals. However, it’s not a “set it and forget it” kind of task. Regular monitoring of your investments is essential to ensure they continue to align with your risk tolerance, time horizon, and overall financial objectives.

Here’s what monitoring your investments entails:

1. Tracking Performance

Keep a close eye on how your investments are performing. This doesn’t mean checking your portfolio obsessively every day. Instead, aim for a regular review, perhaps monthly or quarterly. Track the returns of individual investments and compare them against relevant benchmarks. Are your investments performing as expected? Are certain asset classes outperforming or underperforming others?

2. Rebalancing Your Portfolio

Over time, your portfolio’s asset allocation will drift from your original target. Market fluctuations can cause some assets to grow faster than others, skewing your intended risk profile. Rebalancing involves selling a portion of overperforming assets and buying more of underperforming ones to bring your portfolio back to its target allocation. This disciplined approach helps manage risk and maintain your desired investment strategy.

3. Evaluating Your Investment Strategy

Monitoring provides an opportunity to assess the effectiveness of your investment strategy. Are you on track to reach your financial goals? Do you need to adjust your target asset allocation based on your changing circumstances or risk tolerance? Don’t be afraid to make adjustments if your current strategy isn’t delivering the desired results, but always base changes on careful analysis and consideration.

4. Staying Informed

The financial markets are constantly evolving. Stay informed about economic trends, geopolitical events, and industry news that could impact your investments. Knowledge empowers you to make more informed decisions about your portfolio.

Common Diversification Mistakes

Building a diversified investment portfolio is crucial for managing risk and maximizing returns. However, many investors make common mistakes that can hinder their diversification efforts. Here are some pitfalls to avoid:

1. Over-concentration in a Single Sector or Asset Class

One of the most common mistakes is investing too heavily in a particular sector or asset class. While it might be tempting to put all your eggs in one basket, especially if that sector is performing well, this approach exposes you to significant risk if the sector experiences a downturn.

2. Confusing Familiarity with Diversification

Many investors gravitate towards companies or industries they are familiar with. While it’s natural to feel more comfortable investing in what you know, this can lead to unintentional concentration in certain areas of the market. True diversification involves venturing outside of your comfort zone.

3. Ignoring International Markets

Limiting your investments to your home country can hinder your diversification efforts. International markets offer exposure to different economic conditions, currencies, and growth opportunities. Ignoring them can mean missing out on potential gains.

4. Insufficient Diversification within Asset Classes

Diversification isn’t just about investing in different asset classes like stocks and bonds; it also involves diversifying within those classes. For example, owning stock in five different tech companies doesn’t provide sufficient diversification within the technology sector.

5. Trying to Time the Market

Trying to predict market movements and time your investments can be detrimental to your diversification strategy. Market timing is notoriously difficult, and even seasoned investors struggle to get it right consistently.

6. Neglecting to Rebalance Regularly

As investments perform differently over time, your portfolio’s asset allocation can drift from its original target. Regularly rebalancing your portfolio involves selling investments that have grown proportionally larger and reinvesting in underperforming assets to maintain your desired asset allocation.

Conclusion

In conclusion, building a diversified investment portfolio is essential for managing risk and maximizing returns in the long term.

{kind=link}