Are you in your 20s and looking to take control of your finances? Learn how to create a personalized personal finance plan tailored to your goals and lifestyle in this comprehensive guide.

Importance of Financial Planning in Your 20s

Your 20s are a time of significant change and growth, both personally and financially. It’s the decade where you start building the foundation for your financial future. While it might seem too early to think about retirement or investments, creating a financial plan in your 20s is crucial for a number of reasons:

Early Bird Gets the Worm: The Power of Compounding

One of the most compelling reasons to start financial planning in your 20s is to harness the power of compounding. Compounding is the snowball effect of earning interest on your interest. The earlier you start investing, even small amounts, the more time your money has to grow exponentially. This early start can make a significant difference in the long run, potentially leading to a larger nest egg for retirement.

Establishing a Strong Financial Foundation

Financial planning in your 20s helps you establish a strong financial foundation for your future. By creating a budget, tracking your expenses, and setting financial goals, you gain control over your money. This control allows you to make informed decisions about spending, saving, and investing, putting you on a path towards financial stability and security.

Managing Financial Responsibilities

As you navigate your 20s, you’re likely to encounter increasing financial responsibilities. Whether it’s student loan repayments, rent payments, or saving for a down payment on a house, having a financial plan in place provides a roadmap to manage these responsibilities effectively. It helps you prioritize spending, avoid unnecessary debt, and work towards achieving your financial goals.

Building Healthy Financial Habits

Perhaps the most important reason to embrace financial planning in your 20s is to develop healthy financial habits that will last a lifetime. By learning to budget, save, invest, and manage debt responsibly at a young age, you set yourself up for long-term financial success. These habits, once ingrained, become second nature and contribute to your overall financial well-being.

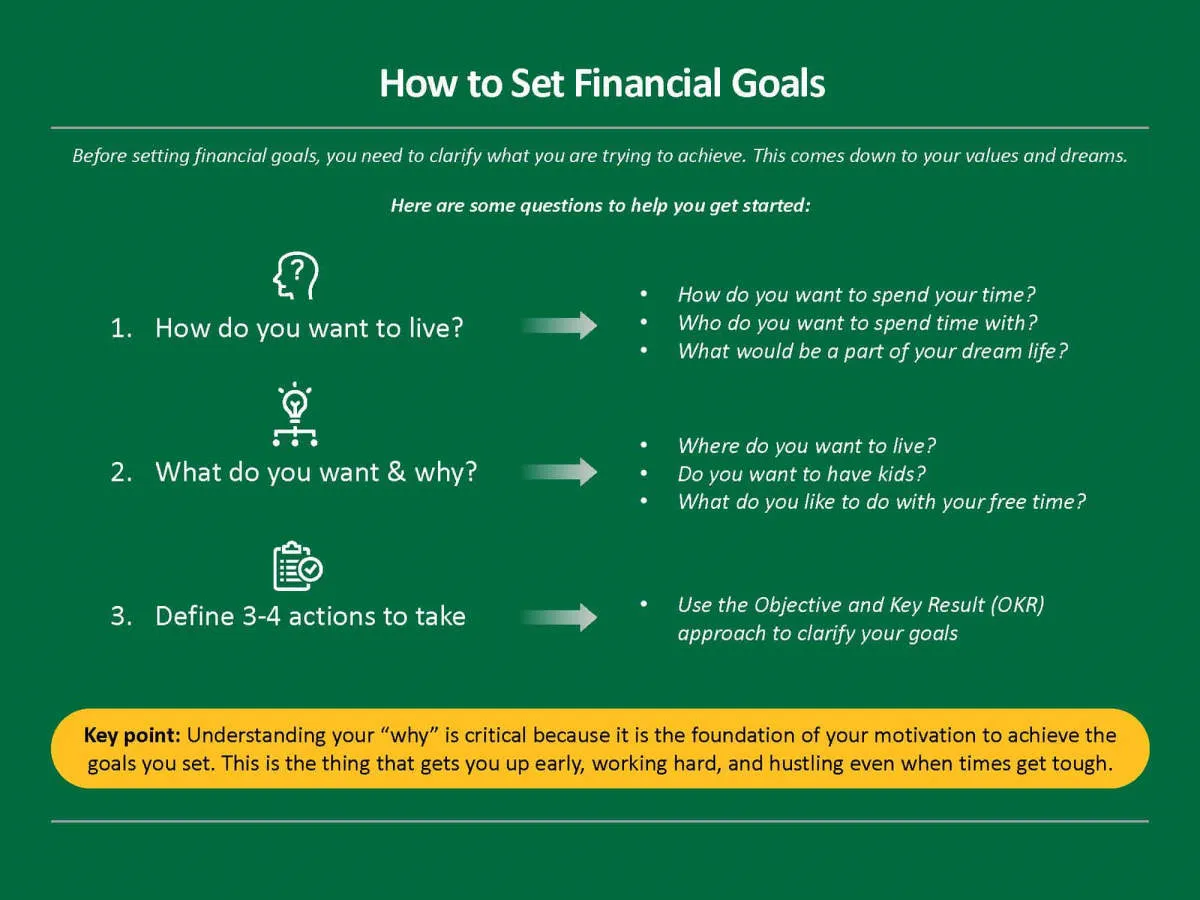

Setting Financial Goals

Having clear financial goals is like having a roadmap for your money. It gives you direction and helps you stay motivated. But where do you even begin in your 20s, a time often marked by new experiences, career starts, and maybe even some student loans?

Start by considering what’s important to you. Do you dream of owning a home? Traveling the world? Retiring early? These aspirations, while exciting, require financial planning.

Here’s how to set effective financial goals in your 20s:

1. Identify Your Short-Term and Long-Term Goals

- Short-term goals are achievable within a year or two. Think building an emergency fund, paying off credit card debt, or saving for a down payment on a car.

- Long-term goals require several years or even decades to achieve. Examples include buying a home, investing for retirement, or achieving financial independence.

2. Make Your Goals SMART

The SMART method is a popular and effective way to set goals:

- Specific: Define your goals clearly. Instead of saying “save more,” specify an amount, like “save $5,000.”

- Measurable: Track your progress. How much will you save each month to reach your goal?

- Achievable: Be realistic. Setting overly ambitious goals can lead to discouragement.

- Relevant: Ensure your goals align with your values and aspirations.

- Time-Bound: Give yourself a deadline. This creates urgency and helps you stay on track.

3. Prioritize Your Goals

You might have multiple goals. Rank them in order of importance. This will help you allocate your finances effectively. For example, paying off high-interest debt is often a top priority.

4. Break Down Large Goals into Smaller Steps

Large goals can feel overwhelming. Breaking them down into smaller, manageable steps makes them less daunting and more attainable. For instance, if your goal is to save $20,000 for a down payment, start by aiming to save $1,000 per month.

Creating a Budget and Saving Plan

Building a solid financial foundation in your 20s starts with understanding where your money is going and establishing a system to save consistently. This is where a budget and savings plan come into play. Here’s how to get started:

1. Track Your Income and Expenses:

Begin by tracking your income and all your expenses for a month or two. This will give you a clear picture of your cash flow – how much is coming in and where it’s going. Utilize budgeting apps, spreadsheets, or even a simple notebook to record this information. Be thorough and honest with yourself about your spending habits.

2. Differentiate Needs vs. Wants:

After analyzing your spending, categorize your expenses as either “needs” or “wants.” Needs are essentials like rent, groceries, utilities, and transportation. Wants are non-essential items like dining out, entertainment, and luxury purchases. Understanding this distinction is crucial for making informed decisions about where to potentially cut back.

3. Set Realistic Financial Goals:

What are your short-term and long-term financial goals? Do you want to save for a down payment on a house, pay off student loans, travel the world, or invest for retirement? Having clear financial goals will motivate you to stick to your budget and savings plan. Write your goals down and revisit them regularly.

4. Create Your Budget:

Now it’s time to build your budget. Allocate your income towards your various expense categories, prioritizing needs over wants. There are various budgeting methods you can follow, such as the 50/30/20 rule (50% of income on needs, 30% on wants, and 20% on savings and debt repayment) or the zero-based budget (where every dollar is assigned a purpose). Choose a method that best suits your lifestyle and goals.

5. Automate Your Savings:

Treat your savings like any other essential expense. Automate regular transfers from your checking account to your savings account. Start small if you need to, and gradually increase the amount as your income grows. Consider setting up a high-yield savings account to maximize your interest earnings.

6. Review and Adjust Regularly:

Your financial situation and goals may evolve over time. It’s important to review your budget and savings plan regularly, at least every few months, to ensure it aligns with your current needs and priorities. Don’t hesitate to make adjustments as necessary.

Building Good Credit

Building good credit is crucial in your 20s as it lays the foundation for future financial endeavors. A good credit score unlocks lower interest rates on loans, better credit card rewards, and even easier apartment rentals. Here’s how to start building a strong credit history:

1. Become an Authorized User

If you have a family member or close friend with good credit, ask to become an authorized user on their credit card. This allows their positive credit history to reflect on your credit report, giving your score a boost.

2. Open a Secured Credit Card

A secured credit card requires a security deposit that typically becomes your credit limit. This is a great option for building credit from scratch as it minimizes risk for lenders.

3. Use Credit Responsibly

Avoid maxing out your credit cards. A good rule of thumb is to keep your credit utilization rate (the percentage of available credit you’re using) below 30%.

4. Make Payments on Time

Payment history is the most significant factor influencing your credit score. Set up payment reminders or utilize autopay to ensure you never miss a due date.

5. Check Your Credit Report Regularly

Monitoring your credit report helps you catch any errors or signs of identity theft early on. You can access your credit report for free annually from each of the three major credit bureaus (Equifax, Experian, and TransUnion).

Investing for the Future

Your 20s are a prime time to start investing, even if you’re starting small. Time is your greatest asset in investing thanks to the power of compounding. The sooner you begin, the longer your money has to grow.

Here’s what to focus on:

- Retirement Accounts: Take advantage of employer-sponsored plans like 401(k)s, especially if they offer employer matching contributions. Consider opening an IRA (Individual Retirement Account) as well for additional tax advantages.

- Low-Cost Index Funds: These funds track a specific market index, offering diversification and typically lower fees than actively managed funds. They’re an excellent choice for beginners.

- Robo-Advisors: If you prefer a hands-off approach, robo-advisors build and manage an investment portfolio for you based on your risk tolerance and financial goals.

- Education and Growth: Continuously learn about investing. Read books, listen to podcasts, and consider taking online courses to increase your financial knowledge.

Remember: Investing involves risk, and it’s crucial to research and understand your investments. Consider consulting with a financial advisor for personalized guidance.

Managing Student Loans

Navigating student loans is a significant aspect of financial planning in your 20s. Here’s a breakdown of key strategies:

1. Understand Your Loans:

Before you can effectively manage your loans, you need a clear picture of what you owe. Gather all your loan documents and identify:

- Loan Servicer(s): The companies managing your loans.

- Interest Rates: Knowing your rates will help you prioritize payments if needed.

- Loan Terms: How long do you have to repay each loan?

- Total Amount Due: This includes principal and any accrued interest.

2. Explore Repayment Options:

Federal loans typically offer various repayment plans, including:

- Standard Repayment: Fixed monthly payments designed to pay off your loan within 10 years.

- Graduated Repayment: Payments start lower and gradually increase over time. This is a good option if you expect your income to rise.

- Income-Driven Repayment: Monthly payments are based on your income and family size. These plans can make repayment more manageable if you’re on a tight budget.

Contact your loan servicer to discuss the best option for your financial situation.

3. Consider Refinancing or Consolidation:

Refinancing involves taking out a new loan with a lower interest rate to pay off your existing loans. This can save you money over the life of your loan.

Consolidation combines multiple federal loans into one new loan, simplifying your repayment process and potentially securing a lower average interest rate.

4. Prioritize Loan Payments:

If you have multiple loans with different interest rates, prioritize paying down the loan with the highest rate first while making minimum payments on the others. This strategy will save you money on interest charges in the long run.

5. Budget for Loan Repayments:

Factor your loan payments into your monthly budget. Create a realistic spending plan that accommodates both your essential expenses and loan obligations. Consider using budgeting apps or tools to track your progress and stay on top of your finances.

Protecting Your Financial Future

Building a solid financial foundation in your 20s is about more than just managing your money today; it’s about safeguarding your future. Here’s how to incorporate protective measures into your personal finance plan:

1. Prioritize Emergency Savings

An emergency fund is crucial for handling unexpected expenses without derailing your finances. Aim for 3-6 months’ worth of living expenses saved in an easily accessible account. This safety net will protect you from going into debt due to unforeseen events like medical bills, car repairs, or job loss.

2. Consider Renter’s or Homeowner’s Insurance

Whether you rent or own, unexpected events like theft, fire, or natural disasters can be financially devastating. Renter’s insurance protects your belongings, while homeowner’s insurance safeguards your property and possessions. These policies provide essential financial protection in case of unforeseen circumstances.

3. Explore Health Insurance Options

Medical expenses can be incredibly costly. If you’re not covered under your parent’s plan or through your employer, research health insurance options. Consider factors like coverage, deductibles, and premiums to find a plan that fits your needs and budget. Having health insurance provides financial security and peace of mind.

4. Start Thinking About Disability Insurance

While it might seem distant, your ability to earn an income is one of your most valuable assets. Disability insurance replaces a portion of your income if you become unable to work due to illness or injury. Starting early allows you to lock in lower premiums while protecting your future earning potential.

Seeking Financial Advice

Navigating the world of personal finance in your 20s can feel overwhelming. While you’re establishing your career, exploring new opportunities, and figuring out your long-term goals, managing your money effectively is crucial. Seeking advice from experienced professionals can provide valuable guidance and set you on the right path.

Why Seek Financial Advice?

Financial advisors bring expertise and objectivity to your financial situation. They can help you:

- Create a personalized plan: Tailored to your specific income, expenses, goals, and risk tolerance.

- Navigate complex financial products: Understand investment options, insurance policies, and retirement plans.

- Stay accountable: Provide ongoing support and motivation to stick to your financial goals.

Types of Financial Advisors

Different types of advisors offer varying services. Consider what best suits your needs:

- Financial Planners: Provide comprehensive financial planning, including budgeting, saving, investing, retirement, and estate planning.

- Investment Advisors: Focus specifically on investment management and portfolio construction.

- Robo-Advisors: Offer automated, algorithm-driven investment advice, typically at a lower cost.

Finding the Right Advisor

When choosing a financial advisor, consider their:

- Credentials: Look for certifications like Certified Financial Planner (CFP®) or Chartered Financial Analyst (CFA®).

- Experience: Choose an advisor with experience working with individuals in your age group and financial situation.

- Fees: Understand how the advisor is compensated, whether through fees, commissions, or a combination of both.

- Communication Style: Select an advisor who you feel comfortable communicating with and who explains financial concepts in a clear and understandable manner.

Conclusion

In conclusion, creating a solid personal finance plan in your 20s is crucial for long-term financial stability and success. Start by setting goals, budgeting wisely, and investing early to secure a strong financial future.

{kind=link}