Looking to achieve financial freedom? Discover effective strategies for paying off your mortgage early and saving on interest with our comprehensive guide.

Benefits of Paying Off Your Mortgage Early

Paying off your mortgage early can provide significant financial and personal benefits. While it requires discipline and often some sacrifices, the rewards can be substantial. Here are some key advantages:

1. Massive Interest Savings

This is arguably the most significant benefit. When you pay off your mortgage early, you save thousands, potentially tens of thousands, of dollars in interest payments. By making even small extra payments over the life of your loan, you reduce the principal balance faster, which significantly reduces the amount of interest accrued.

2. Increased Financial Freedom

Imagine a life without monthly mortgage payments! This freedom allows you to allocate those funds towards other financial goals, such as:

- Investing and building wealth

- Saving for retirement

- Funding your children’s education

- Pursuing your passions and hobbies

3. Reduced Financial Stress

Owning your home outright provides peace of mind and reduces financial anxiety. You’ll no longer have the burden of a large monthly payment hanging over your head, especially during times of economic uncertainty or job loss.

4. Improved Credit Score

While paying off your mortgage early doesn’t directly boost your credit score, it can indirectly contribute to a positive credit history. By demonstrating responsible financial behavior and reducing your debt-to-income ratio, you enhance your creditworthiness for future loans.

5. Home Equity Advantage

Paying down your mortgage faster builds equity in your home more quickly. This can be beneficial if you decide to sell your home or refinance in the future, as you’ll have more equity to leverage.

How to Create a Repayment Plan

Creating a strategic repayment plan is crucial for successfully paying off your mortgage early. Here’s a step-by-step guide to help you develop an effective plan:

1. Assess Your Financial Situation:

Start by analyzing your income, expenses, debts, and savings. Determine how much extra money you can realistically allocate towards mortgage payments each month.

2. Set Realistic Goals:

Decide on a timeframe for paying off your mortgage early. Consider factors like your financial capacity, risk tolerance, and other financial goals. It’s important to set achievable goals that align with your overall financial well-being.

3. Explore Repayment Options:

Research different mortgage repayment strategies, such as:

- Bi-weekly payments: Switching to bi-weekly payments can help you make one extra monthly payment each year, accelerating the principal reduction process.

- Increased monthly payments: Gradually increase your monthly mortgage payments as your income grows or expenses decrease.

- Lump-sum payments: Make occasional lump-sum payments towards your principal whenever you receive extra funds, such as bonuses, tax refunds, or inheritance.

4. Choose a Suitable Strategy:

Based on your financial situation and goals, select the repayment strategy or a combination of strategies that best suits your needs. Consider factors like your comfort level with different payment frequencies and your ability to make additional payments.

5. Review and Adjust Regularly:

Periodically review your repayment plan to ensure it aligns with your current financial circumstances and goals. Life events and financial changes may require adjustments to your plan over time.

Tips for Reducing Interest Costs

Paying off your mortgage early is a fantastic way to save thousands of dollars in interest and build equity faster. Here are some effective strategies to reduce the overall interest you’ll pay on your loan:

1. Make Extra Payments Strategically

Even small extra payments can make a big difference over the life of your loan. Consider these approaches:

- Bi-weekly payments: Switching to bi-weekly payments means you make half your mortgage payment every two weeks, resulting in one extra payment per year.

- Additional principal payments: Whenever you have extra cash, consider making an additional payment directly towards your loan principal.

- Lump-sum payments: If you receive a bonus, tax refund, or inheritance, putting a portion towards your mortgage principal can significantly reduce your interest payments over time.

2. Explore Refinancing Options

Refinancing your mortgage might save you money if you can secure a lower interest rate. It’s especially beneficial if:

- Interest rates have dropped: Monitor interest rate trends and consider refinancing if you can get a lower rate.

- Your credit score has improved: A better credit score can qualify you for lower interest rates.

3. Consider a Shorter Loan Term

While your monthly payments might be higher, opting for a shorter loan term (like 15 years instead of 30) means you pay significantly less interest over the life of the loan.

4. Make Home Improvements That Increase Value

Investing in home improvements that increase your property value could allow you to refinance in the future for a lower interest rate or shorter term, ultimately reducing your interest costs.

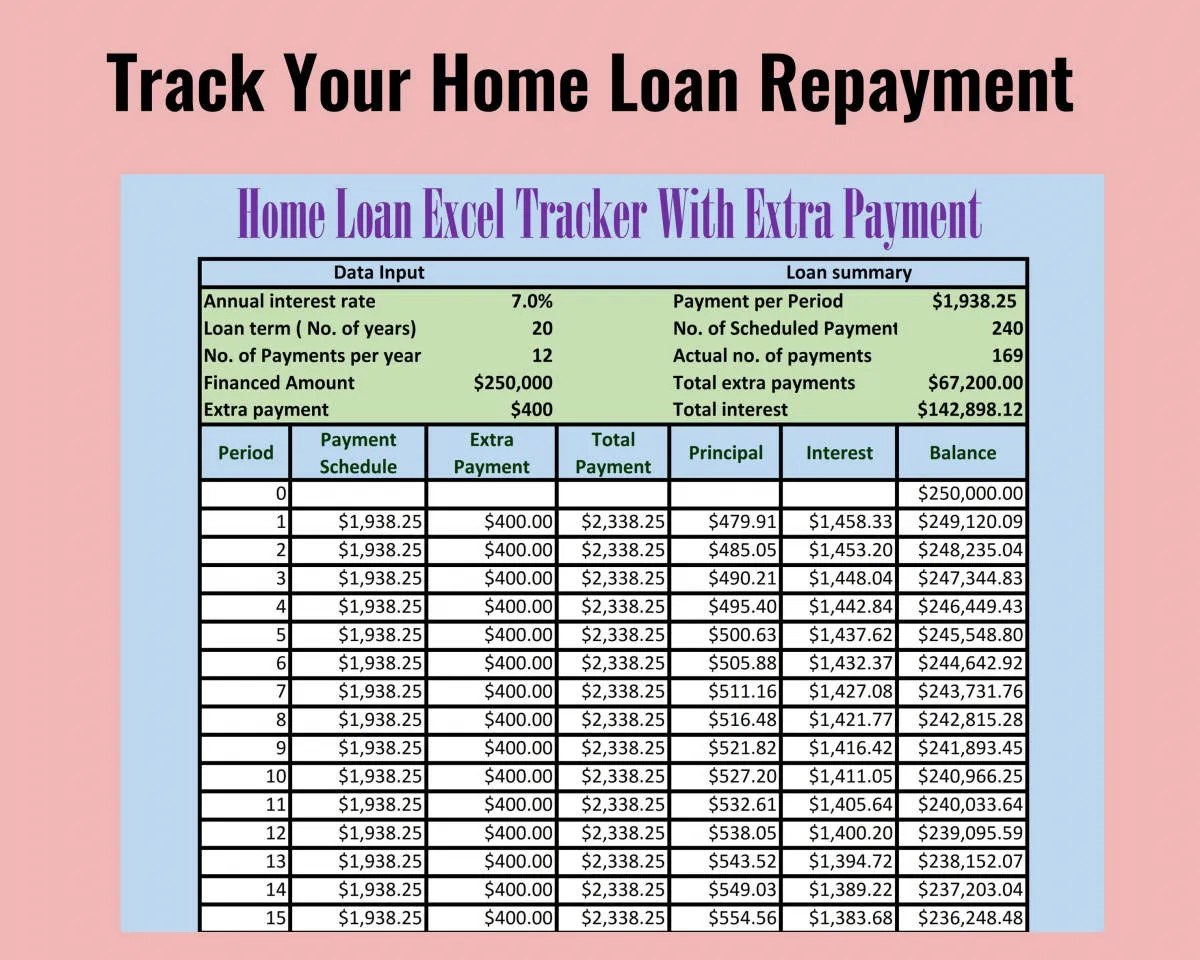

Making Extra Payments

One of the most effective strategies for paying off your mortgage early is making extra payments. This might seem daunting, but even small additional amounts can make a significant difference in the long run. Let’s explore different ways you can achieve this:

Bi-Weekly Payments

Instead of making one large payment every month, consider switching to bi-weekly payments. By dividing your monthly payment in half and paying every two weeks, you essentially make an extra full monthly payment each year. This strategy can shave off years from your loan term and save thousands in interest.

Adding a Little Extra

You don’t need a windfall to make a dent in your principal. Consider adding a small amount, such as $50 or $100, to each mortgage payment. Over time, this consistent extra payment will add up and significantly reduce the life of your loan.

Utilizing Windfalls

When you receive unexpected income, such as tax refunds, work bonuses, or inheritance, consider putting a portion, or even all of it, towards your mortgage principal. These lump sum payments can drastically reduce your loan balance and save years of interest payments.

Rounding Up Payments

Round up your mortgage payments to the nearest $50 or $100. This simple trick can add up to a significant extra payment over the life of your loan.

Important Note: Before making extra payments, verify with your lender to ensure they are applied directly to the principal balance and that there are no prepayment penalties associated with your mortgage.

Refinancing Your Mortgage

Refinancing your mortgage involves replacing your existing mortgage with a new one, potentially with different terms and a lower interest rate. This can be a powerful strategy for paying off your mortgage early if done strategically.

Benefits of Refinancing for Early Mortgage Payoff

- Lower interest rate: Securing a lower interest rate reduces the overall interest you’ll pay over the life of the loan, freeing up more money to put towards the principal.

- Shorter loan term: Refinancing to a shorter loan term, such as going from a 30-year to a 15-year mortgage, can help you pay off your mortgage faster, albeit with higher monthly payments.

Factors to Consider When Refinancing

- Closing costs: Refinancing comes with closing costs, similar to your original mortgage. Ensure the potential savings from refinancing outweigh these costs.

- Credit score: A higher credit score can qualify you for lower interest rates, making refinancing more beneficial.

- Current interest rate environment: Monitor interest rate trends to determine if refinancing is financially advantageous.

- Break-even point: Calculate how long it will take for the savings from refinancing to exceed the closing costs. This is your break-even point.

Using Windfalls to Pay Down Debt

Windfalls are unexpected financial gains that can come from various sources, such as:

- Tax refunds

- Work bonuses

- Inheritances

- Lottery winnings

- Gifts

While it’s tempting to splurge on a vacation or a new car, using windfalls to pay down your mortgage early can save you thousands of dollars in interest and help you own your home sooner.

Here are some ways to use windfalls to pay down your mortgage:

- Make an extra mortgage payment. Even a small windfall can make a big difference when applied directly to your mortgage principal.

- Make a lump-sum payment. If you receive a significant windfall, consider putting it towards a lump-sum payment on your mortgage principal. This can drastically reduce the length of your loan term and save you substantial interest payments.

- Set up a dedicated savings account. If your windfall isn’t large enough for a significant lump-sum payment, consider depositing it into a high-yield savings account specifically earmarked for future extra mortgage payments.

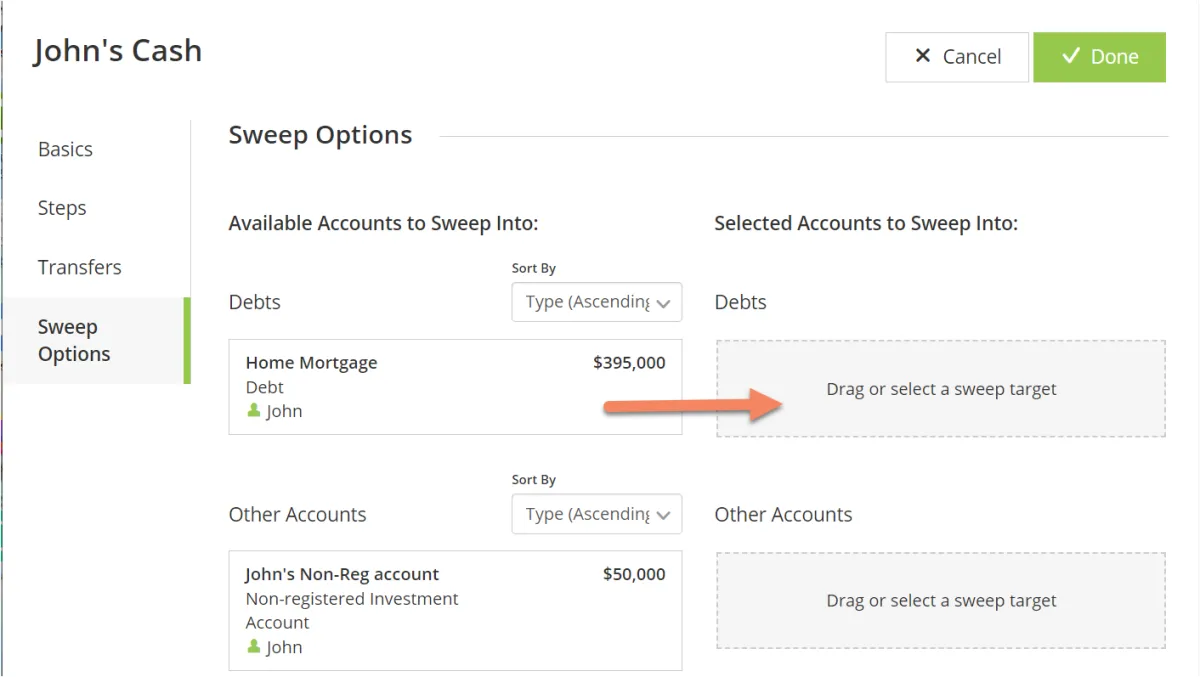

Managing Other Debts Simultaneously

While focusing on mortgage payoff is admirable, don’t neglect other debts. High-interest credit card balances or loans can derail your progress.

Prioritize and strategize:

- List all debts: Include balances and interest rates.

- High-interest first: Prioritize paying down debts with the highest interest rates. This minimizes the overall interest you accrue.

- Minimum payments: While tackling high-interest debt, ensure you make minimum payments on other debts to avoid penalties.

- Consider balance transfer: Explore options like balance transfer cards with lower introductory interest rates to consolidate and pay off credit card debt faster.

Staying Motivated to Reach Your Goal

Paying off your mortgage early is a fantastic goal, but it requires dedication and consistency over a long period. There will be times when your motivation wanes. Here are some tips for staying motivated:

1. Visualize Your Goal

Imagine the feeling of being mortgage-free. Picture yourself free from that monthly payment, having more financial freedom, and potentially retiring earlier. Visualizing the end result can reignite your drive.

2. Track Your Progress and Celebrate Milestones

Create a visual representation of your mortgage payoff, like a thermometer you fill in, or a graph that shows your principal decreasing. Seeing the progress you’re making is incredibly motivating. Celebrate milestones along the way, like paying off a significant chunk of the principal or reaching the halfway point.

3. Find an Accountability Partner

Share your goal with a trusted friend, family member, or financial advisor. Having someone to check in with and hold you accountable can make a significant difference. Consider finding someone with a similar goal, like paying off debt, for mutual support.

4. Remind Yourself of the “Why”

Write down the reasons why paying off your mortgage early is important to you. Is it for financial freedom, early retirement, or less stress? When you hit a motivational slump, revisit your “why” to remind yourself of the bigger picture.

5. Break Down the Goal into Smaller Steps

Looking at the total amount you need to pay off can be overwhelming. Instead, break down your goal into smaller, more manageable steps. Focus on paying an extra $100 a month, then increase it as you feel more comfortable. Each small victory will fuel your motivation.

Conclusion

In conclusion, implementing smart financial strategies and increasing mortgage payments can help accelerate paying off your mortgage early, saving you significant interest costs in the long run.

{kind=link}