Discover the top strategies essential for achieving successful small business financing, from securing loans to exploring alternative funding options.

Understanding Small Business Financing

Small business financing refers to the various methods entrepreneurs use to obtain capital to start, operate, or grow their businesses. It’s a critical aspect of entrepreneurship, as adequate funding fuels business operations, facilitates expansion, and can be the determining factor between success and failure.

Why is understanding small business financing important?

- Informed Decision Making: A strong grasp of financing options allows you to choose the best fit for your business needs and goals, minimizing risk and maximizing potential returns.

- Financial Health: Understanding financing terms, interest rates, and repayment structures is crucial for maintaining a healthy cash flow and ensuring the long-term sustainability of your business.

- Growth and Expansion: Knowing how and where to access capital can be the key to seizing growth opportunities, investing in new equipment, or expanding into new markets.

Key areas to understand within small business financing include:

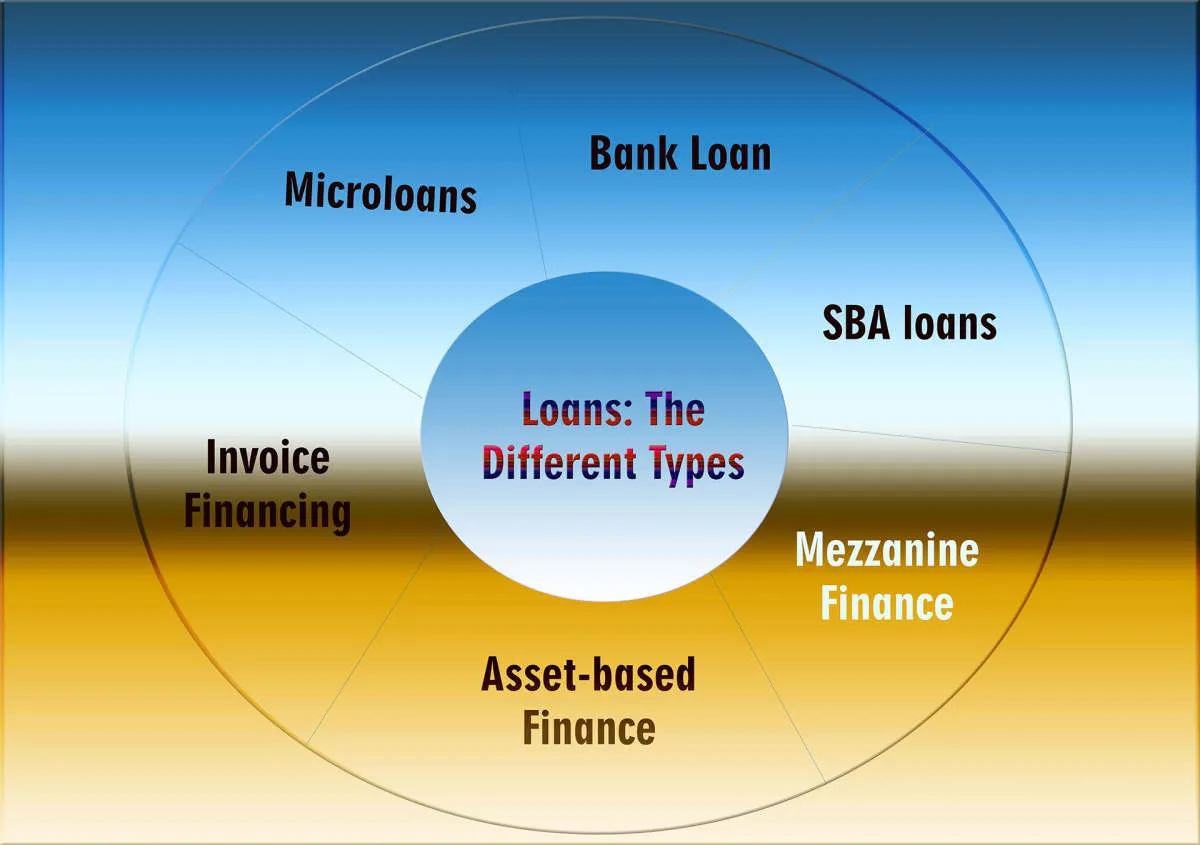

- Types of Financing: Explore the diverse range of options available, such as bank loans, SBA loans, lines of credit, equipment financing, invoice financing, crowdfunding, angel investors, and venture capitalists.

- Eligibility Requirements: Each financing option comes with specific requirements related to credit score, business history, revenue, and collateral. Understanding these criteria is essential to determine which options are viable for your business.

- Financing Terms: Pay close attention to interest rates, repayment periods, fees, and any potential prepayment penalties associated with each financing option.

Types of Business Loans

Navigating the world of business financing can feel like traversing a maze. Understanding the different loan types available is key to securing the right funding for your specific needs. Let’s shed light on some popular options:

1. Term Loans

Term loans are a cornerstone of business financing. These loans provide a lump sum upfront, repaid with interest over a set period (the “term”). They offer predictability in repayment and can be used for various purposes, from purchasing equipment to managing cash flow.

2. Lines of Credit

Think of a line of credit as a financial safety net. It provides access to a pre-approved amount of funds that you can draw upon as needed. Interest is only charged on the amount you use. This flexibility makes lines of credit ideal for managing short-term expenses or unexpected cash flow gaps.

3. SBA Loans

Backed by the Small Business Administration (SBA), these loans offer competitive terms and lower down payment requirements. SBA loans can be a great option for businesses that might not qualify for traditional financing.

4. Equipment Financing

Need to invest in new machinery or vehicles? Equipment financing allows you to purchase the assets your business needs, using the equipment itself as collateral. This can be a cost-effective way to upgrade without depleting your working capital.

5. Invoice Financing

Dealing with slow-paying clients? Invoice financing unlocks the cash tied up in your outstanding invoices. A lender provides an advance on your invoices, giving you immediate access to funds while you await payment from your customers.

How to Apply for a Business Loan

Applying for a business loan requires careful preparation and a clear understanding of the process. Here’s a step-by-step guide to help you navigate the application procedure:

1. Determine Your Needs and Eligibility

Before applying, determine the specific amount you need and how you’ll use the funds. Lenders want to see a well-defined purpose for the loan. Research lender eligibility criteria, including credit score requirements, revenue thresholds, and time in business.

2. Research and Choose a Lender

Explore different lenders, including traditional banks, credit unions, and online lenders. Compare interest rates, loan terms, and eligibility requirements to find the best fit for your business needs.

3. Gather Your Documentation

Be prepared to provide comprehensive documentation, including:

- Business plan

- Financial statements (balance sheets, income statements, cash flow statements)

- Tax returns (personal and business)

- Bank statements

- Legal documents (business licenses, permits, articles of incorporation)

4. Complete the Application

Fill out the loan application accurately and completely. Double-check all information to avoid delays in processing.

5. Review and Submit

Carefully review the loan agreement, terms, and conditions before submitting. Ensure you understand the interest rate, repayment schedule, and any associated fees.

6. Follow Up

After submitting your application, follow up with the lender to check on its status and provide any additional information required. Be proactive and responsive throughout the process.

Alternative Financing Options

While traditional bank loans are often the go-to for small business funding, they aren’t the only option. In fact, securing a bank loan, especially for newer businesses, can be challenging. That’s where alternative financing options come into play. Let’s explore some popular choices:

1. Crowdfunding

Platforms like Kickstarter and Indiegogo allow you to raise funds from a large pool of individuals who believe in your business idea. This method works especially well for businesses with a unique product or service that can generate excitement.

2. Peer-to-Peer Lending

Websites like LendingClub and Prosper connect borrowers directly with individual lenders, often bypassing the stricter requirements of traditional banks. This can be a faster way to access funding.

3. Invoice Financing

If you have a business with outstanding invoices, invoice financing allows you to borrow money against the value of those invoices. This provides immediate cash flow without waiting for customers to pay.

4. Microloans

Non-profit organizations often provide microloans, which are smaller loans specifically designed for startups and small businesses. These loans usually come with lower interest rates and more flexible terms.

5. Angel Investors and Venture Capitalists

Angel investors are individuals who provide capital in exchange for equity in your company. Venture capitalists are firms that invest larger sums in businesses with high growth potential, also for equity.

Managing Business Finances

Effective financial management is the backbone of any successful small business. It’s not just about securing funding; it’s about making smart decisions with the money you have and planning for the future. Here’s a closer look at key components of managing your business finances:

1. Budgeting and Forecasting

Create a realistic budget that outlines your projected income and expenses. This roadmap will help you track cash flow, identify potential shortfalls, and make informed spending decisions. Regularly revisit and adjust your budget as needed, especially during periods of growth or economic uncertainty. Forecasting future financial performance based on historical data and market trends is also crucial for long-term planning.

2. Separate Business and Personal Finances

One of the most important steps for financial clarity and legal protection is maintaining separate bank accounts and credit cards for your business. This separation simplifies accounting, reduces liability risks, and makes it easier to track your business’s financial performance.

3. Track All Income and Expenses

Maintain meticulous records of all financial transactions, including sales, invoices, payments, and receipts. This practice is not only essential for tax purposes but also provides valuable insights into your business’s financial health. Use accounting software to streamline this process and generate reports that facilitate informed decision-making.

4. Monitor Key Financial Metrics

Regularly review key financial indicators to understand your business’s performance. These metrics might include:

- Gross profit margin: This reflects the profitability of your products or services.

- Net profit margin: This shows your overall profitability after all expenses are considered.

- Current ratio: This measures your ability to cover short-term liabilities.

- Debt-to-equity ratio: This indicates the level of debt used to finance your business.

Analyzing these metrics helps identify areas for improvement and make informed financial decisions.

5. Plan for Taxes

Understanding your tax obligations and implementing a strategy for managing them is critical. Consult with a tax professional to stay informed about relevant deductions, credits, and filing requirements. Setting aside funds throughout the year for tax payments can prevent financial strain come tax season.

Tips for Improving Business Credit

Establishing strong business credit is crucial for securing favorable financing options. Here are some effective tips to enhance your business credit:

1. Separate Business and Personal Finances

Open a dedicated bank account and credit card specifically for your business. This helps lenders distinguish your personal and business credit histories, showcasing your business’s financial health independently.

2. Establish Trade Lines

Work with vendors and suppliers who report to business credit bureaus. Consistently paying invoices on time through these trade lines demonstrates your creditworthiness to potential lenders.

3. Monitor Your Business Credit Reports

Regularly review your business credit reports from major credit bureaus like Experian, Equifax, and Dun & Bradstreet. Check for any inaccuracies and dispute them promptly to maintain a healthy credit profile.

4. Manage Debt Responsibly

Keep your business credit utilization rate low by using a small portion of your available credit. Avoid maxing out credit cards and aim for a healthy credit-to-debt ratio.

5. Build a Positive Payment History

Make all loan payments, bill payments, and supplier invoices on time. Late payments can severely damage your business credit score, making it harder to secure financing in the future.

6. Consider a Business Credit Card

Using a business credit card responsibly and paying it off in full each month can help build a positive credit history and improve your credit score.

7. Time is of the Essence

Building a strong business credit profile takes time and effort. Start implementing these tips early in your business journey to establish a solid foundation for future financing opportunities.

Financial Planning for Growth

While securing funding is a crucial step, successful small business financing hinges on strategic financial planning for growth. This involves:

1. Forecasting Future Cash Flows:

Accurately projecting future revenue and expenses is vital. Consider historical data, market trends, and your growth strategy to create realistic financial forecasts. This helps determine how much funding you need, when you need it, and how it will impact your future financial position.

2. Budgeting for Growth Initiatives:

Allocate resources wisely by creating a detailed budget that aligns with your growth objectives. Outline specific expenditures for marketing and advertising, hiring new talent, expanding inventory, or investing in new equipment. Ensure your budget balances growth initiatives with your operational needs.

3. Monitoring Key Performance Indicators (KPIs):

Identify and track KPIs relevant to your growth strategy. This may include metrics like customer acquisition cost, lifetime value, sales growth, or gross profit margin. Regularly monitoring these KPIs allows you to measure the effectiveness of your growth initiatives and make necessary adjustments.

4. Seeking Expert Financial Advice:

Consult with a financial advisor or accountant experienced in working with small businesses. They can provide valuable guidance on financial forecasting, budgeting, tax implications of growth, and optimizing your capital structure.

Avoiding Common Financing Mistakes

Securing funding is crucial for small business growth, but navigating the financial landscape can be tricky. Avoiding these common mistakes can significantly increase your chances of securing favorable financing and setting your business up for success:

1. Poor Planning and Preparation

One of the biggest mistakes is approaching lenders without a solid business plan. Lenders need to see a clear roadmap outlining your business goals, revenue projections, and how you plan to use the funds. A well-structured business plan demonstrates your seriousness and increases lender confidence.

2. Underestimating Funding Needs

It’s common for entrepreneurs to underestimate startup or expansion costs. Factor in all potential expenses, including equipment, inventory, marketing, and unforeseen contingencies. It’s better to secure slightly more funding than to fall short during critical growth phases.

3. Ignoring Your Credit Score

Your personal and business credit scores play a significant role in loan approvals and interest rates. Before applying for financing, check your credit reports for errors and take steps to improve your score. A higher score can significantly improve your chances of securing loans with favorable terms.

4. Not Shopping Around for the Best Rates

Don’t jump at the first financing offer you receive. Explore different options from various lenders, including banks, credit unions, and online lenders. Compare interest rates, repayment terms, and any associated fees to find the most advantageous financing solution for your business.

5. Misunderstanding Loan Terms

Before signing any loan agreement, thoroughly review and understand all the terms and conditions. Pay close attention to interest rates, repayment schedules, penalties for late payments, and any prepayment options. Seek clarification from your lender on any points that are unclear.

Conclusion

In conclusion, mastering diverse financing strategies is crucial for small businesses to thrive and grow sustainably.

{kind=link}