Learn how to craft a thorough financial plan to secure your future financial stability in our guide on “How to Create a Comprehensive Financial Plan.”

Importance of a Financial Plan

A financial plan is a roadmap that outlines your financial goals and provides a structured approach to achieve them. It acts as a guide for your financial decisions, helping you prioritize spending, save effectively, and make informed investments. Having a well-defined financial plan offers numerous benefits:

1. Goal Clarity and Achievement:

A financial plan begins with identifying your short-term and long-term financial goals. Whether it’s buying a home, funding your retirement, or saving for your child’s education, having clear goals allows you to create a targeted plan and track your progress.

2. Controlled Spending and Debt Management:

A financial plan helps you understand your cash flow – your income and expenses. By tracking your spending habits and creating a budget, you can identify areas to reduce unnecessary expenses and free up more money for savings and investments. This control over your finances is crucial for effective debt management and building a strong financial foundation.

3. Strategic Investing and Wealth Building:

A financial plan guides your investment decisions based on your risk tolerance, time horizon, and financial goals. By aligning your investments with your plan, you can potentially maximize returns and build wealth over time. A well-diversified investment portfolio, as recommended in most financial plans, can help mitigate risks and enhance long-term financial growth.

4. Prepared for Emergencies and the Unexpected:

Life is full of uncertainties, and financial emergencies can arise unexpectedly. A comprehensive financial plan includes provisions for an emergency fund, covering three to six months of living expenses. This safety net provides financial security and peace of mind during unexpected events like job loss, medical emergencies, or unforeseen repairs.

5. Secure Future and Retirement Planning:

Retirement might seem distant, but planning for it early is crucial. A financial plan helps you determine how much you need to save for a comfortable retirement and outlines strategies to achieve your retirement savings goals. By starting early and consistently investing, you can benefit from the power of compounding and secure your financial future.

Assessing Your Current Financial Situation

The first step in crafting a robust financial plan is gaining a crystal-clear understanding of where you stand financially right now. This means taking a comprehensive inventory of your assets, debts, income, and expenses. While it might seem daunting, this process is crucial in identifying areas of strength and weakness, ultimately setting the foundation for your financial journey ahead.

Income & Expenses: Mapping Your Cash Flow

Start by tracking your income from all sources – salary, investments, rental income, etc. Be thorough and include every penny coming in. Next, create a detailed list of your monthly expenses. Categorize them as fixed (rent, utilities) and variable (groceries, entertainment). This exercise will reveal your average monthly cash flow – the difference between what you earn and spend. A positive cash flow provides more financial flexibility, while a negative one necessitates adjustments.

Assets & Debts: Understanding Your Net Worth

List all your assets – savings, investments, retirement accounts, property, and valuable possessions. Then, compile your debts – mortgages, loans, credit card balances. Calculate your net worth by subtracting your total liabilities from your total assets. This figure provides a snapshot of your overall financial health at this moment.

Financial Goals: A Compass for Your Journey

With a firm grasp of your current financial standing, you can begin to define your short-term and long-term financial goals. Are you aiming to purchase a home, retire early, or secure your children’s education? Defining these objectives will guide your financial decisions and motivate you to stay on track with your plan.

Setting Short and Long-Term Goals

A crucial aspect of financial planning involves setting clear and achievable financial goals. These goals act as your roadmap, guiding your financial decisions and helping you measure progress along the way. They provide a clear picture of what you want to achieve financially and how you plan to get there.

Short-Term Goals

Short-term goals are achievable within a year or less. They lay the foundation for long-term aspirations and often involve:

- Building an emergency fund (3-6 months of living expenses)

- Paying off high-interest debt (credit cards, payday loans)

- Saving for a down payment on a car or home

- Funding a vacation or special event

Long-Term Goals

Long-term goals typically span several years or even decades. They require a long-term perspective and disciplined saving and investing strategies. Some common long-term goals include:

- Retirement planning

- Funding a child’s education

- Purchasing a home

- Starting a business

The Importance of Goal Alignment

Your short and long-term goals should work in harmony. For instance, consistently saving a portion of your income (short-term goal) can set you on the path towards a comfortable retirement (long-term goal).

SMART Goals

To maximize your chances of success, ensure your goals are SMART:

- Specific: Clearly define what you want to achieve (e.g., save $5,000 for a down payment).

- Measurable: Quantify your goals with specific amounts (e.g., save $500 per month).

- Achievable: Set realistic goals considering your income and expenses.

- Relevant: Align goals with your values and aspirations.

- Time-bound: Set a deadline for achieving each goal.

Budgeting and Saving Strategies

A comprehensive financial plan necessitates a keen understanding and implementation of effective budgeting and saving strategies. These strategies provide a roadmap for managing your money, ensuring you allocate funds wisely to achieve your financial goals.

Creating a Realistic Budget

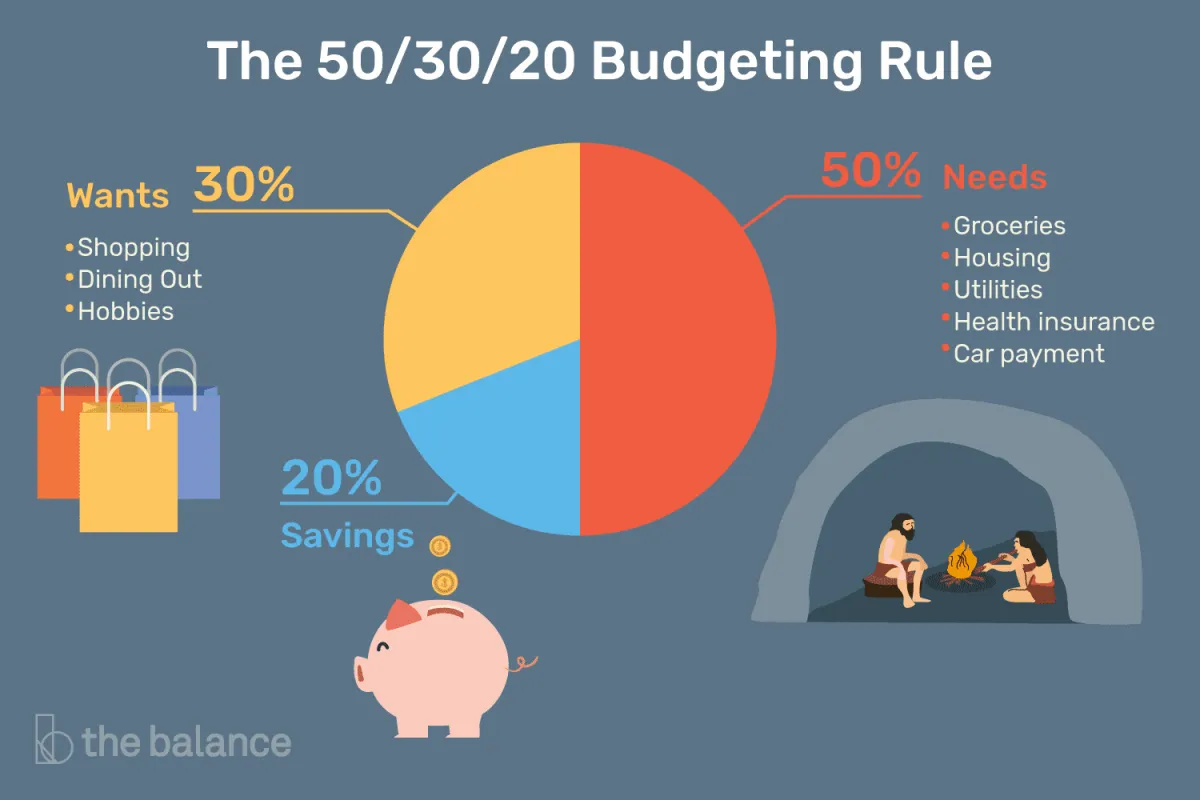

Start by tracking your income and expenses. Analyze your spending habits to identify areas where you can cut back. Categorize your expenses (e.g., housing, transportation, food) and allocate a specific amount for each. Be realistic and factor in occasional expenses like vacations or gifts. There are various budgeting methods, such as the 50/30/20 rule or zero-based budgeting, that you can explore to find the one that suits your needs.

Setting Clear Saving Goals

Define your short-term and long-term financial objectives. Whether it’s saving for a down payment on a house, funding your retirement, or building an emergency fund, having clear goals will keep you motivated and disciplined in your saving efforts.

Automating Savings

Leverage technology to make saving effortless. Set up automatic transfers from your checking to your savings account each month. This “pay yourself first” approach ensures consistent savings without requiring constant manual effort.

Exploring Saving Options

Research different savings options to find those that align with your financial goals and risk tolerance. Consider high-yield savings accounts, money market accounts, certificates of deposit (CDs), or even investing in low-risk bonds for potentially higher returns.

Regularly Review and Adjust

Your financial situation can change over time, so it’s crucial to review your budget and savings goals periodically. Adjust your plan as needed to reflect changes in income, expenses, or financial priorities. Flexibility and adaptability are key to successful long-term financial management.

Investment Planning

Investment planning is a crucial component of a comprehensive financial plan, aiming to grow your wealth over time and achieve your long-term financial goals, whether it’s retiring comfortably, purchasing a home, or funding your children’s education.

Here are key steps to consider in investment planning:

1. Define Your Financial Goals:

Clearly articulate your financial objectives, including the amount of money you need, the timeframe for achieving them, and the purpose of each goal. This will guide your investment strategy and risk tolerance.

2. Assess Your Risk Tolerance:

Determine your comfort level with investment risk. Are you risk-averse, seeking stable but potentially lower returns, or are you comfortable with higher-risk investments that offer greater potential for growth? Your risk tolerance will shape your asset allocation.

3. Determine Your Investment Horizon:

Your investment horizon is the length of time you plan to hold your investments. Longer investment horizons generally allow for greater risk-taking, as you have more time to recover from market fluctuations.

4. Choose Your Investment Strategy:

There are various investment strategies, from passive investing, such as index funds and ETFs, to active investing, like stock picking or managed funds. Your chosen strategy should align with your risk tolerance, investment horizon, and financial goals.

5. Diversify Your Portfolio:

Don’t put all your eggs in one basket. Diversification involves spreading your investments across different asset classes (stocks, bonds, real estate, etc.) and sectors to reduce overall risk. A well-diversified portfolio can help mitigate losses in one area with gains in another.

6. Regular Monitoring and Rebalancing:

Regularly review your investment portfolio’s performance against your goals and risk tolerance. Rebalance your portfolio as needed to maintain your desired asset allocation.

Retirement Planning

Retirement might seem far off, but planning for it early is crucial for financial security. Here’s what to consider:

1. Determine Your Retirement Goals

Start by envisioning your ideal retirement lifestyle. Where do you want to live? How do you want to spend your time? Quantify your vision by estimating how much annual income you’ll need to support your desired lifestyle.

2. Estimate Retirement Expenses

While some expenses might decrease in retirement (like commuting costs), others could rise (like healthcare). Carefully project your anticipated living expenses during retirement, taking inflation into account.

3. Choose Retirement Savings Plans

Explore different retirement savings options:

- Employer-Sponsored Plans: Take advantage of 401(k)s or similar plans, especially if your employer offers matching contributions.

- Individual Retirement Accounts (IRAs): Contribute to Traditional or Roth IRAs to grow your savings tax-advantaged.

- Other Investment Accounts: Consider taxable brokerage accounts for additional retirement savings.

4. Determine Your Retirement Savings Rate

The earlier you start saving, the less you’ll need to contribute each month. Use online retirement calculators to determine how much you should be saving regularly to reach your goals.

5. Review and Adjust Regularly

As you progress through life, your financial situation and goals may change. Review your retirement plan annually, or whenever significant life events occur, and adjust your savings and investment strategy accordingly.

Estate Planning

Estate planning is the process of arranging for the management and distribution of your assets after your death. It’s a crucial aspect of financial planning, ensuring your loved ones are taken care of and your wishes are honored. Here are key elements to consider:

Will

A will is a legal document outlining how you want your assets distributed upon your death. Without a will, your estate will be divided according to state law, which may not align with your wishes.

Trusts

Trusts can be used to manage assets for beneficiaries, potentially reducing estate taxes and avoiding probate. Different types of trusts serve various purposes, so consult with an estate planning attorney to determine the best fit for your situation.

Beneficiary Designations

Ensure your retirement accounts (401(k), IRA), life insurance policies, and other financial accounts have up-to-date beneficiary designations. This ensures these assets transfer directly to your chosen beneficiaries, bypassing probate.

Power of Attorney

A durable power of attorney allows a designated person to make financial and legal decisions on your behalf if you become incapacitated. This ensures your affairs are managed according to your wishes, even if you are unable to make decisions yourself.

Healthcare Directive

A healthcare directive outlines your wishes for medical treatment if you are unable to communicate them. This can include a living will, which specifies end-of-life care preferences, and a healthcare proxy, designating someone to make medical decisions on your behalf.

Don’t delay estate planning. Life is unpredictable, and having a plan in place provides peace of mind for both you and your loved ones. Consult with a qualified estate planning attorney to create a plan tailored to your specific needs and circumstances.

Reviewing and Updating Your Plan

A financial plan isn’t something you create once and forget about. Life throws curveballs, your goals evolve, and the economic environment shifts. Regularly reviewing and updating your plan is crucial for staying on track and achieving your financial aspirations.

How Often Should You Review?

Aim for at least an annual review of your financial plan. However, certain life events might necessitate more frequent check-ins:

- Marriage or divorce

- Birth or adoption of a child

- Job loss or significant salary change

- Receiving an inheritance

- Major market downturns

Key Areas to Focus On:

During your review, consider these aspects of your plan:

1. Goals:

Are your short-term and long-term goals still the same? Have your priorities changed? Adjust your plan to reflect your current aspirations.

2. Net Worth:

Calculate your net worth (assets minus liabilities) to track your financial progress. Is your net worth growing as expected? Identify areas for improvement.

3. Budget:

Review your income and expenses. Are you sticking to your budget? Do you need to adjust spending or saving habits based on changes in your income or expenses?

4. Investments:

Assess the performance of your investments. Are they aligned with your risk tolerance and time horizon? Rebalance your portfolio as needed to stay on track.

5. Retirement Planning:

Are you saving enough for retirement? Use retirement calculators to estimate your future needs and make adjustments to your contributions.

6. Estate Planning:

Review your will, beneficiaries on accounts, and insurance policies. Ensure they are up-to-date and reflect your current wishes.

Seeking Professional Guidance:

Consider consulting with a certified financial planner for a comprehensive review and personalized advice. They can provide insights into market trends, tax optimization strategies, and investment opportunities that align with your goals.

Conclusion

Establishing a comprehensive financial plan is crucial for achieving your long-term monetary goals. By outlining your objectives, creating a budget, investing wisely, and regularly reviewing and adjusting your plan, you can secure a stable financial future.

{kind=link}