Planning your finances for a major life change is crucial for a smooth transition. Learn how to budget, save, and strategize for events like marriage, buying a home, or starting a family in this comprehensive guide.

Setting Financial Goals

When preparing for a major life change, establishing clear financial goals is paramount. These goals act as your roadmap, guiding your financial decisions and ensuring you’re financially equipped to navigate the transition smoothly.

Start by identifying the financial implications of your upcoming life change. Are you getting married, buying a house, starting a family, or transitioning into retirement? Each milestone comes with its own set of financial considerations. For example:

- Marriage: Combining finances, planning for joint expenses, and aligning financial goals.

- Buying a Home: Saving for a down payment, closing costs, and ongoing expenses like mortgage payments, property taxes, and potential maintenance.

- Starting a Family: Budgeting for childcare, education, and increased living expenses associated with raising children.

- Retirement: Ensuring you have sufficient retirement savings to maintain your desired lifestyle without relying on a steady income.

Once you’ve outlined the financial implications, set specific, measurable, achievable, relevant, and time-bound (SMART) goals.

For instance, instead of a general goal like “save for a down payment,” a SMART goal would be: “Save $20,000 for a down payment on a house within the next three years.”

Break down larger goals into smaller, manageable milestones. This makes the goal less daunting and allows you to track your progress effectively. Celebrate your achievements along the way to stay motivated.

Creating a Savings Plan

A major life change often comes with significant financial implications. Whether you’re getting married, having a baby, starting a business, or retiring, having a solid savings plan is crucial to navigate the transition smoothly and achieve your financial goals.

Here’s a step-by-step guide to help you create an effective savings plan:

1. Define Your Financial Goals:

Start by identifying your financial objectives for this life change. Be specific about what you want to achieve and set realistic timelines. For example, if you’re saving for a down payment on a house, determine how much money you need and when you aim to purchase the property.

2. Assess Your Current Financial Situation:

Take stock of your income, expenses, assets, and debts. Track your spending patterns to identify areas where you can cut back and free up more cash for savings. Creating a budget will give you a clear picture of your finances.

3. Determine Your Savings Target:

Based on your financial goals and the timeline you’ve set, calculate the total amount you need to save. Break down this target into smaller, manageable monthly or weekly savings goals.

4. Automate Your Savings:

Set up automatic transfers from your checking account to your savings account each month. This “pay yourself first” approach ensures consistent saving and prevents you from accidentally spending the money allocated for your goals.

5. Explore Different Savings Options:

Research various savings accounts, money market accounts, or certificates of deposit (CDs) to find the best interest rates and terms that align with your needs and risk tolerance.

6. Reduce Expenses and Increase Income:

Look for opportunities to cut down on unnecessary expenses. Consider downsizing your lifestyle, negotiating lower bills, or finding more affordable alternatives. Additionally, explore ways to increase your income through a side hustle, freelance work, or asking for a raise.

7. Track Your Progress and Adjust Accordingly:

Regularly review your savings plan and monitor your progress toward your goals. Adjust your savings targets, timelines, or strategies as needed, especially if your financial situation or goals change.

Finding Extra Money to Save

Major life changes often come with major expenses. Whether you’re planning a wedding, starting a family, buying a home, or going back to school, it’s crucial to ensure your finances are ready for the transition. A key part of this preparation is finding extra money to save. Here’s how:

1. Track Your Spending and Identify Areas to Cut Back

You can’t manage what you don’t measure. Start by tracking your spending for a month or two to get a clear picture of where your money is going. Use a budgeting app, a spreadsheet, or a notebook—whatever method works best for you. Once you have a handle on your spending habits, identify areas where you can potentially cut back.

2. Reduce Non-Essential Expenses

Take a close look at your spending habits and pinpoint non-essential expenses that you can temporarily or permanently reduce. This could include:

- Dining out

- Entertainment subscriptions

- Clothing purchases

- Expensive hobbies

Remember, even small cuts can make a big difference over time.

3. Explore Additional Income Sources

Boosting your income can significantly accelerate your savings efforts. Consider these options:

- Freelancing or Gig Work: Utilize your skills to earn extra income through freelance platforms or gig economy jobs.

- Selling Unwanted Items: Declutter your home and sell unused items online or at consignment stores.

- Part-Time Employment: If your schedule allows, consider a part-time job to supplement your income.

4. Automate Your Savings

Make saving automatic by setting up recurring transfers from your checking account to your savings account. This way, you’ll consistently contribute to your savings goals without having to think about it.

5. Review and Negotiate Bills

Regularly review your bills, such as your internet, phone, and insurance plans. Contact providers to inquire about potential discounts or negotiate lower rates. You might be surprised by the savings you can uncover.

Cutting Expenses to Save More

When preparing for a major life change, such as moving, changing careers, or starting a family, building a strong financial foundation is crucial. One of the most effective ways to do this is by cutting expenses and boosting your savings. This might feel daunting, but identifying areas where you can reduce spending can significantly impact your financial well-being.

Review Your Budget and Identify Non-Essential Spending

Begin by closely examining your current spending habits. Track your income and expenses for a month or two to understand where your money is going. Once you have a clear picture, categorize your expenses as essential and non-essential.

- Essential expenses are unavoidable costs like rent/mortgage payments, utilities, groceries, and transportation.

- Non-essential expenses are discretionary spending on things like dining out, entertainment, subscriptions, and luxury items.

Find Savings Within Your Essential Expenses

While it might seem difficult to reduce essential expenses, there are often opportunities for savings. Consider these strategies:

- Negotiate lower bills: Contact service providers for utilities, internet, and insurance to inquire about discounts or lower rates.

- Reduce housing costs: Explore downsizing, renting out a spare room, or relocating to a more affordable area if feasible.

- Shop smarter for groceries: Plan meals, utilize coupons, buy in bulk, and explore discount grocery stores.

- Minimize transportation costs: Opt for public transport, carpool, bike, or walk when possible. Explore fuel-efficient vehicle options if you need a car.

Cut Back on Non-Essential Expenses

Reducing or eliminating non-essential expenses can free up a significant portion of your income. Here are some areas to consider:

- Limit dining out and takeout: Cook more meals at home and explore affordable meal planning strategies.

- Evaluate subscriptions and memberships: Cancel or pause subscriptions you rarely use, such as streaming services, gym memberships, or magazine subscriptions.

- Find free or low-cost entertainment: Explore free community events, take advantage of parks and libraries, and look for discounts on entertainment options.

- Delay gratification for big purchases: Before making significant purchases, give yourself time to consider if it’s a need or a want. Delaying gratification can help you avoid impulsive spending and prioritize savings.

Using High-Interest Accounts

When planning your finances for a major life change, maximizing your savings is crucial. A high-interest savings account can be a valuable tool in this endeavor. Unlike traditional savings accounts that offer minimal returns, high-interest accounts provide a higher annual percentage yield (APY), allowing your money to grow at an accelerated rate.

Here’s how using high-interest accounts can benefit you:

- Increased Savings Growth: The higher APY means your savings will accumulate interest more quickly, helping you reach your financial goals faster.

- Compound Interest: High-interest accounts often compound interest daily or monthly, meaning you earn interest on both your initial deposit and any accumulated interest. This compounding effect can significantly boost your savings over time.

- Liquidity and Accessibility: While some high-yield options like certificates of deposit (CDs) have restrictions on withdrawals, many high-interest savings accounts offer flexibility. You can typically access your funds when needed, though some accounts may have a limited number of free withdrawals per month.

When choosing a high-interest account:

- Compare APYs: Shop around and compare rates from different banks and credit unions. Online banks often offer the most competitive APYs.

- Read the Fine Print: Pay attention to fees, minimum balance requirements, and any conditions that could impact your interest earnings.

- Consider Your Needs: Determine how important liquidity is to you. If you anticipate needing frequent access to your savings, prioritize an account with flexible withdrawal options.

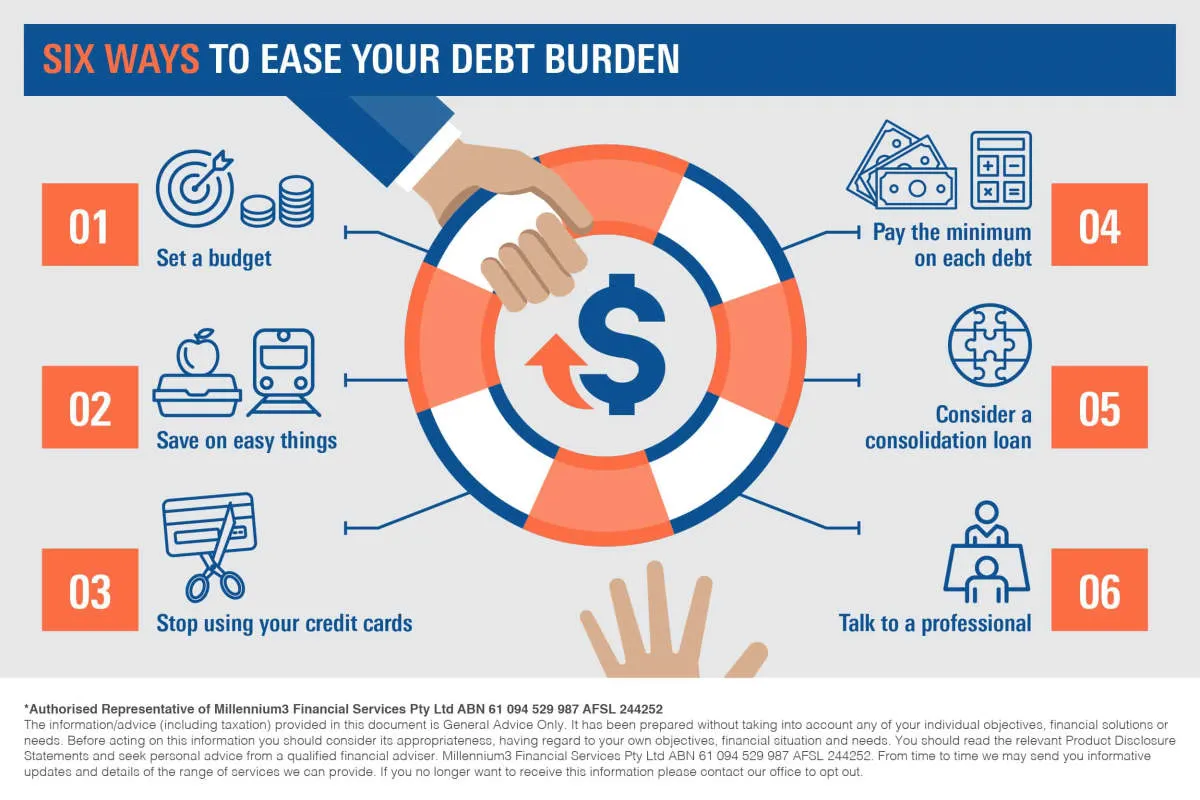

Avoiding Unnecessary Debt

Major life changes often come with major expenses. Whether you’re getting married, having a baby, or moving across the country, it’s easy to find yourself swiping your credit card more than usual. However, starting a new chapter with a pile of debt can create unnecessary stress and hinder your financial progress. Here’s how to navigate major life events while keeping debt at bay:

1. Plan Ahead and Budget Realistically

Don’t wait until the last minute to figure out your finances. As soon as you know a major life change is on the horizon, start planning. Research potential costs and create a realistic budget. Factor in unexpected expenses and add a buffer for unforeseen circumstances.

2. Differentiate Between Needs and Wants

It’s easy to get caught up in the excitement of a major life change and convince yourself that “wants” are actually “needs.” Take a step back and honestly assess your priorities. Do you need the extravagant wedding venue, or will a smaller, more intimate location suffice? Can you purchase a used car instead of a brand new one? Making conscious spending choices can save you a significant amount of money and prevent unnecessary debt.

3. Explore Alternative Options

Get creative and think outside the box to find cost-effective solutions. Can you DIY your wedding decorations or find gently used furniture for your new home? Consider downsizing or selling items you no longer need to generate extra cash.

4. Be Prepared to Make Sacrifices

Avoiding unnecessary debt often requires making sacrifices. This might mean postponing a large purchase, taking on a side hustle for extra income, or making temporary lifestyle adjustments. Remember, the short-term sacrifices you make can lead to long-term financial stability and peace of mind.

5. Seek Professional Financial Advice

If you’re struggling to manage your finances or feel overwhelmed by the prospect of a major life change, don’t hesitate to seek guidance from a financial advisor. They can provide personalized advice, help you create a solid financial plan, and offer strategies for avoiding debt.

Tracking Your Savings Progress

Keeping tabs on your savings is essential for staying motivated and making sure you’re on track to meet your financial goals. Here’s how to effectively track your savings progress:

1. Choose a Tracking Method

Find a system that works best for you. This could be:

- Spreadsheet: Create a simple spreadsheet to track your income, expenses, and savings goals.

- Budgeting Apps: Many apps are available that automatically track your finances and provide visual representations of your progress.

- Notebook: If you prefer pen and paper, a dedicated notebook can be an effective way to track your savings.

2. Set Realistic Savings Goals

Break down your larger savings goal into smaller, more manageable milestones. This will make the process feel less daunting and allow you to celebrate your achievements along the way.

3. Regularly Review and Adjust

Set aside time each month to review your savings progress. Are you on track to meet your goals? Do you need to adjust your savings plan? Regularly reviewing your progress allows you to make necessary adjustments and stay on course.

4. Visualize Your Progress

Visual aids can be a powerful motivator. Use charts, graphs, or even a simple visual representation of your goal to see how far you’ve come and stay inspired.

5. Celebrate Milestones

Recognize and celebrate your achievements along the way. This will help you stay motivated and reinforce positive financial habits.

Reaching Your Life Change Goal

You’ve crafted a solid financial plan, budgeted meticulously, and prepared for the unexpected. Now, it’s time to focus on the driving force behind all your hard work: reaching your life change goal.

Whether it’s moving to a new city, starting a family, switching careers, or pursuing a long-held dream, keep that goal at the forefront of your mind.

Staying Motivated and Adaptable

Major life changes are marathons, not sprints. There will be challenges and setbacks. Here’s how to stay on track:

- Visualize your success: Regularly remind yourself of the reasons behind your goal and the positive impact it will have.

- Break down the journey: Divide your larger goal into smaller, manageable milestones. Celebrate each achievement to stay motivated.

- Embrace flexibility: Life is unpredictable. Be prepared to adjust your financial plan and timeline as needed, without losing sight of your ultimate goal.

- Seek support: Share your journey with loved ones, mentors, or support groups. Their encouragement and advice can prove invaluable, especially during challenging times.

Conclusion

Planning your finances is crucial for navigating major life changes effectively and with confidence. Take proactive steps, seek professional advice, and stay adaptable for a secure financial future.

{kind=link}