Planning for your retirement is crucial for financial stability. Learn how to create a personalized financial plan to secure your future.

Importance of Retirement Planning

Retirement planning is not just about saving money; it’s about designing your ideal future. It’s about ensuring you have the financial freedom to live life on your own terms, pursuing passions, and spending quality time with loved ones without financial worries.

Here’s why prioritizing retirement planning is crucial:

- Financial Security: Retirement planning provides a financial safety net, allowing you to maintain your lifestyle and cover essential expenses without relying solely on limited income sources like social security.

- Inflation Protection: The cost of living tends to rise over time. A well-structured retirement plan factors in inflation, ensuring your savings retain their purchasing power and you can maintain your standard of living.

- Healthcare Costs: As we age, healthcare expenses often increase. Retirement planning helps you allocate funds specifically for medical needs, alleviating potential financial strain during retirement.

- Pursuing Dreams: Retirement isn’t just about stopping work; it’s about starting a new chapter. Whether it’s traveling, pursuing hobbies, or starting a business, retirement planning empowers you to pursue your passions without financial constraints.

- Peace of Mind: Knowing you have a solid financial plan in place brings peace of mind, allowing you to enjoy the present and look forward to the future with confidence, knowing you’re financially prepared for the journey ahead.

Setting Retirement Goals

Retirement planning is more than just crunching numbers. It starts with a vision for your future. What do you want your retirement to look like? Where do you want to live? What do you want to do with your time?

Once you have a general idea, it’s time to set specific, measurable, achievable, relevant, and time-bound (SMART) goals. Here’s how:

1. Define Your Vision of Retirement

Imagine your ideal day in retirement. Are you traveling the world, pursuing a hobby, spending time with family, or a combination of these? Be as detailed as possible.

2. Break Down Your Goals

- Lifestyle Goals: Consider your desired living standard. Will you travel extensively, downsize your home, or pursue expensive hobbies?

- Financial Goals: How much money will you need annually to support your desired lifestyle? Consider healthcare costs, potential travel expenses, and leisure activities.

- Timeline Goals: When do you plan to retire? Having a target retirement age will help determine how much you need to save and at what rate.

3. Quantify Your Goals

Assign a monetary value to each goal. For example, if you want to travel for six months out of the year, estimate the annual cost. If you plan to relocate, research housing costs in your desired location.

4. Prioritize and Adjust

You may have multiple goals, and some might be more important than others. Prioritize your list and be realistic about what you can achieve. You might need to adjust your timeline or goals based on your financial situation.

Estimating Retirement Expenses

Retirement might mean saying goodbye to your 9-to-5, but it doesn’t mean saying goodbye to expenses. In fact, planning for your retirement income needs starts with understanding your potential expenses. While this might seem daunting, breaking it down can make it more manageable.

Consider Your Lifestyle

How do you envision your retirement? Will you be traveling the world, picking up new hobbies, or enjoying a quiet life at home? Your lifestyle choices will significantly impact your spending. Be realistic about your aspirations and how they translate into actual costs.

Factor in Inflation

Inflation erodes the purchasing power of your money over time. What costs $100 today might cost significantly more in 10 or 20 years. When estimating retirement expenses, factor in an average annual inflation rate to ensure your savings keep pace with rising costs.

Account for Healthcare Costs

Healthcare is a significant expense, especially as we age. Medicare will cover some healthcare costs, but not all. Factor in premiums, deductibles, co-pays, and potential long-term care needs.

Don’t Forget About Housing

Will you stay in your current home, downsize, or relocate? Consider potential costs like property taxes, insurance, maintenance, and potential rent or mortgage payments.

Review and Adjust Regularly

Life is full of surprises, and your retirement expenses won’t always be predictable. It’s crucial to review and adjust your estimated expenses annually, or whenever you experience a significant life change.

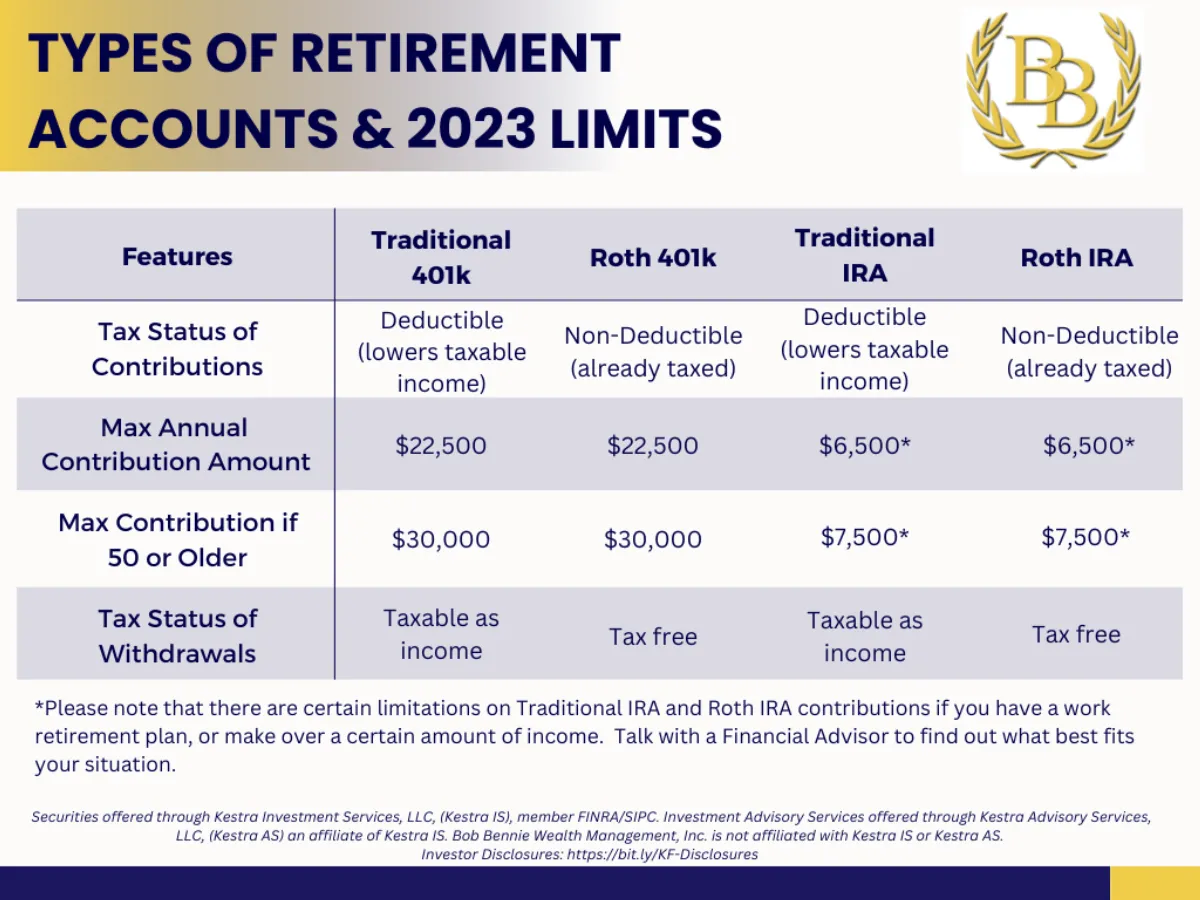

Choosing Retirement Accounts

One of the most important steps in planning for retirement is choosing the right retirement account. There are many different types of accounts available, each with its own advantages and disadvantages. Some of the most popular options include:

401(k) or 403(b)

These are employer-sponsored retirement plans. With these plans, you contribute a portion of your pre-tax income to the plan, and your employer may match a portion of your contributions. The money in the account grows tax-deferred, meaning you won’t owe taxes on it until you withdraw it in retirement.

Traditional IRA

A traditional IRA is a retirement account that allows you to make pre-tax contributions. This means that your contributions may be tax-deductible, which can save you money on your taxes in the present. The money in the account grows tax-deferred, meaning you won’t owe taxes on it until you withdraw it in retirement. However, you will have to pay taxes on your distributions in retirement.

Roth IRA

A Roth IRA is a retirement account that allows you to make after-tax contributions. This means that your contributions are not tax-deductible. However, the money in the account grows tax-free, meaning you won’t owe any taxes on it when you withdraw it in retirement.

Self-Directed Retirement Accounts

If you’re self-employed or have a side hustle, you can open a self-directed retirement account, such as a Solo 401(k) or a SEP IRA. These accounts offer similar tax advantages to employer-sponsored plans but give you more control over your investments.

Factors to Consider When Choosing an Account

When choosing a retirement account, you’ll need to consider a number of factors, including:

- Your employment status

- Your income level

- Your risk tolerance

- Your retirement goals

It’s essential to research and compare the different account options and consult with a financial advisor to determine the best fit for your individual circumstances.

Investment Strategies for Retirement

Planning for retirement requires careful consideration of various investment strategies tailored to your financial goals and risk tolerance. Here are some key strategies to consider:

1. Long-Term Growth:

Retirement investing is a long game. Prioritize investments that offer potential for long-term growth, such as:

- Stocks: While volatile in the short-term, stocks historically offer higher returns over extended periods.

- Real Estate: Investing in rental properties or REITs (Real Estate Investment Trusts) can provide rental income and potential property appreciation.

- Index Funds and Mutual Funds: These diversified investments offer exposure to a basket of assets, reducing risk and potentially maximizing returns.

2. Diversification:

The adage “Don’t put all your eggs in one basket” rings especially true for retirement planning. Diversify your portfolio by:

- Asset Allocation: Spread your investments across different asset classes – stocks, bonds, real estate, and more – to mitigate risk.

- Industry Diversification: Don’t limit yourself to one industry. Invest in companies across various sectors to minimize the impact of a downturn in any single industry.

- Geographic Diversification: Consider international investments to tap into global growth opportunities.

3. Risk Management:

Your risk tolerance will likely change as you approach retirement. Consider these strategies:

- Adjusting Your Asset Allocation: As you get closer to retirement, gradually shift towards a more conservative portfolio with a higher percentage of bonds and other fixed-income investments.

- Consider Annuities: Annuities provide a guaranteed stream of income in retirement, offering protection against market volatility.

4. Regular Contributions and Reinvesting:

The power of compounding can significantly impact your retirement savings. Establish a consistent habit of:

- Regular Contributions: Contribute to your retirement accounts (401(k), IRA, etc.) regularly, even if the amounts are small. Consistency is key.

- Reinvesting Earnings: Reinvest dividends, interest, and capital gains to accelerate the growth of your portfolio over time.

5. Professional Financial Advice:

Navigating investment strategies for retirement can be complex. Consider seeking guidance from a qualified financial advisor who can help you:

- Develop a Personalized Investment Plan: A financial advisor can tailor a plan based on your specific financial situation, goals, and risk appetite.

- Monitor and Adjust Your Portfolio: Markets and your financial circumstances can change. Regular portfolio reviews and adjustments are essential to stay on track.

Social Security and Pensions

Social Security and pensions often form a significant part of your retirement income. Understanding how they work and what to expect is crucial for effective retirement planning.

Social Security

Social Security is a federal program that provides retirement, disability, and survivor benefits to eligible individuals. The amount you receive depends on your lifetime earnings and the age at which you choose to start receiving benefits. You can start receiving Social Security retirement benefits as early as age 62, but your benefits will be reduced. The full retirement age, where you receive 100% of your benefits, varies based on your birth year. Delaying benefits past your full retirement age can increase your monthly payments.

Pensions

Pensions, also known as defined benefit plans, are retirement plans typically offered by employers. With a pension, your employer contributes to a fund that provides you with a fixed income stream during retirement. The amount you receive is typically based on factors like your salary history and years of service. However, traditional pensions are becoming less common.

Factoring Social Security and Pensions into Your Plan

- Estimate your benefits: Use online tools like the Social Security Administration’s website to get an estimate of your potential Social Security benefits. Contact your employer or pension plan administrator for information about your projected pension income.

- Consider your retirement age: When you plan to retire significantly impacts your Social Security and pension income. Earlier retirement means lower monthly benefits, while delaying retirement can increase your payments.

- Coordinate with other income sources: Understand how your Social Security and pension income will work in conjunction with other savings, investments, and potential income streams.

Healthcare Costs in Retirement

One of the most significant expenses you’ll face in retirement is healthcare. As you age, the need for medical care typically increases, and without the safety net of employer-sponsored health insurance, these costs can quickly erode your retirement savings.

Factors influencing your healthcare costs in retirement include:

- Your current health and family medical history

- Your estimated longevity

- The cost of premiums for Medicare and supplemental health insurance plans

- Out-of-pocket expenses like deductibles, co-pays, and prescription drugs

- The potential need for long-term care services

Planning for healthcare expenses during retirement is essential. Consider these steps:

- Estimate your healthcare costs: Research the average healthcare expenses for retirees in your area and factor in your personal health situation. Online calculators can be helpful for this purpose.

- Maximize your Medicare benefits: Understand the different parts of Medicare (Parts A, B, C, and D) and enroll in the options that best suit your needs and budget.

- Explore supplemental health insurance: Consider Medigap policies, retiree health plans, or other options to cover costs that Medicare doesn’t.

- Plan for long-term care: Investigate long-term care insurance options or explore other ways to finance potential long-term care needs.

- Build a dedicated healthcare fund: Consider setting aside funds specifically for healthcare expenses in retirement. A Health Savings Account (HSA) can be a tax-advantaged way to save if you’re eligible.

Reviewing and Adjusting Your Plan

Creating a financial plan for retirement isn’t a “set it and forget it” task. As you move through life, your circumstances change, and your plan needs to adapt with you. Here’s why regular reviews are essential and what to focus on:

Why Regular Reviews are Critical

- Life Events: Marriage, divorce, children, home buying, career changes – these all significantly impact your financial needs and goals.

- Market Fluctuations: Investment returns aren’t guaranteed. Market downturns can impact your retirement savings, requiring adjustments to your strategy.

- Inflation: The rising cost of goods and services erodes the purchasing power of your money over time. Your plan needs to outpace inflation to maintain your living standards.

- Health and Longevity: Unexpected healthcare costs or a longer lifespan than anticipated require adjustments to ensure your money lasts.

How Often to Review

A good rule of thumb is to review your plan at least annually. However, major life events might warrant a more immediate review.

Key Areas to Review and Adjust

- Savings Rate: Evaluate if you’re saving enough to meet your goals, especially after life changes like a salary increase or a career break.

- Investment Strategy: Reassess your risk tolerance and adjust your asset allocation as needed. You may need to become more conservative as you get closer to retirement.

- Retirement Expenses: Review your estimated retirement expenses and factor in potential changes, such as healthcare costs or travel plans.

- Withdrawal Strategy: Determine how you’ll access your savings in retirement, considering factors like taxes and longevity.

Seeking Professional Guidance

A financial advisor can provide valuable insights and help you navigate the complexities of retirement planning. They can offer personalized recommendations based on your unique circumstances and help you stay on track with your goals.

Conclusion

In conclusion, creating a solid financial plan for retirement is crucial for a secure future. Start early, set realistic goals, invest wisely, and regularly review your plan to ensure a comfortable retirement.

{kind=link}