In the quest for financial independence, reaching financial freedom before the age of 40 is a challenging yet achievable goal. Discover the essential steps and strategies to pave your way to a secure financial future in this comprehensive guide.

Defining Financial Freedom

Financial freedom means something different to everyone. It’s not just about being rich; it’s about having control over your finances and enough money to cover your expenses without constant worry. This could mean being debt-free, having a comfortable emergency fund, and being able to pursue your passions without financial constraints.

For some, financial freedom might mean early retirement, while for others, it might mean the ability to start a business or work fewer hours. Ultimately, it’s about aligning your money with your values and creating a life where you have the flexibility and resources to pursue what matters most to you.

Setting Clear Financial Goals

The cornerstone of achieving financial freedom, especially by a younger age like 40, is establishing crystal clear financial goals. This isn’t about vaguely wanting to be “comfortable” or having “enough” money. It’s about defining exactly what you want your financial future to look like and putting concrete figures and deadlines to those aspirations.

Here’s how to set effective financial goals:

1. Dream Big, Then Break It Down:

Start by envisioning your ideal life at 40. Do you want to own a home outright? Retire early and travel? Be financially secure enough to pursue creative passions? Once you have the big picture, break it down into smaller, actionable financial goals:

- Short-Term Goals (1-2 years): Building an emergency fund, paying off a specific credit card, saving for a down payment.

- Mid-Term Goals (3-5 years): Paying off student loans, investing a certain amount in the stock market, purchasing a rental property.

- Long-Term Goals (5+ years): Achieving financial independence, early retirement, having a fully funded retirement account.

2. Make Goals Specific and Measurable:

A goal like “save more money” is too vague. Instead, aim for something like: “Save $10,000 for a down payment in the next 24 months.”

3. Set Realistic Yet Challenging Goals:

Be ambitious but grounded. Consider your income, expenses, and lifestyle. Your goals should push you while remaining attainable.

4. Put it in Writing and Track Your Progress:

Write down your goals and review them regularly. Use budgeting apps, spreadsheets, or a financial journal to track your progress. Seeing how far you’ve come can be incredibly motivating.

Creating a Realistic Budget

Achieving financial freedom before 40 starts with a solid financial plan, and at the heart of any good plan lies a realistic budget. This isn’t about restriction; it’s about understanding where your money goes and making it work harder for you.

Here’s how to build a budget that empowers you towards financial freedom:

1. Track Your Spending:

You can’t manage what you don’t measure. Use budgeting apps, spreadsheets, or even a notebook to track every dollar you spend for a month. Categorize your spending (housing, transportation, food, entertainment, etc.) to understand your spending patterns.

2. Identify Needs vs. Wants:

Differentiate between essential expenses (needs) and discretionary spending (wants). While wants are enjoyable, prioritizing needs ensures you cover essential costs first.

3. Set Realistic Goals:

Financial freedom means different things to different people. Define what it means for you, whether it’s early retirement, starting a business, or financial security. Having clear goals provides motivation and direction for your budget.

4. Automate Savings:

Treat savings like a non-negotiable expense. Set up automatic transfers from your checking account to your savings and investment accounts each month. This “pay yourself first” approach ensures you prioritize your financial goals.

5. Review and Adjust Regularly:

Your budget isn’t static; it needs regular review and adjustments. Life changes, income fluctuates, and goals evolve. Revisit your budget monthly or quarterly to make necessary tweaks and ensure it aligns with your financial aspirations.

Increasing Your Income

Increasing your income is a crucial step towards achieving financial freedom, especially if you aim to do so before 40. A higher income provides more resources to invest, pay off debt faster, and build a solid financial foundation. Here are some effective strategies to boost your earning potential:

1. Enhance Your Skills and Knowledge:

In today’s competitive job market, continuous learning is essential. Consider investing in your professional development through:

- Taking relevant courses or certifications to acquire in-demand skills.

- Attending workshops and conferences to stay updated on industry trends.

- Pursuing higher education, such as a master’s degree, if it aligns with your career goals.

2. Negotiate Your Salary:

Don’t be afraid to negotiate your salary when starting a new job or during performance reviews. Research industry benchmarks, quantify your accomplishments, and present a compelling case for your worth. Remember, your salary is a reflection of your value to the company.

3. Explore Side Hustles:

The gig economy offers numerous opportunities to generate extra income. Consider these side hustle ideas:

- Freelancing your skills in writing, graphic design, web development, or other areas.

- Driving for a ride-sharing service or delivering food or groceries.

- Selling handmade goods or used items online through platforms like Etsy or eBay.

4. Seek Career Advancement:

Position yourself for promotions and raises by consistently exceeding expectations in your current role. Take on challenging projects, demonstrate initiative, and build strong relationships with your colleagues and supervisors.

5. Invest in Your Network:

Networking can open doors to new opportunities and increase your earning potential. Attend industry events, connect with professionals on LinkedIn, and nurture your existing relationships. You never know where your next lead or job offer might come from.

Saving and Investing Wisely

Saving and investing wisely are the cornerstones of achieving financial freedom at any age, especially before 40. This involves a two-pronged approach: accumulating your funds and putting them to work for you.

Building a Strong Savings Habit

Start by establishing a realistic budget to track income and expenses. Identify areas where you can cut back and redirect funds towards savings. Aim to save at least 20% of your income, although the more you can save early on, the more time your money has to grow.

- Automate Savings: Set up automatic transfers to your savings or investment accounts. This “pay yourself first” strategy ensures consistent saving.

- Emergency Fund: Prioritize building a 3-6 month emergency fund. This safety net prevents derailing your financial goals due to unexpected events.

- High-Yield Savings: Maximize your savings growth by opting for high-yield savings accounts or money market accounts.

Investing for Long-Term Growth

Investing is essential for outpacing inflation and growing your wealth over time. Time is your greatest asset when you’re young, allowing you to ride out market fluctuations and benefit from compound growth.

- Start Early: Even small investments in your 20s and 30s can significantly impact your long-term financial well-being.

- Diversify Investments: Don’t put all your eggs in one basket. Spread your investments across different asset classes like stocks, bonds, and real estate to manage risk.

- Retirement Accounts: Take advantage of tax-advantaged retirement accounts like 401(k)s and IRAs. Employer-sponsored plans often come with matching contributions, which is essentially free money.

- Seek Professional Advice: Consider consulting with a financial advisor to create a personalized investment strategy based on your goals, risk tolerance, and time horizon.

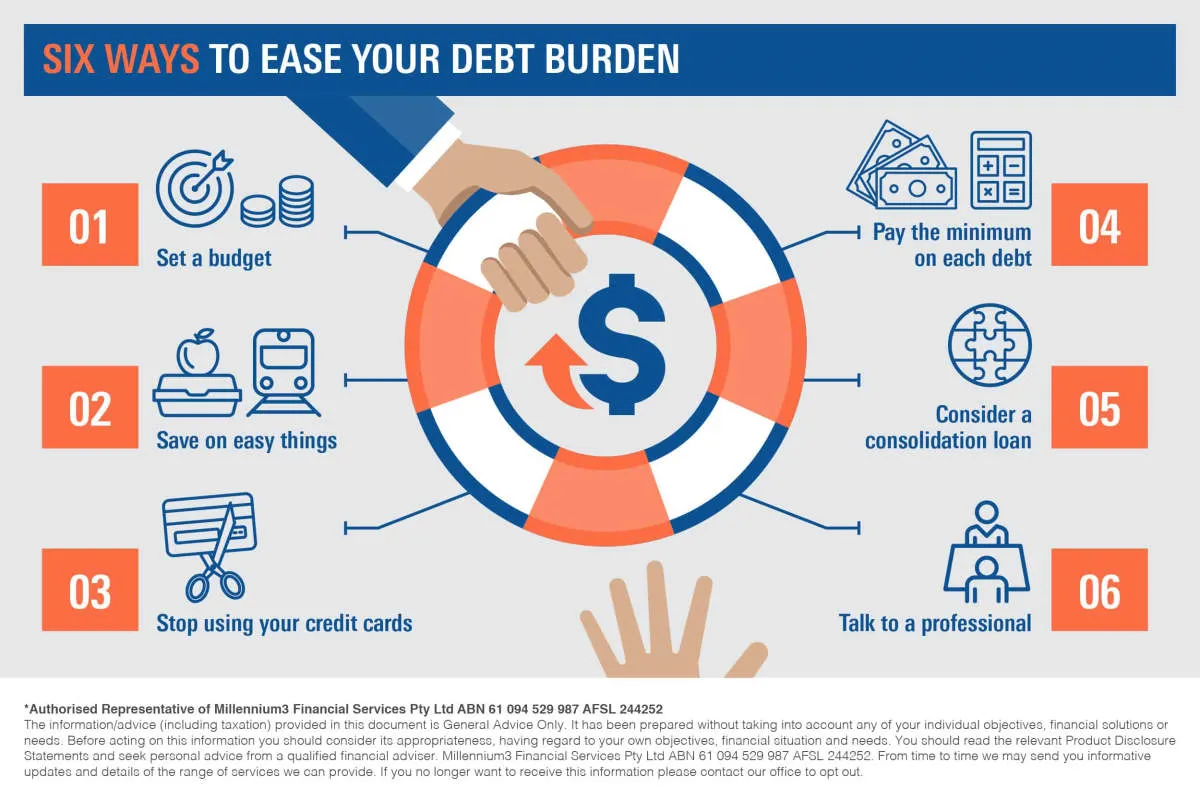

Avoiding Unnecessary Debt

One of the biggest obstacles to financial freedom is unnecessary debt. It’s easy to fall into the trap of living beyond your means, especially when credit is readily available. However, carrying high-interest debt can significantly hinder your ability to save and invest for the future. Here’s how to avoid unnecessary debt and stay on track towards financial freedom:

1. Differentiate Between Needs and Wants

Before making a purchase, ask yourself if it’s a necessity or simply something you desire. Needs are essentials like housing, food, and basic transportation. Wants are everything else. While it’s fine to indulge in wants occasionally, prioritize your spending on needs and make conscious decisions about your wants.

2. Live Below Your Means

This might seem obvious, but it’s crucial. Create a budget and track your expenses diligently. Aim to spend less than you earn and allocate the difference towards savings and investments. Consider downsizing your lifestyle if your expenses consistently outweigh your income.

3. Build an Emergency Fund

Unexpected expenses will arise, and having an emergency fund can prevent you from relying on credit cards. Aim to save three to six months’ worth of living expenses in a readily accessible account. This safety net provides a buffer against financial shocks and helps you avoid going into debt for unexpected events.

4. Resist Impulse Purchases

Impulse purchases can quickly derail your budget. Implement strategies to curb impulsive spending, such as waiting 24 hours before making a significant purchase. This cooling-off period allows you to carefully consider the purchase and decide if it aligns with your financial goals.

5. Utilize Credit Cards Strategically

Credit cards can be valuable tools for building credit and earning rewards, but only if used responsibly. Pay your balance in full and on time each month to avoid accumulating high-interest debt. If you find yourself struggling to manage credit card spending, consider leaving them at home to prevent impulsive purchases.

6. Explore Alternative Transportation

Car payments, insurance, and maintenance can put a significant dent in your budget. Explore alternative transportation options like public transportation, biking, or walking when possible. If you live in an area where owning a car is a necessity, consider purchasing a reliable used car instead of a brand-new vehicle.

Building Multiple Income Streams

One of the most effective strategies to achieve financial freedom, especially before 40, is to build multiple income streams. Relying solely on a single source of income can be risky and limit your earning potential. Diversifying your income sources can provide financial security, accelerate your wealth-building journey, and bring you closer to your financial goals.

Why Multiple Income Streams Matter:

- Financial Security: If one income stream dries up (e.g., job loss), you have others to fall back on.

- Accelerated Wealth Building: More income streams mean more money to invest and grow your wealth faster.

- Faster Debt Reduction: Use additional income to pay down debt quicker and reduce interest payments.

- Increased Flexibility and Freedom: Multiple income streams can provide the financial flexibility to pursue passions, take risks, or retire early.

Ideas for Building Income Streams:

The key is to leverage your skills, interests, and resources. Here are some potential avenues:

- Invest in Dividend-Paying Stocks: Earn passive income through dividends while holding onto your investments.

- Real Estate Investing: Generate rental income or explore house flipping for potential profits.

- Start a Side Hustle or Business: Turn your skills or hobbies into a source of income (e.g., freelance writing, online tutoring, crafts, etc.).

- Create and Sell Digital Products: Offer online courses, ebooks, templates, or other digital resources.

- Peer-to-Peer Lending: Lend small amounts of money to borrowers and earn interest payments.

- Rent Out Assets: Rent out a spare room, parking space, or even your car when not in use.

Staying Disciplined and Focused

Achieving financial freedom before 40 requires an unwavering commitment to your financial goals. Life is full of distractions and temptations that can easily derail your progress. Here are some key strategies to stay disciplined and focused on your path to financial independence:

1. Define Your “Why”

Clearly articulate why financial freedom is important to you. Is it early retirement, the ability to pursue your passions, or securing your family’s future? A strong “why” will fuel your motivation when you face challenges or feel tempted to stray from your plan.

2. Set SMART Goals

Vague aspirations won’t cut it. Set Specific, Measurable, Achievable, Relevant, and Time-Bound goals. Instead of “save more money,” aim for “save $500 per month towards a down payment on a rental property within 3 years.”

3. Track Your Progress and Reward Yourself

Regularly monitor your income, expenses, savings, and investments. Use budgeting apps, spreadsheets, or financial software to stay organized. Celebrate milestones along the way to stay motivated. Reward yourself without derailing your progress – think a nice dinner out, not a spontaneous shopping spree.

4. Automate Your Savings and Investments

Make saving and investing automatic. Set up regular transfers from your checking account to your savings, investment, and retirement accounts. This “pay yourself first” approach ensures consistent progress and reduces the temptation to spend the money elsewhere.

5. Surround Yourself with Support

Share your goals with supportive friends, family, or a financial advisor. Surround yourself with people who encourage your financial journey. Consider joining online communities or forums focused on financial independence for additional support and motivation.

6. Practice Delayed Gratification

Resist the urge for instant gratification. Before making a purchase, especially a large one, ask yourself if it aligns with your long-term goals. Can you wait, save up, or find a more cost-effective alternative?

Conclusion

In conclusion, following a structured financial plan, investing wisely, and prioritizing savings are key steps to achieve financial freedom before the age of 40. It is important to start early and stay consistent in your financial habits for long-term success.

{kind=link}