Planning for retirement can be overwhelming, but with the right strategy tailored to your goals and lifestyle, you can create a personalized retirement plan that ensures financial security and peace of mind. Learn how to create a plan that works for you.

Importance of Retirement Planning

Retirement planning is not just about accumulating a large sum of money. It’s about designing a future where you can live comfortably, pursue your passions, and enjoy financial freedom without relying solely on a paycheck. Here’s why prioritizing retirement planning is crucial:

Financial Security

Retirement planning provides a financial safety net, ensuring you have the resources to cover your expenses when your regular income ceases. This includes essential needs like housing, healthcare, food, and transportation, as well as discretionary spending for travel, hobbies, or supporting loved ones.

Inflation Protection

Inflation erodes the purchasing power of money over time. What you can buy today with a certain amount will likely cost more in the future. Retirement planning helps you stay ahead of inflation by growing your savings at a rate that outpaces the rising cost of living.

Healthcare Costs

Healthcare expenses tend to increase as we age. Planning for retirement means factoring in potential long-term care costs, medical bills, and insurance premiums. A well-structured plan helps you prepare for these expenses and avoids depleting your savings due to unexpected health issues.

Pursuing Your Passions

Retirement should be a time to enjoy the fruits of your labor. Whether it’s traveling the world, starting a business, volunteering, or simply spending more time with family, retirement planning gives you the financial freedom to pursue your passions without financial constraints.

Peace of Mind

Perhaps the most significant benefit of retirement planning is the peace of mind it provides. Knowing you have a solid plan in place alleviates financial stress and allows you to approach your later years with confidence and excitement.

Setting Retirement Goals

Retirement planning isn’t just about saving money. It starts with a vision of what you want your retirement to look like. Do you dream of traveling the world, pursuing a new hobby, or simply enjoying leisurely days at home? Defining your retirement goals is the first step in creating a plan that’s tailored to your aspirations.

Here’s how to set effective retirement goals:

1. Think About Your Ideal Lifestyle

Imagine your perfect day in retirement. Where are you? What are you doing? Who are you with? Be as specific as possible. This vision will help you determine how much money you need to support your desired lifestyle.

2. Consider Your Timeline

When do you want to retire? Your retirement age will influence how much you need to save each month and what type of investments you choose. A longer time horizon allows for more aggressive investment strategies.

3. Factor in Healthcare Costs

Healthcare expenses tend to rise with age. Research potential healthcare costs in retirement and factor these into your savings goals. Consider long-term care insurance as part of your plan.

4. Address Housing

Where do you plan to live in retirement? Will you stay in your current home, downsize, or relocate? Understanding your housing plans will have a significant impact on your retirement budget.

5. Quantify Your Goals

Once you have a clear picture of your retirement vision, assign a monetary value to your goals. This will give you a target savings number to work towards.

Estimating Retirement Expenses

Retirement planning is incomplete without a firm grasp on your expected expenses. While it’s impossible to predict the future perfectly, a realistic estimate of your retirement spending is crucial. This projection will guide your savings goals, investment strategies, and ultimately, your retirement lifestyle.

To estimate your retirement expenses, consider these factors:

1. Current Spending Habits:

Start by analyzing your current spending. Review bank statements, credit card bills, and budgeting spreadsheets to understand where your money goes. This forms the foundation of your retirement budget, but remember, your spending habits may change.

2. Housing:

Will you stay in your current home, downsize, or relocate? Factor in potential costs like mortgage payments, rent, property taxes, insurance, maintenance, and potential renovations.

3. Healthcare:

Healthcare costs tend to rise with age. Factor in health insurance premiums, potential out-of-pocket expenses, and long-term care possibilities. Explore Medicare options and supplemental insurance plans.

4. Lifestyle Choices:

How do you envision your retirement? Will you travel extensively, pursue hobbies, or spend more time with loved ones? Factor these aspirations into your budget. Be realistic – extravagant travel plans might require significant savings.

5. Inflation:

The purchasing power of money diminishes over time due to inflation. What costs $100 today might cost significantly more in 10 or 20 years. Factor in an average annual inflation rate when estimating future expenses.

6. Debt:

Ideally, aim to enter retirement with minimal debt. If you have outstanding loans, include those payments in your budget. High-interest debt can eat into your retirement savings, so prioritize reducing it beforehand.

7. Unexpected Expenses:

Life throws curveballs. A realistic retirement budget should include a cushion for unexpected expenses, such as home repairs, medical emergencies, or supporting family members.

By carefully considering these factors, you can create a retirement expense estimate that aligns with your individual circumstances and aspirations. Remember, this is not a one-time exercise – revisit and adjust your estimates periodically as your plans and circumstances evolve.

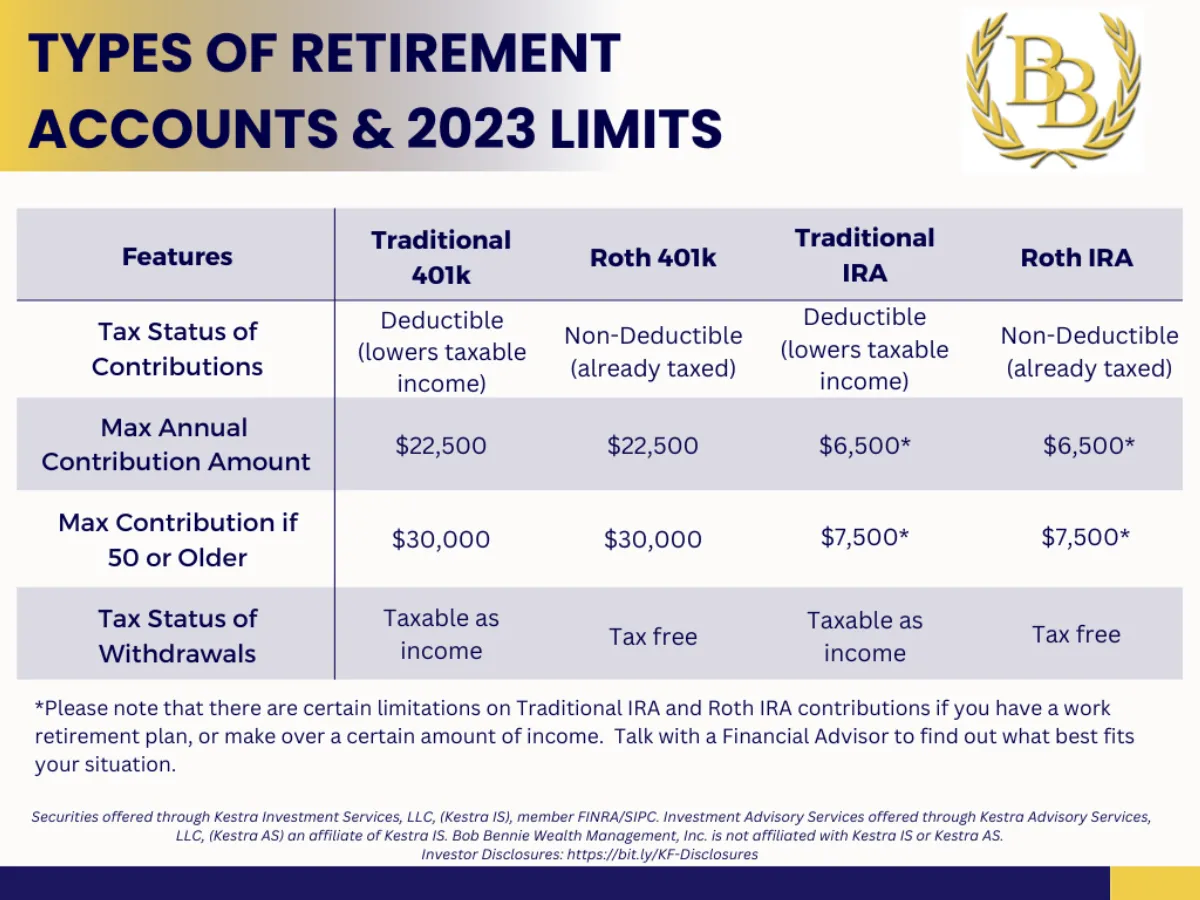

Choosing Retirement Accounts

One of the most important steps in creating your retirement plan is choosing the right accounts to house your savings. The best type of account for you will depend on your individual circumstances, such as your employment status, risk tolerance, and retirement goals.

Common Retirement Account Options:

- Employer-Sponsored Plans: If your employer offers a 401(k) or 403(b) plan, this is often a great place to start. These plans allow you to contribute pre-tax income, which lowers your taxable income. Often, employers will match your contributions up to a certain percentage, which is essentially free money.

- Individual Retirement Accounts (IRAs): IRAs are available to anyone, regardless of employment status. There are two main types of IRAs: Traditional and Roth. Traditional IRAs offer tax-deductible contributions, while Roth IRAs offer tax-free withdrawals in retirement.

- Self-Employed Plans: If you’re self-employed or own a small business, options like SEP IRAs and Solo 401(k)s offer higher contribution limits and tax advantages tailored to your needs.

Factors to Consider:

- Contribution Limits: Each type of retirement account has annual contribution limits set by the IRS. Make sure you understand these limits to maximize your savings.

- Tax Benefits: Consider whether you prefer tax deductions now (Traditional 401(k), Traditional IRA) or tax-free withdrawals in retirement (Roth 401(k), Roth IRA).

- Investment Options: Explore the investment funds and options available within each account type. Some plans offer more diverse investment options than others.

- Fees: Pay close attention to administrative fees, investment fees, and any other charges associated with each account. These fees can eat into your returns over time.

It’s crucial to carefully research and compare different retirement account options. Consulting with a qualified financial advisor can provide personalized guidance based on your specific financial situation and retirement objectives.

Investment Strategies for Retirement

Investing is a critical component of retirement planning. It allows you to grow your savings over time and outpace inflation. However, choosing the right investment strategies can feel daunting. Here’s a breakdown of key considerations:

1. Time Horizon:

Your time horizon, or the length of time until you retire, significantly influences your investment approach.

- Longer Time Horizon (20+ Years): A longer time horizon allows you to take on more risk. You can consider a more significant allocation to growth-oriented investments like stocks, which have historically delivered higher returns over the long term.

- Shorter Time Horizon (5-10 Years): As you approach retirement, preserving your capital becomes paramount. Shifting towards a more conservative portfolio with a higher allocation to bonds and fixed-income securities can help mitigate potential losses as you near your retirement date.

2. Risk Tolerance:

Understanding your risk tolerance is crucial. How comfortable are you with the potential for your investments to fluctuate in value?

- High Risk Tolerance: You’re comfortable with market volatility and the potential for higher returns, even if it means accepting the possibility of short-term losses.

- Moderate Risk Tolerance: You seek a balance between growth and preserving your capital. A diversified portfolio combining stocks and bonds is often suitable.

- Low Risk Tolerance: You prioritize the safety of your investments over potential for high returns. Fixed-income securities, money market accounts, and other lower-risk options may be more appropriate.

3. Diversification:

“Don’t put all your eggs in one basket.” Diversifying your investments across different asset classes is essential to manage risk. This can involve investing in:

- Stocks: Represent ownership in publicly traded companies and offer potential for growth.

- Bonds: Debt securities that typically offer more stability than stocks and provide regular interest payments.

- Real Estate: Can offer rental income and potential for appreciation.

- Commodities: Raw materials like gold, oil, or agricultural products, which can provide a hedge against inflation.

4. Retirement Accounts:

Take advantage of tax-advantaged retirement accounts:

- 401(k) or 403(b): Employer-sponsored plans that offer tax benefits and potential employer matching contributions.

- Traditional IRA: Contributions may be tax-deductible, and earnings grow tax-deferred until retirement.

- Roth IRA: Contributions are made with after-tax dollars, but withdrawals in retirement are tax-free.

5. Regular Review and Rebalancing:

It’s essential to review your retirement portfolio periodically, at least annually. As your time horizon and market conditions change, your asset allocation may need adjustment to stay aligned with your goals.

Social Security and Pensions

Social Security and pensions can form a significant portion of your retirement income. Understanding how these systems work and when to tap into them is crucial for maximizing your benefits.

Social Security: This federal program provides retirement, disability, and survivor benefits based on your work history and earnings. You become eligible to start receiving benefits as early as age 62, but your benefits will be higher if you wait until your full retirement age (FRA), which varies depending on your birth year. Delaying benefits past your FRA can further increase your monthly payout.

Pensions: Traditional pensions, also known as defined benefit plans, are less common now but still offered by some employers. If you’ve participated in a pension plan, you’ll receive a guaranteed income stream in retirement, typically calculated based on your salary and years of service. It’s important to understand the vesting rules and payout options associated with your specific plan.

Healthcare Costs in Retirement

One of the most significant expenses you’ll face in retirement is healthcare. While Medicare will cover a portion of your costs, it doesn’t cover everything. You’ll be responsible for deductibles, copayments, and some services not covered by Medicare.

Factor in the potential costs of:

- Medicare premiums

- Supplemental health insurance (Medigap)

- Prescription drug coverage (Part D)

- Long-term care, which is generally not covered by Medicare

These costs can add up quickly, so it’s crucial to factor them into your retirement budget. Consider setting aside funds specifically for healthcare expenses, such as a health savings account (HSA) if you’re eligible.

Reviewing and Adjusting Your Plan

Creating a retirement plan is not a “set it and forget it” endeavor. Life is fluid, and your financial needs and goals will likely evolve over time. That’s why it’s crucial to regularly review and adjust your retirement plan. Here’s how:

Frequency of Review

Aim to review your plan at least annually. Additionally, consider revisiting it after major life events like:

- Marriage or divorce

- Birth or adoption of a child

- Job changes or promotions

- Receiving an inheritance or significant financial windfall

- Major health changes for you or a loved one

Key Areas to Assess:

- Savings Rate: Is your current savings rate still sufficient to reach your retirement goals? If you received a raise or bonus, can you increase your contributions?

- Investment Performance: Review your portfolio’s performance. Are your investments aligned with your risk tolerance? Do you need to rebalance your asset allocation?

- Retirement Timeline: Has your desired retirement age changed? Adjust your savings and investment strategies accordingly.

- Expenses: Have your anticipated retirement expenses increased or decreased? Factor in healthcare costs, travel plans, and potential lifestyle changes.

- Withdrawal Strategy: Once you’re nearing retirement, carefully consider how you’ll draw income from your savings.

Seeking Professional Guidance

Consider consulting with a qualified financial advisor to gain personalized advice and guidance on your retirement plan. They can help you navigate complex financial decisions and ensure your plan is still on track to meet your needs.

Conclusion

In conclusion, crafting a personalized retirement plan involves meticulous financial planning, considering individual goals, lifestyle, and risk tolerance. Regularly reviewing and adjusting the plan ensures its effectiveness in securing a comfortable retirement.

{kind=link}