Creating a budget tailored to your needs is essential for financial success. Learn how to craft a personalized budget that aligns with your lifestyle and helps you achieve your money goals in our comprehensive guide.

Importance of Budgeting

Creating and maintaining a budget is fundamental to achieving your financial goals, no matter how big or small they may be. It’s more than just tracking your income and expenses; it’s a proactive approach to managing your money, making informed financial decisions, and building a secure future.

Here’s why budgeting is crucial:

- Financial Control: Budgeting gives you a clear picture of your money flow – where it comes from and where it goes. This awareness empowers you to make conscious spending choices aligned with your priorities.

- Goal Achievement: Whether saving for a down payment, paying off debt, or taking a dream vacation, a budget acts as a roadmap to reach your financial destinations. It allows you to allocate funds strategically, accelerating your progress towards your goals.

- Debt Reduction: A budget helps you identify areas of overspending and redirect those funds towards paying off debts faster. By allocating more money to debt repayment, you can reduce interest payments and become debt-free sooner.

- Stress Reduction: Money worries are a major source of stress. Having a budget provides peace of mind by giving you a clear understanding of your financial situation, eliminating financial surprises, and allowing you to face the future with confidence.

- Preparedness for Emergencies: Life is unpredictable, and unexpected expenses can arise at any moment. A well-structured budget includes an emergency fund, ensuring you have a financial safety net to handle unexpected situations without derailing your financial stability.

In essence, budgeting is not about restricting your life; it’s about empowering you to live a financially secure and fulfilling life by making informed decisions about your money.

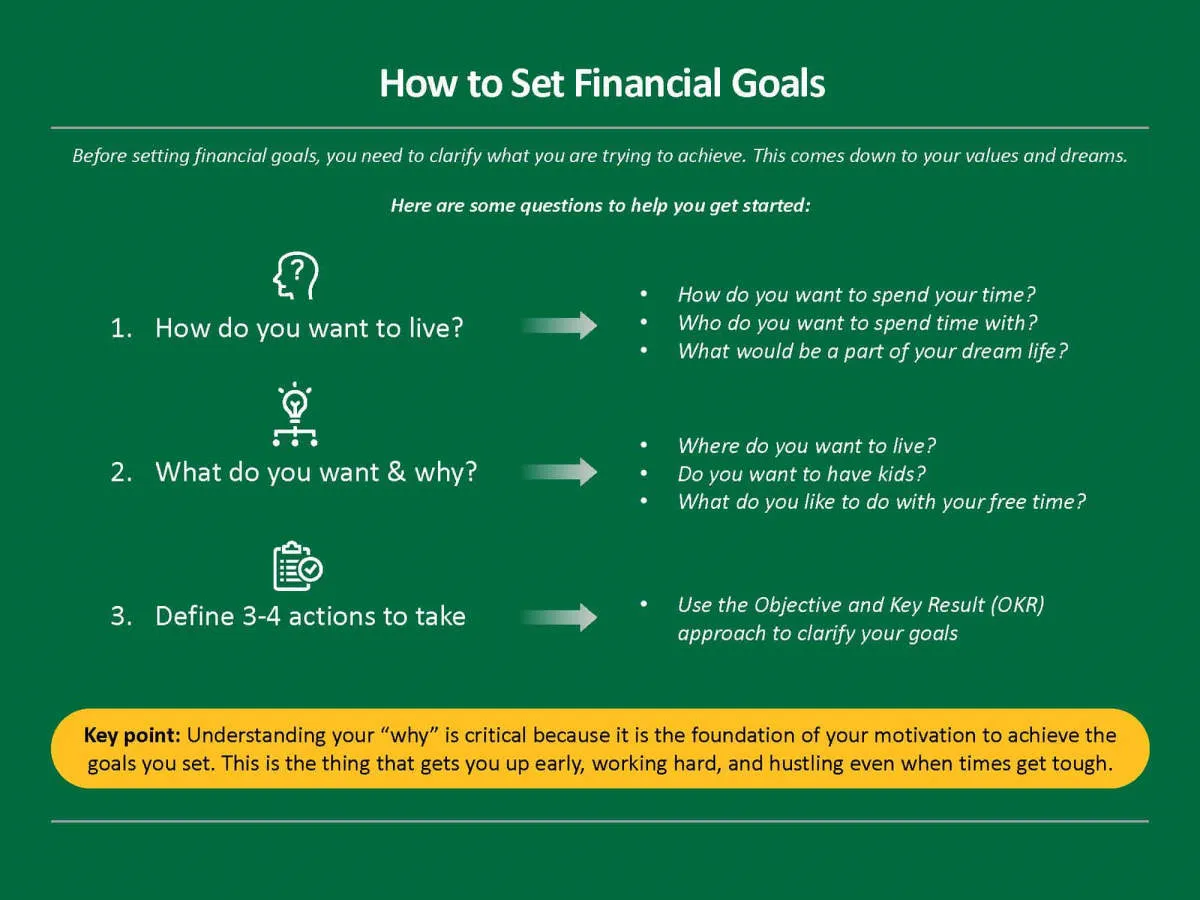

Setting Financial Goals

A budget without a goal is like a ship without a destination – you might sail, but you won’t know if you’re headed in the right direction. Before you crunch numbers and allocate spending, you need to define your “why”. What are you working towards? This is where setting clear financial goals comes in.

Start by brainstorming your short-term, mid-term, and long-term goals.

- Short-term goals might include building an emergency fund, paying off a credit card, or saving for a down payment on a car within the next year.

- Mid-term goals could involve saving for a vacation, paying off a significant portion of student loans, or investing in a retirement account over the next 3-5 years.

- Long-term goals typically involve larger sums and longer timelines, such as buying a house, funding your children’s education, or securing a comfortable retirement in 10+ years.

Make your goals SMART:

- Specific: Clearly define what you want to achieve. “Save more money” is vague; “Save $5,000 for a down payment” is specific.

- Measurable: Quantify your goals with numbers so you can track progress.

- Achievable: Set realistic goals that you can reach with effort and planning.

- Relevant: Choose goals that align with your values and priorities.

- Time-Bound: Set deadlines to create a sense of urgency and accountability.

Once you have clear financial goals, your budget becomes the roadmap to achieve them. By aligning your spending and saving habits with your aspirations, you transform your budget from a restrictive chore into a powerful tool for achieving financial success.

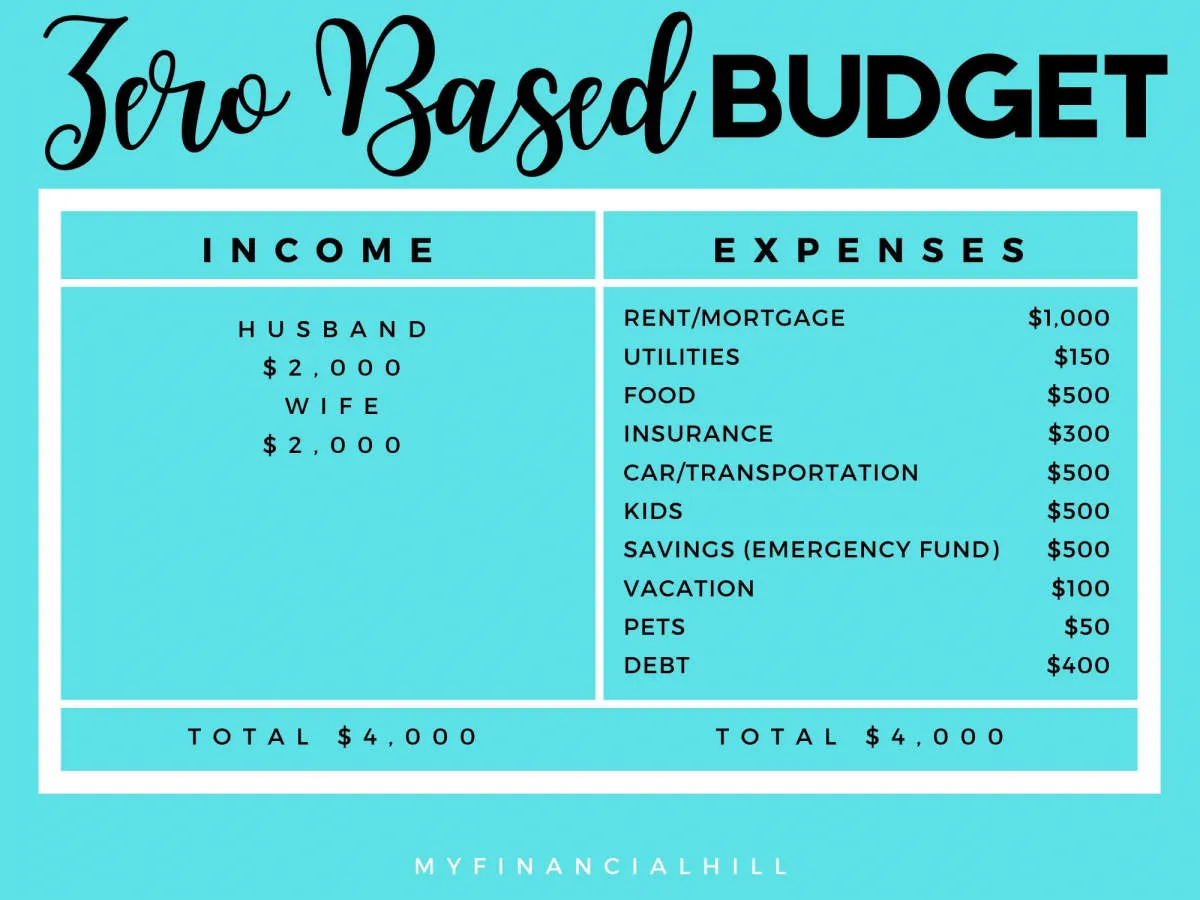

Tracking Your Income and Expenses

The cornerstone of any successful budget is understanding your cash flow – where your money comes from and where it goes. This means diligently tracking both your income and expenses.

Tracking Income:

This part is often more straightforward. List down all sources of income:

- Salary (after taxes)

- Wages (if paid hourly)

- Bonuses

- Side hustle income

- Investment returns

- Other sources (e.g., alimony, child support)

Tracking Expenses:

This is where most people need to pay close attention. Be thorough and honest with yourself. Categorize your spending to make it easier to analyze:

- Fixed Expenses: These stay relatively the same each month. (Rent/mortgage, car payments, loan payments, utilities, subscriptions)

- Variable Expenses: These fluctuate. (Groceries, dining out, entertainment, transportation, clothing)

- Periodic Expenses: Occur infrequently but are important to factor in. (Car repairs, medical bills, annual fees, gifts)

Methods for Tracking:

- Budgeting Apps: Many user-friendly apps connect to your bank accounts and automatically categorize transactions.

- Spreadsheets: Create your own system for inputting income and expenses.

- Notebook and Pen: The old-fashioned way still works! Be sure to keep receipts for accurate recording.

Tips for Effective Tracking:

- Be Consistent: Make it a habit to track regularly, whether daily, weekly, or at least monthly.

- Review Regularly: Don’t just track and forget! Analyze your spending patterns to identify areas for improvement or adjustment.

- Be Honest with Yourself: Don’t omit any expenses, no matter how small they seem.

Creating a Realistic Budget

A realistic budget is the cornerstone of effective financial management. It’s not about restricting your life, but empowering you to achieve your financial goals without constantly feeling financially strained. Here’s how to create a budget that’s tailored to your unique circumstances and helps you reach your financial aspirations:

1. Track Your Income and Expenses

Start by understanding where your money is coming from and going. Track your income from all sources, including salary, wages, investments, and any other forms of revenue. Next, track your expenses meticulously. Utilize budgeting apps, spreadsheets, or even a notebook to record every dollar you spend. Categorize your expenses for a clearer picture of your spending habits.

2. Differentiate Between Needs and Wants

Analyze your spending patterns and differentiate between “needs” and “wants.” Needs are essential for your daily living, such as housing, groceries, utilities, and transportation. Wants are things that enhance your life but aren’t essential for survival, like entertainment, dining out, and luxury items.

3. Set Realistic Spending Limits

Based on your income and expense analysis, establish realistic spending limits for each category. Be honest about what you can afford without jeopardizing your financial well-being. Prioritize your needs while allocating a portion of your budget for your wants. Remember, it’s about finding a balance that allows you to enjoy life while working towards your financial goals.

4. Build in Flexibility and Emergency Funds

Life is unpredictable, so your budget needs to be flexible. Don’t create a budget so rigid that it can’t accommodate unexpected expenses. Build in some “wiggle room” for unplanned events. Additionally, prioritize building an emergency fund to cover unexpected costs like medical bills or car repairs. Having this financial safety net prevents you from derailing your entire budget when unforeseen events arise.

5. Monitor, Adjust, and Review

Creating a budget isn’t a one-time task. It requires consistent monitoring and adjustments. Regularly review your budget, ideally monthly, to see if you’re staying on track, identify areas where you can improve, and make necessary adjustments based on changes in your income, expenses, or financial goals.

Tips for Sticking to Your Budget

You’ve done the hard part and created a budget that reflects your financial goals. Now, the real challenge begins: sticking to it. Here are a few tips to keep you on track:

1. Track Your Spending Regularly

Consistently tracking your expenses is crucial. Whether you prefer a budgeting app, a spreadsheet, or a good old-fashioned notebook, find a system that works for you and stick with it. This allows you to see where your money is going and make adjustments as needed.

2. Automate Your Savings

Treat your savings like any other essential expense by automating transfers to your savings account each month. This ensures you’re consistently putting money aside for your goals and reduces the temptation to spend it elsewhere.

3. Use the “Envelope System”

Consider utilizing the envelope system for discretionary spending categories like dining out or entertainment. Allocate a specific amount of cash to each category at the beginning of the month. Once the cash is gone, you’re done spending in that area for the month.

4. Find a Budgeting Buddy

Having someone to share your financial journey with can be incredibly motivating. Find a trusted friend or family member who can provide support, encouragement, and even hold you accountable to your budget.

5. Regularly Review and Adjust

Life is full of unexpected twists and turns. Your budget should be flexible enough to adapt. Make it a habit to review your budget regularly (e.g., monthly or quarterly) and make adjustments based on changes in your income, expenses, or financial goals.

6. Celebrate Small Wins

Sticking to a budget is a marathon, not a sprint. Acknowledge and celebrate your successes along the way. Whether you’ve successfully stuck to your grocery budget for a month or reached a savings milestone, take the time to appreciate your progress.

Adjusting Your Budget as Needed

Creating a budget is not a “set it and forget it” task. Life is constantly changing, and your budget needs to be flexible enough to change with it. Here’s why and how to adjust your budget as needed:

Why Your Budget Needs Regular Adjustments

- Life Changes: New job? Marriage? Baby? Big move? These milestones often come with significant financial shifts.

- Unexpected Expenses: Car repairs, medical bills, or a broken appliance can throw your budget off track.

- Inflation: The rising cost of goods and services means your money may not stretch as far as it used to.

- Financial Goals: As your goals evolve (saving for a house, early retirement), so should your budget.

How to Adjust Your Budget

- Review Regularly: Don’t wait for a financial crisis! Review your budget at least monthly, or more frequently if needed.

- Track Your Spending: Use budgeting apps, spreadsheets, or the old-fashioned pen-and-paper method to monitor your cash flow.

- Identify Areas for Adjustment: Where can you cut back? Are there subscriptions you can live without? Can you reduce your grocery bill?

- Reallocate Funds: Shift money from less important categories to cover increased costs or reach your goals faster.

- Be Realistic: Don’t set unrealistic expectations. Small, sustainable adjustments are more likely to stick long-term.

Using Budgeting Tools and Apps

Managing your finances effectively often requires more than just mental calculations and scribbled notes. Fortunately, we live in an age where technology can make budgeting significantly easier. Budgeting tools and apps provide a convenient and structured way to track income, expenses, and savings goals.

There are a plethora of options available, each with unique features. Here’s what to look for:

Key Features to Consider:

- Expense Tracking: The ability to connect to your bank accounts and credit cards for automatic transaction importing makes tracking expenses much easier.

- Income Recording: Inputting and categorizing your income sources provides a clear picture of your overall financial situation.

- Budgeting Categories: Pre-set or customizable categories help you allocate your money effectively based on your spending habits and priorities.

- Goal Setting: Setting short-term and long-term financial goals within the app can keep you motivated and track your progress.

- Reporting and Analysis: Visual representations of your spending habits through charts and graphs can reveal areas where you can save.

Choosing the Right Tool for You:

The best budgeting tool depends on your individual needs and preferences. Some popular options include:

- Mint: Known for its comprehensive features, including bill payment reminders and credit score monitoring.

- YNAB (You Need a Budget): Emphasizes proactive budgeting by assigning every dollar a purpose.

- Personal Capital: Geared towards investment tracking and retirement planning, in addition to budgeting.

- PocketGuard: Simplifies budgeting with an approachable interface and “In the Green” spending guidance.

Many apps offer free versions with basic features and paid versions with enhanced functionality. Explore free trials to find the best fit for your financial management style.

Reviewing Your Budget Regularly

Creating a budget is a crucial first step towards financial health, but it’s not a “set it and forget it” solution. Life is constantly changing, and your budget needs to adapt alongside those changes. Regularly reviewing your budget ensures it remains relevant to your current financial situation and helps you stay on track towards your financial goals.

How often should you review your budget? While there’s no one-size-fits-all answer, most financial experts recommend a review at least once a month. This allows you to track your spending habits, identify any areas where you’ve overspent, and make adjustments as needed.

What should you look for during a budget review?

- Income and Expenses: Have there been any changes to your income streams or regular expenses?

- Spending Habits: Analyze your spending in different categories. Are you consistently overspending in certain areas?

- Progress Towards Goals: Are you on track to meet your savings goals or debt repayment timelines?

- Unexpected Expenses: Did you encounter any unforeseen costs that need to be factored into future budgets?

By regularly reviewing and adjusting your budget, you can ensure it remains a valuable tool for achieving your financial goals.

Conclusion

In conclusion, creating a personalized budget is crucial for financial success. By tracking expenses, setting realistic goals, and adjusting as needed, you can achieve your financial objectives.

{kind=link}