Entering your 40s is a crucial time for financial planning. Discover key strategies and tips to achieve financial success in this pivotal decade of your life. From investing wisely to saving for retirement, learn how to navigate and thrive in your 40s financially.

Importance of Financial Planning in Your 40s

Your 40s are a pivotal time in your life, both personally and financially. You’re likely at the peak of your career, juggling family responsibilities, and potentially staring down the reality of retirement being closer than you think. This is why prioritizing financial planning in your 40s is crucial.

Solidifying Your Financial Foundation

By this stage, you’ve likely accumulated some assets, but you’re also facing increasing expenses. Your 40s are the time to solidify your financial foundation and ensure you’re on track to meet both your short-term and long-term goals. This means:

- Managing Debt: Aggressively paying down high-interest debts, like credit cards, should be a priority. Consider refinancing mortgages or consolidating loans to lower interest rates and free up cash flow.

- Boosting Retirement Savings: Retirement might seem far off, but it’s closer than ever. Increase your retirement contributions and explore catch-up contributions if you’re behind on your savings goals.

- Investing Wisely: Review your investment portfolio to ensure it aligns with your risk tolerance and time horizon. Consider diversifying your investments to mitigate risk and maximize potential returns.

Planning for the Unexpected

Life is full of surprises, and not all of them are pleasant. In your 40s, it’s crucial to have a plan in place to protect yourself and your loved ones from the unexpected:

- Insurance Coverage: Review your life, health, and disability insurance policies to make sure they adequately cover your needs.

- Emergency Fund: Aim to have 3-6 months’ worth of living expenses saved in an easily accessible account to cover unexpected events like job loss or medical emergencies.

- Estate Planning: Create or update your will, living will, and power of attorney documents. These are essential for ensuring your wishes are carried out and your loved ones are taken care of in case of an emergency.

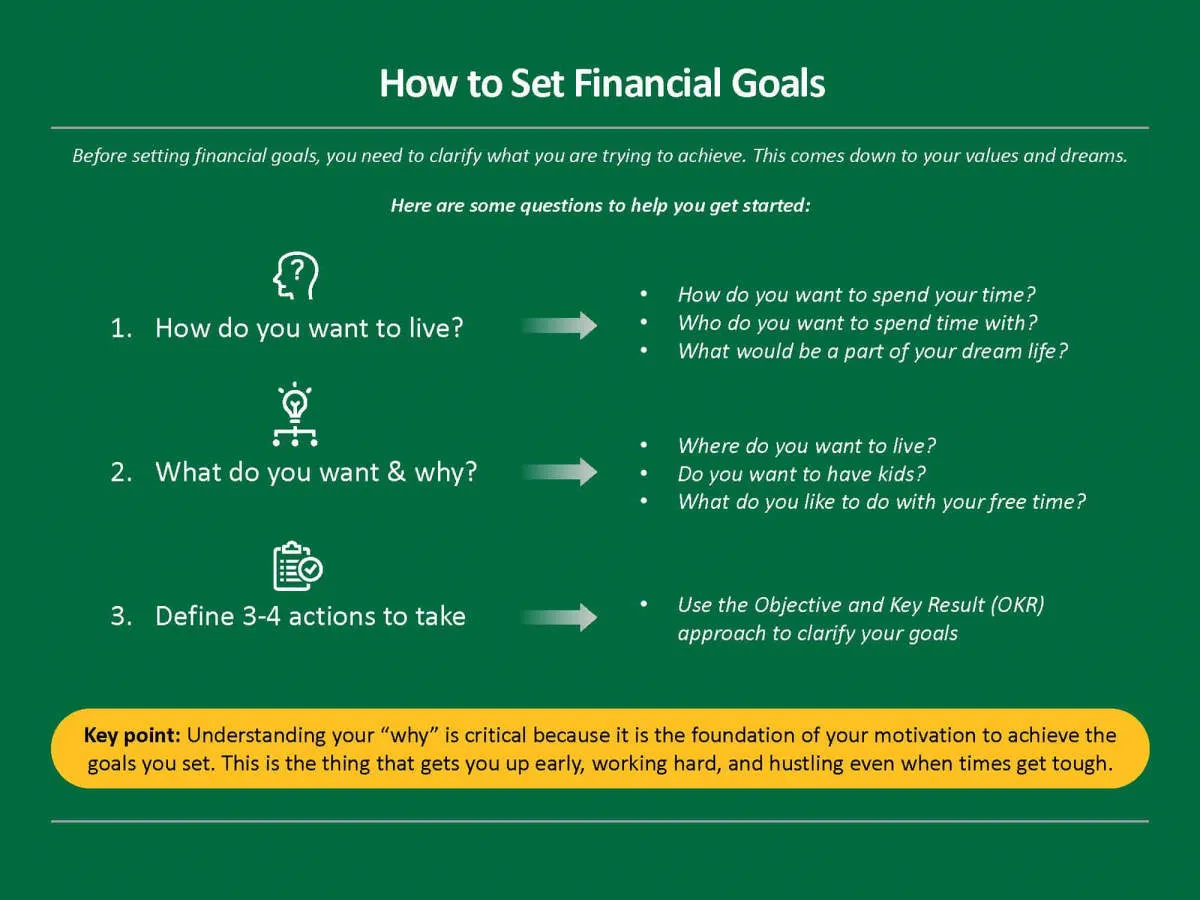

Setting Financial Goals

Turning 40 is a significant milestone, often accompanied by a shift in perspective. Your financial goals should reflect your evolving priorities and aspirations. Now is the time to take stock of your financial situation and set clear, achievable goals.

Identify Your Priorities

What matters most to you? Is it securing your retirement, supporting your children’s education, purchasing a dream home, or traveling the world? Defining your priorities will provide clarity and direction for your financial planning.

Be Specific and Realistic

Avoid vague goals. Instead, set specific, measurable, achievable, relevant, and time-bound (SMART) goals. For instance, instead of saying “I want to save for retirement,” quantify it as “I want to save $500,000 in my retirement account by age 60.”

Consider Your Time Horizon

Your financial goals should align with your time horizon. Short-term goals (within 1-3 years) might include creating an emergency fund or paying off credit card debt. Mid-term goals (3-10 years) could involve saving for a down payment or funding a child’s education. Long-term goals (10+ years) typically center around retirement planning.

Regularly Review and Adjust Your Goals

Life is dynamic, and your financial goals should be adaptable. Regularly review your goals to ensure they remain aligned with your current circumstances and aspirations. Don’t hesitate to adjust them as needed, based on changes in your income, expenses, or life events.

Creating a Budget and Saving Plan

Your 40s are a crucial time to get serious about your financial future. By now, you likely have a good understanding of your income, expenses, and financial goals. Here’s how to craft a budget and savings plan that will set you up for success:

1. Track Your Spending:

You can’t manage what you don’t measure. Utilize budgeting apps, spreadsheets, or even a simple notebook to track every dollar you spend for a month or two. This will give you a clear picture of where your money is going.

2. Identify Needs vs. Wants:

Separate your spending into essential needs (housing, food, transportation) and discretionary wants (entertainment, dining out). Look for areas where you can potentially reduce spending on wants to free up more money for saving and investing.

3. Set Realistic Financial Goals:

Whether it’s early retirement, a down payment on a bigger home, or your children’s education, clearly define your financial goals. Having specific targets will motivate you to stick to your budget and savings plan. Break down large goals into smaller, more manageable milestones.

4. Automate Your Savings:

Treat savings like a non-negotiable expense. Set up automatic transfers from your checking account to your savings and investment accounts each month. Start small if needed and gradually increase the amount as your income allows.

5. Prioritize Retirement Savings:

Time is your greatest asset when it comes to retirement savings. If you haven’t already, max out contributions to your employer-sponsored retirement plan, especially if there’s an employer match. Consider other retirement savings vehicles like IRAs to boost your retirement nest egg.

6. Review and Adjust Regularly:

Your financial situation and goals will evolve over time. Review your budget and savings plan at least annually, or whenever you experience a major life change, to make sure it still aligns with your priorities.

Investing for Retirement

Your 40s are a crucial time to ramp up your retirement savings. While it might feel far off, the earlier you invest, the more time your money has to grow through the power of compounding. Here’s what to focus on:

Maximize Retirement Accounts:

Take full advantage of employer-sponsored plans like 401(k)s, especially if there’s an employer match. Increase your contributions annually, even if it’s just by a small percentage.

Consider Catch-Up Contributions:

Once you turn 50, you can make “catch-up” contributions to your retirement accounts. This allows you to invest an additional amount beyond the usual limit, helping you boost your savings rate.

Diversify Your Portfolio:

Don’t put all your eggs in one basket. Diversify your investments across different asset classes (stocks, bonds, real estate, etc.) to manage risk and potentially enhance returns.

Review and Adjust Your Risk Tolerance:

As you get closer to retirement, you might become more risk-averse. Review your investment portfolio and adjust your asset allocation to align with your changing risk tolerance and time horizon.

Seek Professional Advice:

Consider consulting with a certified financial advisor to create a personalized retirement plan. They can help you determine how much you need to save, choose appropriate investments, and navigate any complexities.

Managing Debt Effectively

Entering your 40s often comes with increased financial responsibilities – mortgages, children’s education, and even caring for aging parents. Effectively managing debt is crucial during this decade to ensure financial stability and progress towards your long-term goals.

Prioritize and Create a Plan:

Not all debt is created equal. High-interest debt, such as credit cards, should be tackled aggressively. Create a budget that outlines your income, expenses, and allocates funds towards debt repayment. Consider using the debt snowball or avalanche methods to focus your efforts.

Explore Debt Consolidation:

If you have multiple debts, explore consolidating them into a single loan with a lower interest rate. This can simplify payments and potentially save you money on interest charges. Options include balance transfer credit cards or a personal loan.

Refinance for Better Terms:

If you have a mortgage or other large loans, investigate refinancing options. Interest rates may have dropped since you initially took out the loan. Refinancing could lower your monthly payments or shorten the loan term, saving you money in the long run.

Negotiate with Creditors:

Don’t hesitate to negotiate with your creditors if you’re facing financial difficulties. They may be willing to work with you by offering lower interest rates, waived fees, or a temporary hardship plan. Communication is key in these situations.

Seek Professional Guidance:

If you’re overwhelmed with debt or struggling to create a plan, consider consulting a certified financial advisor. They can provide personalized advice, help you create a realistic budget, and explore debt management solutions tailored to your situation.

Protecting Your Financial Future

While building wealth is a primary goal in your 40s, protecting what you’ve earned becomes equally crucial. Here’s how to fortify your financial well-being:

1. Review and Amplify Insurance Coverage

Life throws curveballs, and being underinsured can derail your financial stability. Review your life, health, disability, and property insurance coverage. Consider increasing coverage amounts if necessary, especially with growing families and assets.

2. Prioritize Emergency Savings

A robust emergency fund acts as a financial cushion against unforeseen events like job loss or medical emergencies. Aim for 6-12 months’ worth of living expenses in an easily accessible account.

3. Estate Planning: Secure Your Legacy

Don’t delay estate planning. Draft or update your will, designate beneficiaries for accounts, and consider trusts to ensure your assets are distributed according to your wishes and your loved ones are provided for.

4. Guard Against Fraud and Identity Theft

Financial security involves safeguarding yourself against fraud. Regularly review bank and credit card statements for discrepancies, shred sensitive documents, and be vigilant about online security practices. Consider identity theft protection services for added peace of mind.

Planning for Major Life Events

Your 40s can be a time of significant life changes, both personally and financially. Children might be heading to college, aging parents might require care, or you may be considering a career change or early retirement. Planning for these major life events is crucial to ensuring your financial stability and minimizing stress:

1. Children’s Education:

If you have children, college costs are likely a major financial consideration. Start planning and saving early through 529 plans or other investment vehicles. Research different colleges and their costs, and discuss affordability and expectations with your children.

2. Caring for Aging Parents:

As your parents age, they might need additional care. Have open conversations with them about their finances, living arrangements, and healthcare preferences. Explore long-term care insurance options and factor potential costs into your financial planning.

3. Housing Changes:

Your housing needs may shift in your 40s. Perhaps you need a larger home, want to downsize, or are considering a move. Analyze the financial implications of each scenario, including mortgage payments, property taxes, and potential maintenance costs.

4. Career Transitions:

You might be considering a career change, starting a business, or pursuing early retirement. Each of these choices will impact your finances. Evaluate your risk tolerance, update your resume, network within your field, and consider any necessary training or education for new opportunities.

5. Healthcare Costs:

As you age, healthcare costs tend to rise. Review your health insurance coverage and explore options like Health Savings Accounts (HSAs) to manage potential expenses. Factor in the potential need for long-term care insurance as well.

Seeking Professional Advice

Navigating your finances in your 40s can feel complex. You’re juggling saving for retirement, potentially funding college for your children, managing debt, and more. This is where seeking professional financial advice can be invaluable.

A financial advisor can provide personalized guidance tailored to your specific circumstances. They can help you:

- Assess your current financial situation: Analyzing your assets, debts, income, and expenses to create a clear picture of where you stand.

- Define your financial goals: Identifying short-term and long-term goals, like retirement savings, buying a house, or funding education.

- Develop a customized financial plan: Creating a roadmap to achieve your goals, including investment strategies, debt management plans, and retirement planning.

- Navigate complex financial products: Providing clarity and guidance on choosing the right investment options, insurance policies, and other financial products.

- Adjust your plan as needed: Life throws curveballs. A financial advisor can help you adapt your plan to accommodate unexpected events or changes in your circumstances.

When choosing a financial advisor, look for:

- Fiduciary duty: Ensure they are legally obligated to act in your best interest.

- Experience and expertise: Seek out advisors with a proven track record and specialization in areas relevant to your needs.

- Clear communication: Choose an advisor who explains financial concepts in an understandable way and keeps you informed about your finances.

Remember, seeking professional financial advice is an investment in your future financial well-being.

Conclusion

In conclusion, setting financial goals, prioritizing retirement savings, and reviewing investments regularly are key steps to achieve financial success in your 40s.

{kind=link}