Planning for retirement is crucial to ensure a secure future. Discover essential tips and strategies to help you manage your finances and achieve peace of mind as you prepare for your retirement years.

Importance of Retirement Planning

Retirement planning is not just about saving money; it’s about securing your financial freedom and ensuring a comfortable lifestyle after you leave the workforce. Here’s why it’s crucial:

- Financial Security: Retirement planning provides a financial safety net, allowing you to maintain your lifestyle without relying solely on social security or family support.

- Inflation Protection: Planning helps you stay ahead of inflation, ensuring your savings retain their purchasing power over time.

- Healthcare Costs: As you age, healthcare expenses tend to rise. Retirement planning allows you to allocate funds for potential medical needs.

- Pursuing Passions: Retirement should be about enjoying life. Having a solid plan enables you to pursue hobbies, travel, or spend time with loved ones without financial constraints.

- Peace of Mind: Knowing you have a secure financial future brings invaluable peace of mind, reducing stress and anxiety about your later years.

Setting Retirement Goals

Retirement planning without clear goals is like sailing without a destination – you might enjoy the journey, but you’re unlikely to end up where you want to be. Setting specific retirement goals is crucial for several reasons:

- Motivation: Having a clear picture of your desired retirement lifestyle fuels your drive to save and invest wisely.

- Planning: Knowing how much money you’ll need and when you want to retire helps you determine how much to save each month and what investment strategies to adopt.

- Decision Making: Retirement goals provide a framework for making important financial decisions, ensuring your choices align with your long-term vision.

Consider these factors when setting your retirement goals:

- Desired Lifestyle: Envision your ideal retirement. Do you want to travel the world, pursue hobbies, downsize your home, or spend more time with family? The cost of living varies greatly depending on your desired lifestyle.

- Retirement Age: When do you want to retire? Retiring earlier often requires more aggressive saving and investing, while delaying retirement gives your investments more time to grow.

- Health Considerations: Factor in potential healthcare costs and long-term care needs. These expenses can significantly impact your retirement savings.

- Inflation: The cost of living will likely rise over time. Ensure your retirement savings account for inflation to maintain your purchasing power.

Understanding Retirement Accounts

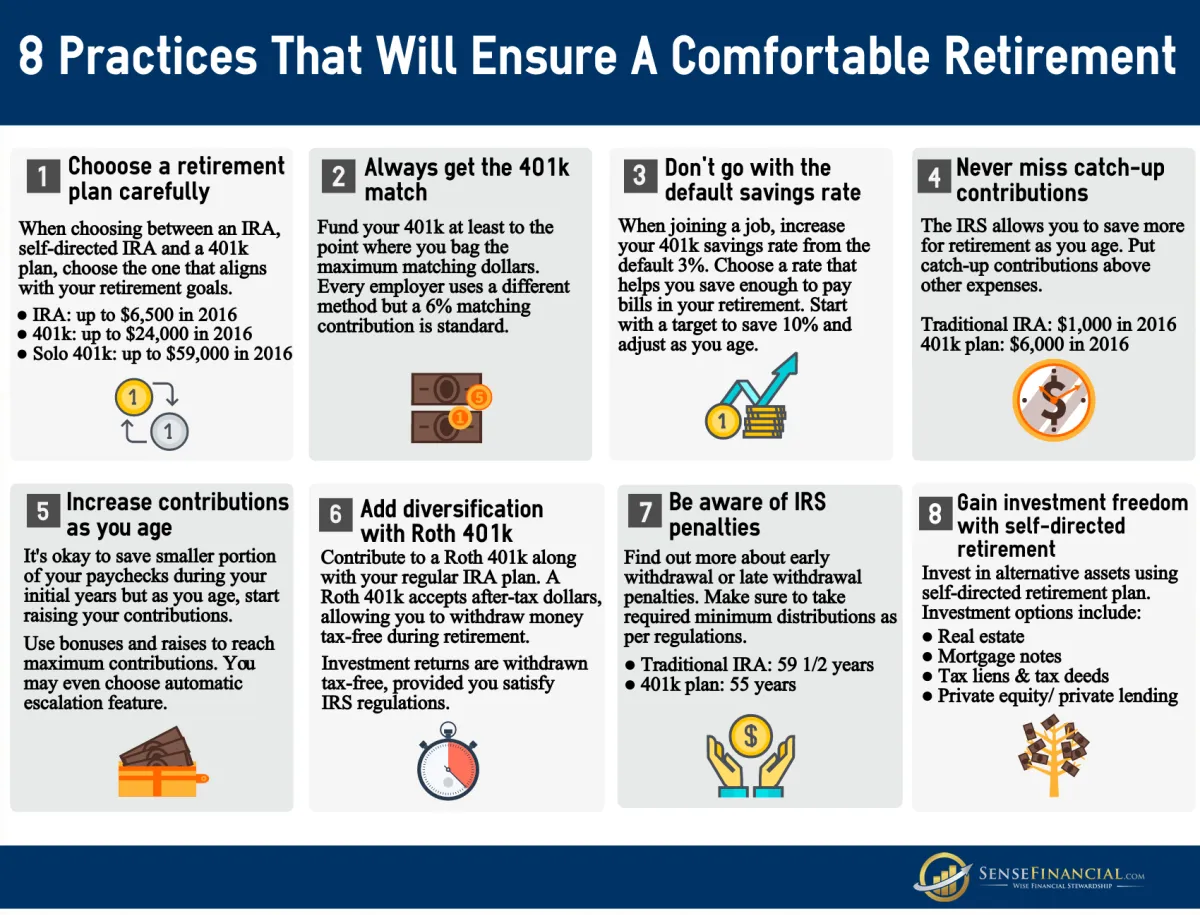

Retirement accounts are specialized financial accounts designed to help you save and invest for retirement. They offer various tax advantages and, in some cases, employer contributions to incentivize saving. Understanding the different types of retirement accounts is crucial for maximizing your savings and securing your financial future.

Common Types of Retirement Accounts:

- 401(k) Plans: These employer-sponsored plans allow pre-tax contributions from your paycheck, reducing your taxable income. Some employers offer a matching contribution up to a certain percentage, essentially free money towards your retirement.

- 403(b) Plans: Similar to 401(k)s, 403(b) plans are designed for employees of public schools and certain tax-exempt organizations.

- Traditional IRA: With a traditional IRA, you make pre-tax contributions, and your money grows tax-deferred until retirement. This can be a good option if you expect to be in a lower tax bracket in retirement.

- Roth IRA: Unlike traditional IRAs, contributions to a Roth IRA are made with after-tax dollars. However, withdrawals in retirement are tax-free, making it potentially advantageous if you anticipate being in a higher tax bracket later in life.

Key Considerations When Choosing a Retirement Account:

- Eligibility requirements: Different accounts have different eligibility criteria based on employment status, income levels, and other factors.

- Contribution limits: The amount you can contribute annually to these accounts is limited by the IRS and subject to change.

- Investment options: Each plan offers a menu of investment options, such as mutual funds, stocks, and bonds. Understanding your risk tolerance and investment timeline is crucial.

- Fees and expenses: Pay attention to administrative fees, investment expense ratios, and other charges that can impact your overall returns.

Consulting with a financial advisor can help you determine which retirement account(s) align with your financial goals, risk tolerance, and retirement timeline.

How to Save for Retirement

Saving for retirement is crucial for ensuring a comfortable and financially secure future. Here are some effective ways to save for your golden years:

1. Start Early and Be Consistent

The earlier you start saving, the better. Time is your greatest asset when it comes to retirement savings. Even small contributions made consistently over a long period can grow significantly due to the power of compounding.

2. Set Realistic Savings Goals

Determine how much money you’ll need to maintain your desired lifestyle during retirement and set realistic savings goals accordingly. Consider factors such as inflation, healthcare costs, and your estimated lifespan.

3. Take Advantage of Employer-Sponsored Plans

If your employer offers a 401(k) or similar retirement plan, contribute as much as you can, especially if they provide a matching contribution. This is essentially free money that can boost your savings significantly.

4. Explore Individual Retirement Accounts (IRAs)

IRAs, such as Traditional and Roth IRAs, offer tax advantages for retirement savings. Contribute to these accounts to supplement your employer-sponsored plan or if you don’t have access to one.

5. Consider Diversifying Your Investments

Don’t put all your eggs in one basket. Diversify your retirement savings by investing in a mix of assets, such as stocks, bonds, and real estate, to mitigate risk and maximize potential returns.

6. Automate Your Savings

Set up automatic transfers from your checking account to your retirement accounts each month. This “pay yourself first” approach ensures consistent savings without much effort.

7. Seek Professional Financial Advice

Consider consulting with a qualified financial advisor to create a personalized retirement plan tailored to your specific circumstances and goals.

Investment Strategies for Retirement

Planning for retirement requires careful consideration of how you’ll invest your savings to support your desired lifestyle. Here are some investment strategies to explore:

1. Determine Your Risk Tolerance

Your risk tolerance refers to how comfortable you are with the possibility of your investments fluctuating in value. Younger investors with a longer time horizon might be comfortable with higher-risk investments that have the potential for higher returns. As you approach retirement, you may want to shift to a more conservative approach with lower-risk investments.

2. Diversify Your Portfolio

Diversification is key to managing risk. Instead of putting all your eggs in one basket, spread your investments across different asset classes such as:

- Stocks: Offer potential for high growth but also come with higher volatility.

- Bonds: Generally less risky than stocks and provide steady income.

- Real Estate: Can be a good long-term investment, but it’s less liquid than stocks or bonds.

- Cash and Cash Equivalents: Important for liquidity but generally offer lower returns.

3. Consider Target-Date Funds

Target-date funds are designed to simplify retirement investing. You choose a fund with a target date close to your expected retirement year, and the fund managers adjust the asset allocation over time, becoming more conservative as you approach retirement.

4. Explore Retirement Accounts

Take advantage of tax-advantaged retirement accounts like:

- 401(k) or 403(b): Employer-sponsored plans that often come with employer matching contributions.

- Traditional IRA: Contributions may be tax-deductible, and earnings grow tax-deferred.

- Roth IRA: Contributions aren’t tax-deductible, but withdrawals in retirement are tax-free.

5. Rebalance Regularly

As market conditions change, your portfolio’s asset allocation may drift from your original plan. It’s important to rebalance your portfolio periodically by buying or selling assets to return to your desired asset mix.

6. Seek Professional Advice

Consider consulting with a qualified financial advisor. They can help you create a personalized retirement plan and recommend investment strategies tailored to your specific needs and goals.

Estimating Retirement Expenses

One of the first steps in retirement planning is determining how much money you’ll need to maintain your desired lifestyle after you stop working. This can be challenging, as retirement can last for several decades, and expenses can fluctuate due to inflation and unforeseen circumstances. However, a realistic estimate is crucial for establishing saving goals and making informed financial decisions.

Start by analyzing your current expenses. Consider housing costs (rent or mortgage, property taxes, insurance), utilities, groceries, transportation, healthcare, entertainment, and any outstanding debts. Then, think about how these expenses might change in retirement. For example, you might spend less on commuting but more on travel and hobbies.

Factor in inflation. The cost of goods and services generally rises over time, so it’s essential to account for inflation when estimating retirement expenses. A modest annual inflation rate of 3% can significantly impact your purchasing power over time.

Consider healthcare costs. Healthcare expenses tend to increase with age, and it’s essential to factor in potential long-term care needs. Explore different health insurance options and research the average costs associated with medical procedures and long-term care in your area.

While estimating retirement expenses requires careful consideration and can feel daunting, numerous online calculators and financial advisors can help you create a personalized retirement budget based on your circumstances and goals.

Planning for Healthcare Costs

Retirement planning isn’t just about ensuring you have enough money to cover your living expenses; it also means preparing for potential healthcare costs. As you age, the likelihood of needing medical care increases, and these expenses can quickly erode your retirement savings if not adequately planned for.

Here are key points to consider:

1. Understand Medicare and its limitations:

While Medicare provides essential healthcare coverage for those aged 65 and older, it doesn’t cover everything. Familiarize yourself with what Medicare does and, more importantly, does NOT cover. For example, long-term care, dental, and vision often require additional coverage.

2. Explore supplemental health insurance options:

Consider options like Medicare Advantage (Part C) or Medigap (Medicare Supplement) plans to fill the gaps in your original Medicare coverage. These plans come with additional costs but can save you significant money in the long run, especially if you have pre-existing conditions.

3. Factor in potential long-term care costs:

Long-term care, which includes services like nursing homes or assisted living, isn’t typically covered by Medicare and can be very expensive. Consider purchasing long-term care insurance or exploring other financial planning tools to prepare for this possibility.

4. Build a dedicated healthcare savings fund:

Start setting aside money specifically for future healthcare costs. A Health Savings Account (HSA) is a great option if you’re eligible, offering tax advantages for medical expenses. Even if you can’t contribute to an HSA, a regular savings account dedicated to healthcare can make a difference.

5. Estimate your future healthcare needs:

While predicting the future is impossible, take your current health, family history, and potential future needs into account when estimating retirement healthcare costs. Various online calculators can help you get a rough estimate, but it’s also wise to consult a financial advisor for personalized advice.

Adjusting Your Plan Over Time

Retirement planning isn’t a “set it and forget it” endeavor. Life throws curveballs, your goals evolve, and economic conditions fluctuate. Regularly revisiting and adjusting your retirement plan is crucial to stay on track for a secure future. Here’s why and how:

Why Adjustments Are Necessary:

- Life Changes: Marriage, divorce, having children, career shifts, or caring for aging parents can significantly impact your financial situation and retirement needs.

- Market Volatility: Investment returns aren’t guaranteed. Market downturns can impact your savings, requiring adjustments to your investment strategy or retirement timeline.

- Inflation: The rising cost of living erodes the purchasing power of your savings over time. Your plan needs to outpace inflation to maintain your desired lifestyle.

- Health and Longevity: Unexpected healthcare costs or living longer than anticipated can put a strain on your retirement funds.

How to Adjust Your Plan:

- Regular Review: Review your plan at least annually, or whenever a major life event occurs. Analyze your progress, update your goals, and assess if you’re on track.

- Reassess Your Risk Tolerance: As you get closer to retirement, your risk tolerance might decrease. Consider shifting towards more conservative investments.

- Adjust Contributions: If possible, increase your retirement contributions, especially after a salary raise or if you’re behind on your savings goals.

- Re-evaluate Your Retirement Age: Working a few years longer than initially planned can significantly impact your financial security by boosting savings and delaying withdrawals.

- Consult a Financial Advisor: A qualified financial advisor can provide personalized guidance, help you navigate market changes, and make adjustments tailored to your circumstances.

Conclusion

In conclusion, proper retirement planning is crucial for a secure future. Start early, save consistently, diversify investments, and seek professional advice to ensure a financially stable retirement.

{kind=link}