In the digital age, understanding how to effectively manage your credit score is essential for financial wellness. Learn the strategies and tips to maintain a healthy credit score and secure your financial future.

What is a Credit Score?

In simple terms, a credit score is a three-digit number that represents your creditworthiness or how likely you are to repay borrowed money responsibly. It’s a numerical snapshot of your financial health based on your credit history. Lenders, such as banks and credit card companies, use this score to assess the risk involved in lending to you.

Think of it like a financial report card. A higher score suggests you’ve managed credit well in the past, making you a more attractive borrower. This often translates into lower interest rates and better loan terms. Conversely, a lower score indicates potential risk for lenders, potentially leading to higher interest rates or even loan denials.

Your credit score is calculated by credit bureaus using information from your credit report. These reports track your borrowing and repayment history, including:

- Credit cards

- Mortgages

- Auto loans

- Student loans

- Other types of credit accounts

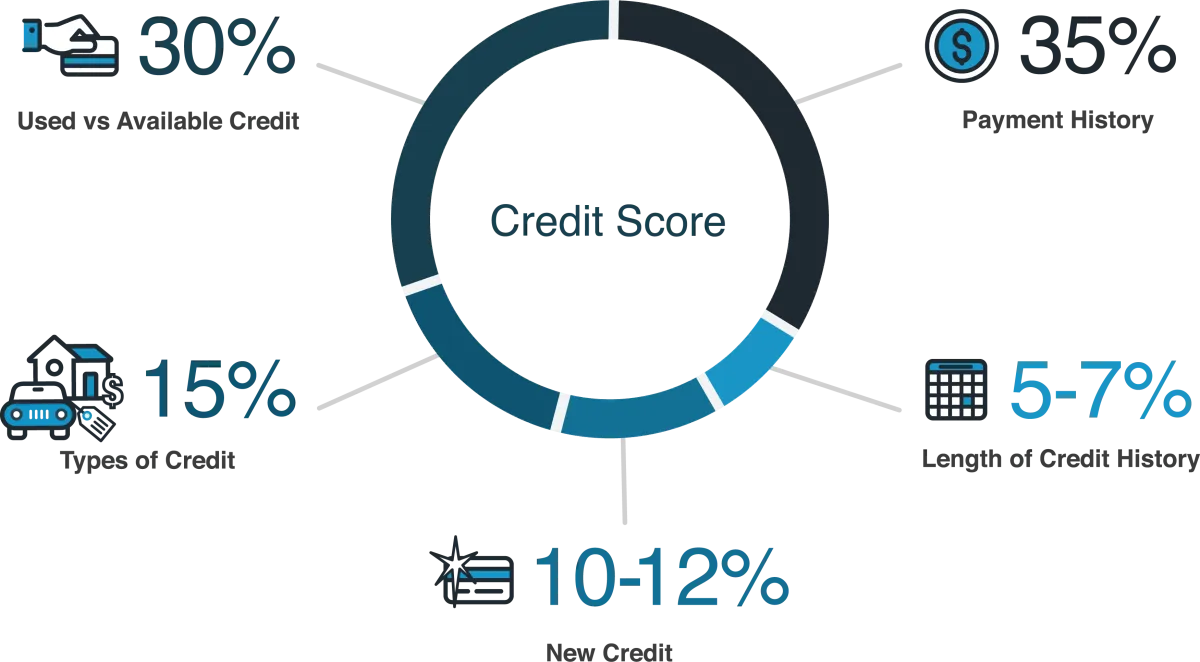

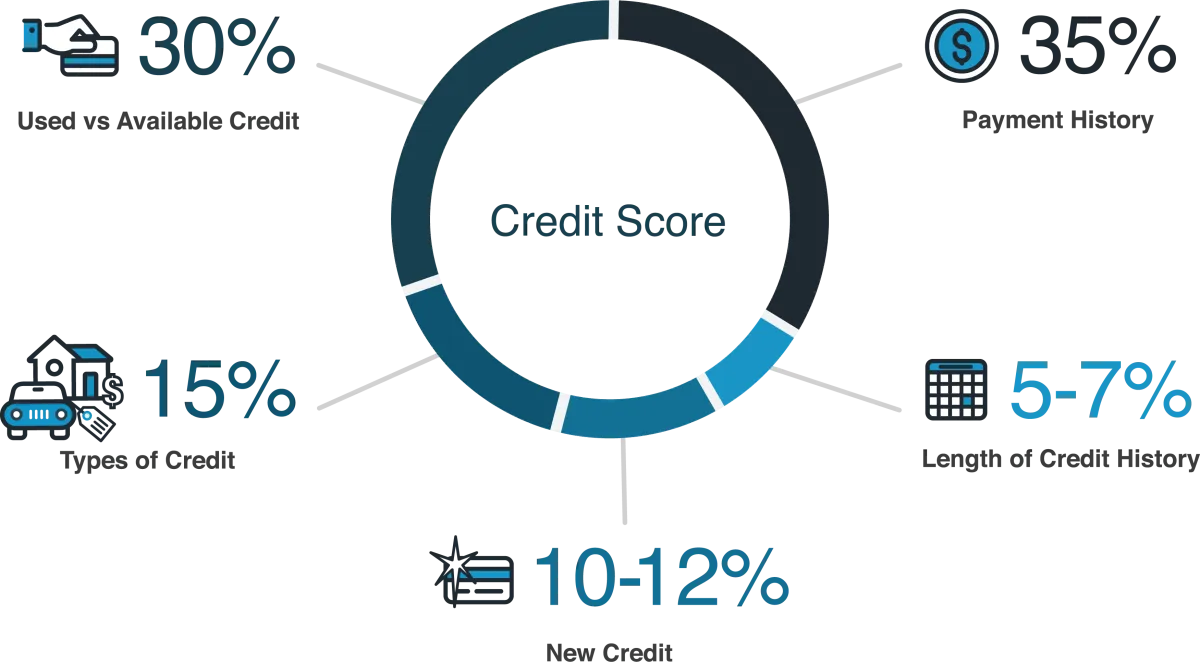

Factors Affecting Your Credit Score

Your credit score is a numerical representation of your creditworthiness, reflecting how responsibly you’ve managed your financial obligations. Lenders use it to assess the risk associated with lending you money. A higher credit score generally translates to more favorable loan terms and interest rates. Understanding the factors influencing your score is crucial for building and maintaining healthy credit. Here are some key factors that affect your credit score:

Payment History

This is the most significant factor, accounting for roughly 35% of your credit score. It tracks your consistency in making on-time payments for credit cards, loans, utilities, and other bills. A history of late or missed payments can severely damage your score.

Credit Utilization Rate

This refers to the percentage of your available credit that you’re currently using. It makes up around 30% of your credit score. A lower credit utilization ratio is generally better, indicating you’re not overly reliant on credit. Ideally, aim to keep your utilization below 30%.

Length of Credit History

The age of your credit accounts contributes to about 15% of your credit score. A longer credit history with a positive payment track record demonstrates financial responsibility and can boost your score.

Credit Mix

This factor, accounting for around 10%, reflects the diversity of your credit accounts, such as credit cards, installment loans (like auto or personal loans), and mortgages. Having a mix of credit types can positively impact your score, showcasing your ability to manage different forms of credit.

New Credit

Applying for new credit accounts too frequently can negatively impact your score (about 10%). Each credit inquiry associated with an application can temporarily lower your score, especially if done within a short period.

Tips for Improving Your Credit Score

A good credit score is crucial for securing loans, renting an apartment, and even landing certain jobs. If your credit score needs a boost, there are several steps you can take to improve it over time:

1. Pay Your Bills on Time

Payment history is one of the most significant factors influencing your credit score. Consistently paying your bills on time, including credit cards, utilities, and loans, demonstrates financial responsibility to lenders.

2. Reduce Your Credit Utilization Ratio

Your credit utilization ratio is the amount of credit you use compared to your total available credit. Keeping this ratio low, ideally below 30%, shows lenders you’re not overly reliant on credit.

3. Keep Old Credit Accounts Open

The length of your credit history also plays a role in your score. Closing old credit cards, even if you don’t use them, can shorten your credit history and potentially lower your score.

4. Avoid Applying for Too Much Credit

Each time you apply for a new credit card or loan, a hard inquiry is recorded on your credit report. Too many hard inquiries in a short period can negatively impact your score.

5. Regularly Check Your Credit Report

It’s essential to monitor your credit report for any errors or discrepancies that could be hurting your score. You’re entitled to a free copy of your credit report from each of the three major credit bureaus (Equifax, Experian, and TransUnion) annually.

How to Check Your Credit Report

Checking your credit report is the first step towards effectively managing your credit score. It provides a detailed overview of your credit history, allowing you to identify any inaccuracies or areas for improvement.

Accessing Your Credit Report

You are entitled to obtain free credit reports from each of the three major credit bureaus – Equifax, Experian, and TransUnion – annually. You can request your reports online, by phone, or by mail.

- AnnualCreditReport.com: This website, authorized by federal law, provides a secure platform to access your reports from all three bureaus simultaneously.

- Credit Bureau Websites: You can visit the individual websites of Equifax, Experian, and TransUnion to request your report directly.

- Phone: Call the toll-free number provided by each credit bureau to request your report over the phone.

- Mail: Download and complete the Annual Credit Report Request Form and mail it to the designated address.

Understanding Your Credit Report

Once you have obtained your credit report, it’s important to carefully review it for any errors or discrepancies. Your credit report typically contains the following sections:

- Personal Information: This section includes your name, address, Social Security number, and date of birth. Verify that all information is accurate and up to date.

- Credit Accounts: This section lists your open and closed credit accounts, including credit cards, loans, and mortgages. Review the details of each account, such as the creditor’s name, account balance, and payment history.

- Public Records: This section may include information on bankruptcies, tax liens, or judgments against you.

- Inquiries: This section lists all entities that have accessed your credit report, including lenders, employers, and yourself.

Common Credit Score Myths

Understanding your credit score is crucial for navigating the financial world, but misinformation often clouds the truth. Let’s debunk some prevalent credit score myths:

Myth 1: Checking your credit score hurts your score.

This is false. Checking your own credit report is considered a “soft inquiry,” which doesn’t affect your score. It’s essential to regularly monitor your credit report for errors or signs of fraud.

Myth 2: Closing old credit cards improves your score.

Not necessarily. While it might seem logical to close old, unused accounts, doing so can actually lower your score. One factor in calculating your score is the length of your credit history, and closing old accounts shortens it. Additionally, it can negatively impact your credit utilization ratio (the amount of credit you use compared to your total available credit).

Myth 3: Carrying a small balance on your credit card helps build credit.

This is another misconception. You don’t need to carry a balance to improve your score. It’s best to pay off your credit card balance in full each month to avoid interest charges and demonstrate responsible credit management.

Myth 4: Your income determines your credit score.

False. While a stable income can help you qualify for loans, it doesn’t directly impact your credit score. Credit scores are based on your credit history, including payment history, credit utilization, and types of credit used.

Impact of Credit Score on Loans

Your credit score plays a pivotal role in your ability to secure loans and the terms you’ll receive. It acts as a financial report card for lenders, providing insights into your creditworthiness and how likely you are to repay borrowed funds.

Here’s how your credit score can impact your loans:

Loan Approval:

A higher credit score significantly increases your chances of loan approval. Lenders view borrowers with good credit as less risky. Conversely, a lower score may lead to loan applications being declined or facing more stringent approval requirements.

Interest Rates:

Your credit score directly influences the interest rates offered on loans. A higher score generally qualifies you for lower interest rates, saving you significant money over the life of the loan. A lower score, on the other hand, can result in higher interest rates, increasing the overall cost of borrowing.

Loan Terms:

Credit scores can also impact loan terms, including loan amounts, repayment periods, and fees. Borrowers with excellent credit scores often have access to larger loan amounts, more flexible repayment options, and lower fees. In contrast, those with lower scores might face limitations on loan amounts, shorter repayment terms, and higher fees.

Credit Card Terms:

Credit card issuers also rely heavily on credit scores. A good score can lead to higher credit limits, lower APRs (Annual Percentage Rates), and more enticing rewards programs. A lower score may limit your card choices, result in lower credit limits, and carry higher interest rates.

Dealing with Credit Score Errors

It’s not uncommon for errors to pop up on your credit report, potentially dragging down your score. Here’s how to tackle them head-on:

1. Review Your Credit Reports Regularly

The foundation of catching errors is consistent monitoring. Request free copies of your credit reports from all three major credit bureaus (Equifax, Experian, and TransUnion) at AnnualCreditReport.com. Review them carefully for any inaccuracies.

2. Identify and Understand the Errors

Look for discrepancies such as:

- Incorrect personal information (name, address, Social Security number)

- Accounts that don’t belong to you

- Inaccurate account balances or payment histories

- Duplicate accounts

3. Dispute Errors with the Credit Bureaus

If you find errors, file a dispute with the relevant credit bureau(s) online, by mail, or by phone. Provide specific details about the error, including supporting documentation (e.g., account statements, bills) to validate your claim.

4. Dispute Errors with the Furnisher

Simultaneously, contact the creditor or lender that provided the inaccurate information (the “furnisher”). Explain the error and provide the same documentation you used for the credit bureau dispute.

5. Monitor the Dispute Process

The credit bureau has 30 days (in some cases, 45) to investigate your dispute. They must notify you of the outcome in writing and provide you with a free copy of your credit report if the dispute results in a change.

6. Don’t Give Up!

Be persistent! If your dispute is initially denied, don’t hesitate to re-dispute the error, especially if you have additional documentation to support your claim.

Building and Maintaining Good Credit

Building good credit is essential for financial health, as it opens doors to lower interest rates, better loan terms, and greater financial opportunities. Here’s how to establish and maintain a solid credit history:

1. Establish a Credit History

- Open a Secured Credit Card: Secured cards require a security deposit that typically equals the credit limit, making them less risky for lenders and a good option for building credit from scratch.

- Become an Authorized User: Ask a trusted friend or family member to add you as an authorized user on their credit card. This allows their positive credit history to reflect on your credit report, boosting your score.

- Get a Credit Builder Loan: These small loans are held by the lender and paid off in installments. Your payments are reported to credit bureaus, helping you establish positive credit.

2. Use Credit Responsibly

- Pay Your Bills on Time: Payment history is the most significant factor influencing your credit score. Set reminders or automate payments to ensure you never miss a due date.

- Maintain Low Credit Utilization: Aim to keep your credit utilization rate below 30%. This refers to the amount of credit you’re using compared to your total available credit limit.

- Avoid Opening Too Many Accounts: Each new credit application can result in a hard inquiry on your credit report, potentially lowering your score. Only apply for credit when needed.

3. Monitor Your Credit Report

- Check for Errors: Regularly review your credit reports from all three bureaus (Equifax, Experian, TransUnion) for inaccuracies. Dispute any errors promptly to maintain the integrity of your credit history.

- Track Your Progress: Monitor your credit score to see how your financial habits impact it over time. This allows you to make adjustments and stay on top of your credit health.

Conclusion

In conclusion, managing your credit score effectively is crucial for financial stability. By practicing responsible credit habits such as timely payments and monitoring your score regularly, you can improve your creditworthiness and access better financial opportunities.

{kind=link}