Learn important strategies and tips on how to achieve financial stability in your life. From budgeting and saving to investing wisely, this article will provide you with actionable steps to secure your financial future.

Setting Clear Financial Goals

The cornerstone of financial stability is having a clear vision of what you want to achieve. Without well-defined goals, it’s easy to fall into a pattern of aimless spending and saving without making real progress. Setting clear financial goals provides direction and motivation, guiding your financial decisions and helping you prioritize your spending.

Types of Financial Goals

Financial goals can vary greatly depending on individual circumstances and aspirations. However, some common categories include:

- Short-term goals: These are goals you aim to achieve within a year, such as building an emergency fund, paying off a credit card debt, or saving for a vacation.

- Mid-term goals: Goals achievable within one to five years, like making a down payment on a house, buying a car, or funding a child’s education, fall under this category.

- Long-term goals: These are goals that require more than five years to achieve, such as retirement planning, investing for your children’s future, or purchasing a second home.

Setting SMART Goals

When defining your financial goals, it’s crucial to make them SMART:

- Specific: Clearly define what you want to achieve. Instead of saying “save more money,” specify “save $5,000 for a down payment.”

- Measurable: Quantify your goals with specific numbers. Instead of saying “reduce debt,” state “pay off $10,000 of credit card debt.”

- Achievable: Set realistic goals that are within your financial reach. Don’t set yourself up for failure with unattainable targets.

- Relevant: Ensure your goals align with your values and overall life goals. Don’t prioritize a luxury vacation over saving for your child’s education if education is more important to you.

- Time-bound: Establish a clear timeframe for achieving each goal. This creates a sense of urgency and helps you track your progress.

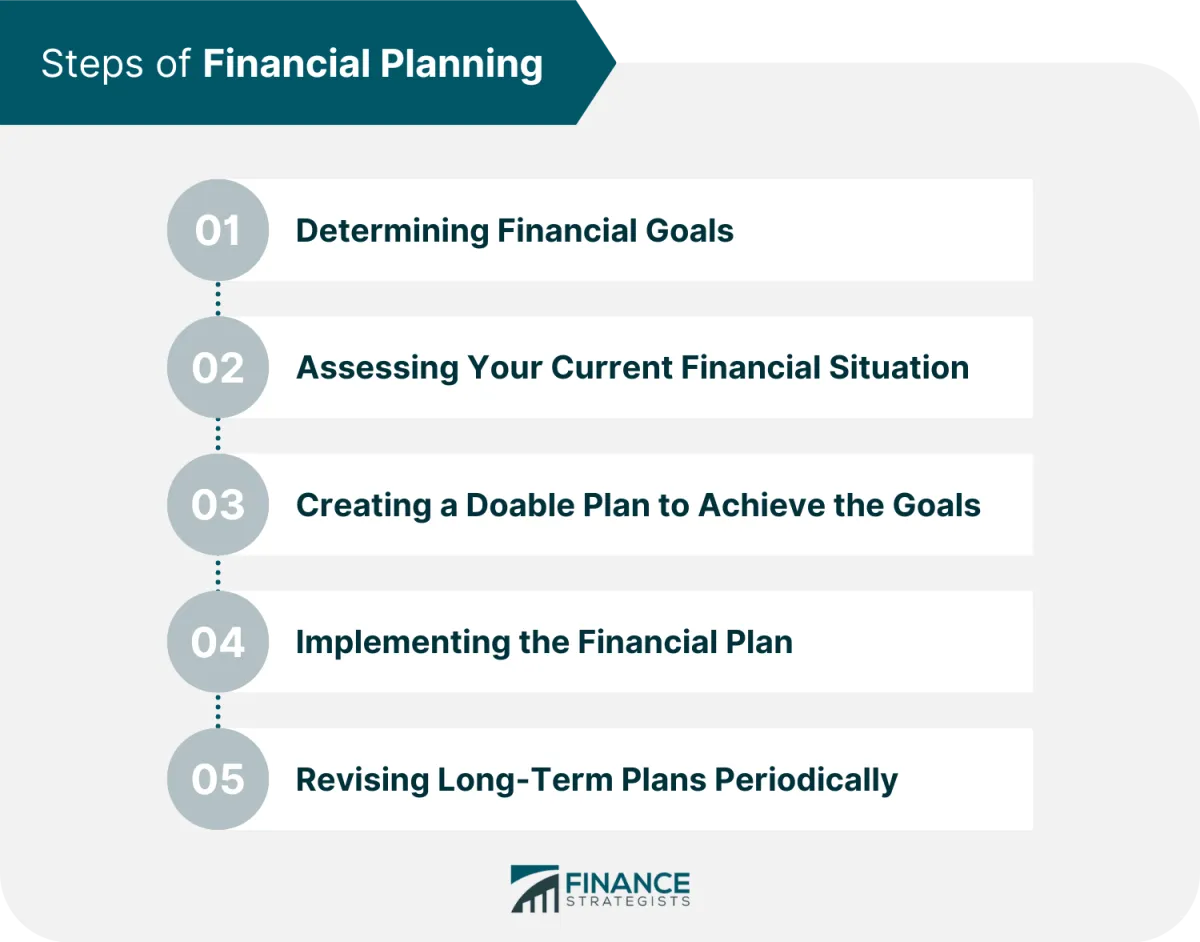

Creating a Financial Plan

A comprehensive financial plan acts as your roadmap to financial stability. It provides a structured approach to managing your money, enabling you to achieve both short-term and long-term goals. Here’s a step-by-step guide to crafting your personalized plan:

1. Assess Your Current Financial Situation

Start by understanding where you stand financially. List your assets (e.g., savings, investments) and liabilities (e.g., debts, loans). Calculate your net worth and track your income and expenses to get a clear picture of your cash flow.

2. Set Financial Goals

Define your financial aspirations. Are you aiming to buy a house, retire early, or secure your children’s education? Establish specific, measurable, achievable, relevant, and time-bound (SMART) goals to provide direction for your plan.

3. Create a Budget

Develop a realistic budget that aligns with your financial goals. Track your income and expenses meticulously, identifying areas where you can cut back and save more. Allocate funds towards essential expenses, debt repayment, and savings goals.

4. Build an Emergency Fund

Life is full of surprises, often financial ones. Establish an emergency fund that covers 3-6 months of living expenses. This safety net will provide financial security in case of unexpected events like job loss or medical emergencies.

5. Manage Debt Effectively

High-interest debt can hinder your progress towards financial stability. Prioritize debt repayment by creating a plan that focuses on paying down high-interest debts first. Explore strategies like debt consolidation or balance transfers to potentially lower interest rates.

6. Save and Invest Regularly

Saving and investing are crucial for long-term financial stability. Automate regular contributions to your savings and investment accounts. Explore different investment options based on your risk tolerance and financial goals.

7. Review and Adjust

Your financial plan is not static. Review and adjust it periodically to align with your evolving financial situation and goals. Life changes, market conditions fluctuate, and your priorities may shift, necessitating adjustments to your plan.

Budgeting for Success

Creating and sticking to a budget is the cornerstone of achieving financial stability. It’s the roadmap that guides your income flow, ensuring your money is working for you, not against you. Here’s how to craft a budget that sets you up for success:

1. Track Your Spending:

Before you can manage your money, you need a clear picture of where it’s going. Track your expenses for a month or two, noting down every dollar you spend. Utilize budgeting apps, spreadsheets, or even a simple notebook to categorize your spending (housing, groceries, transportation, entertainment, etc.).

2. Identify Needs vs. Wants:

Scrutinize your spending tracker. Differentiate between essential needs (rent, utilities, groceries) and discretionary wants (dining out, entertainment subscriptions). This exercise helps highlight areas where you can potentially cut back without drastically impacting your lifestyle.

3. Set Realistic Goals:

Establish clear financial goals for yourself. Are you aiming to build an emergency fund, pay off debt, save for a down payment, or invest for the future? Having tangible goals will motivate you to stick to your budget.

4. The 50/30/20 Rule (Or Find What Works For You):

Consider adopting a budgeting framework like the 50/30/20 rule:

- 50% of your after-tax income goes towards NEEDS.

- 30% goes towards WANTS.

- 20% is allocated for SAVINGS and DEBT REPAYMENT.

Adjust these percentages based on your individual circumstances and financial goals. Remember, the key is to find a system that’s sustainable for you.

5. Automate Your Savings:

Treat your savings like a non-negotiable expense. Set up automatic transfers from your checking account to your savings or investment accounts each month. This “pay yourself first” strategy ensures you’re consistently working towards your financial goals.

6. Regularly Review and Adjust:

Your financial situation and goals are likely to evolve over time. Make it a habit to revisit your budget monthly or quarterly. Track your progress, identify any areas needing adjustment, and celebrate your successes.

Saving and Investing Wisely

Saving and investing are essential components of achieving financial stability. They go hand-in-hand, working together to build a secure financial future.

Saving: Building a Strong Foundation

Saving forms the bedrock of financial stability. It provides a financial cushion for emergencies and unexpected expenses, preventing you from falling into debt. It also allows you to achieve short-term financial goals, such as buying a car or going on vacation.

Here are key saving strategies:

- Create a Budget: Track your income and expenses to identify areas where you can save.

- Set Savings Goals: Having specific targets (e.g., a down payment, emergency fund) can boost motivation.

- Automate Savings: Set up automatic transfers to your savings account to make saving consistent.

- Emergency Fund: Aim for 3-6 months of living expenses in an easily accessible account.

Investing: Growing Your Wealth Over Time

While saving safeguards your money, investing grows it. It helps outpace inflation and build long-term wealth, crucial for goals like retirement.

Key investing considerations:

- Start Early: The power of compounding yields greater returns over longer periods.

- Risk Tolerance: Understand your comfort level with investment risk; higher risk can mean higher potential returns but also greater potential losses.

- Diversification: Don’t put all your eggs in one basket. Spread investments across different asset classes (e.g., stocks, bonds, real estate) to mitigate risk.

- Investment Options: Explore options like stocks, bonds, mutual funds, ETFs, and real estate, understanding the risks and potential returns of each.

- Seek Professional Advice: Consider consulting a financial advisor for personalized guidance.

Reducing and Managing Debt

Debt can be a major obstacle to achieving financial stability. It can limit your financial freedom, increase your stress levels, and even damage your credit score. The good news is that it’s possible to reduce and manage your debt effectively, putting you back in control of your finances.

1. Create a Budget and Identify Spending Habits

The first step towards debt reduction is understanding where your money is going. Create a detailed budget that tracks your income and expenses. Analyze your spending habits to identify areas where you can cut back.

2. Prioritize Debt Repayment

Not all debts are created equal. Prioritize high-interest debts like credit card balances, as these accrue interest quickly. Consider using the debt snowball or debt avalanche methods to focus your repayment efforts.

3. Negotiate Lower Interest Rates

Don’t be afraid to contact your creditors and negotiate lower interest rates. Explain your financial situation and your commitment to repayment. A lower interest rate can save you money and help you pay off your debt faster.

4. Explore Debt Consolidation Options

If you have multiple debts, consolidating them into one loan with a lower interest rate can simplify repayment and potentially save you money. Explore options such as balance transfer credit cards or personal loans.

5. Seek Professional Financial Advice

If you’re struggling to manage your debt, don’t hesitate to seek professional help. A financial advisor can assess your situation, provide personalized advice, and help you develop a realistic debt management plan.

6. Avoid Taking On New Debt

While you’re working to reduce your existing debt, it’s crucial to avoid taking on new debt. Resist impulsive purchases and carefully consider the long-term financial implications before taking out any new loans.

7. Build an Emergency Fund

Having an emergency fund can prevent you from relying on credit cards in unexpected situations. Aim to save three to six months’ worth of living expenses to cushion against financial shocks and avoid accumulating further debt.

Building an Emergency Fund

One of the cornerstones of financial stability is having a safety net to catch you when unexpected expenses arise. This is where an emergency fund comes in. It’s a stash of money set aside specifically to cover unforeseen costs, preventing you from spiraling into debt or derailing your financial goals.

Why is an Emergency Fund Crucial?

Life is full of surprises, and not all of them are pleasant. Your car could break down, you might face unexpected medical bills, or you could lose your job. An emergency fund acts as a buffer against these financial shocks, providing peace of mind and preventing you from making rash financial decisions in times of stress.

How Much Should You Save?

A common guideline is to save three to six months’ worth of living expenses. This means having enough to cover essential costs like rent/mortgage, utilities, groceries, and debt payments for that duration. However, your ideal emergency fund size will depend on your individual circumstances, such as your job security, dependents, and risk tolerance.

Where to Keep Your Emergency Fund

Accessibility and safety are key considerations for your emergency fund. A high-yield savings account or a money market account are generally good options. These accounts offer easy access to your funds while still earning some interest.

Tips for Building Your Fund

- Start small: Even setting aside a small amount each week can add up over time.

- Automate your savings: Set up automatic transfers from your checking to your savings account.

- Cut back on expenses: Identify areas where you can reduce spending and redirect those funds to your emergency fund.

- Windfalls: Deposit any unexpected income, like tax refunds or bonuses, into your emergency fund.

Monitoring Your Progress

Tracking your financial journey is just as important as setting goals. It helps you stay motivated, identify areas for improvement, and make necessary adjustments along the way. Here’s how to effectively monitor your progress towards financial stability:

1. Regularly Review Your Budget and Expenses

Set aside time each month to review your budget and compare it to your actual spending. Identify any areas where you overspent or underspent. Analyze your spending habits to see if there are any recurring patterns or areas where you can cut back.

2. Track Your Net Worth

Your net worth is a key indicator of your financial health. Calculate it regularly by subtracting your liabilities (debts) from your assets (what you own). Seeing your net worth grow over time can be a great motivator.

3. Monitor Your Credit Score

A good credit score is crucial for obtaining loans and favorable interest rates. Regularly check your credit report for any errors and track your credit score to ensure it’s improving. Use free credit monitoring services or request a free report from credit bureaus annually.

4. Evaluate Your Progress Towards Goals

Are you on track to reach your savings goals? Are you paying down debt at a steady pace? Regularly assess your progress towards your financial goals and make adjustments as needed. Don’t be afraid to revise your goals if your circumstances change.

5. Celebrate Milestones

Acknowledge and celebrate your accomplishments along the way. Whether it’s paying off a credit card, reaching a savings milestone, or getting a raise, take the time to recognize your progress. This positive reinforcement can keep you motivated and engaged in your financial journey.

Adjusting Your Plan as Needed

Achieving financial stability isn’t about setting a rigid plan in stone and never deviating. Life is full of surprises, and your financial plan should be flexible enough to adapt.

Regularly Review and Reassess: Make it a habit to review your financial plan at least once a year, or more frequently if you experience significant life changes like a new job, marriage, or the birth of a child. Consider how these events might impact your income, expenses, and financial goals, and adjust your plan accordingly.

Don’t Be Afraid to Make Changes: If you find your current plan isn’t working, don’t hesitate to make adjustments. Perhaps your income has changed, your expenses have increased, or you’ve realized your initial goals were unrealistic. Be honest with yourself and adapt your plan to reflect your current situation and aspirations.

Expect the Unexpected: Life is unpredictable. Build an emergency fund to cover unforeseen expenses like medical bills, car repairs, or job loss. Having this financial safety net will prevent you from derailing your long-term goals when unexpected events occur.

Stay Informed and Seek Guidance: Keep yourself updated on financial news and trends that might impact your plan. Consider consulting with a financial advisor who can offer personalized guidance and help you navigate complex financial decisions.

Conclusion

In conclusion, achieving financial stability requires planning, budgeting, and wise financial decisions. By saving, investing, and avoiding unnecessary debt, individuals can secure their financial futures.

{kind=link}