In times of uncertainty, having an emergency fund is crucial. Learn effective strategies to quickly build a financial safety net to protect yourself from unforeseen expenses and emergencies.

Why an Emergency Fund is Important

Life is unpredictable. No matter how carefully you plan, unexpected expenses can pop up at any moment. These unexpected events can throw your finances into a tailspin if you’re not prepared. That’s where an emergency fund comes in.

An emergency fund is a safety net of money set aside specifically for unexpected expenses or financial hardships. These aren’t your everyday expenses, but rather the unforeseen circumstances that can wreak havoc on your finances.

Here’s why having an emergency fund is crucial:

- Peace of mind: Knowing you have a financial cushion to fall back on provides invaluable peace of mind. You won’t have to panic about where the money will come from if your car breaks down or you face a medical emergency.

- Avoid debt: Unexpected expenses often lead to high-interest debt, like credit cards. An emergency fund helps you avoid going into debt and accruing interest charges that can take years to pay off.

- Stay afloat during job loss: Losing your job is stressful enough without the added worry of how to pay your bills. An emergency fund can cover essential expenses while you search for a new job.

- Maintain financial stability: An emergency fund acts as a buffer to protect you from financial setbacks, helping you stay on track with your financial goals despite life’s curveballs.

Setting a Savings Goal

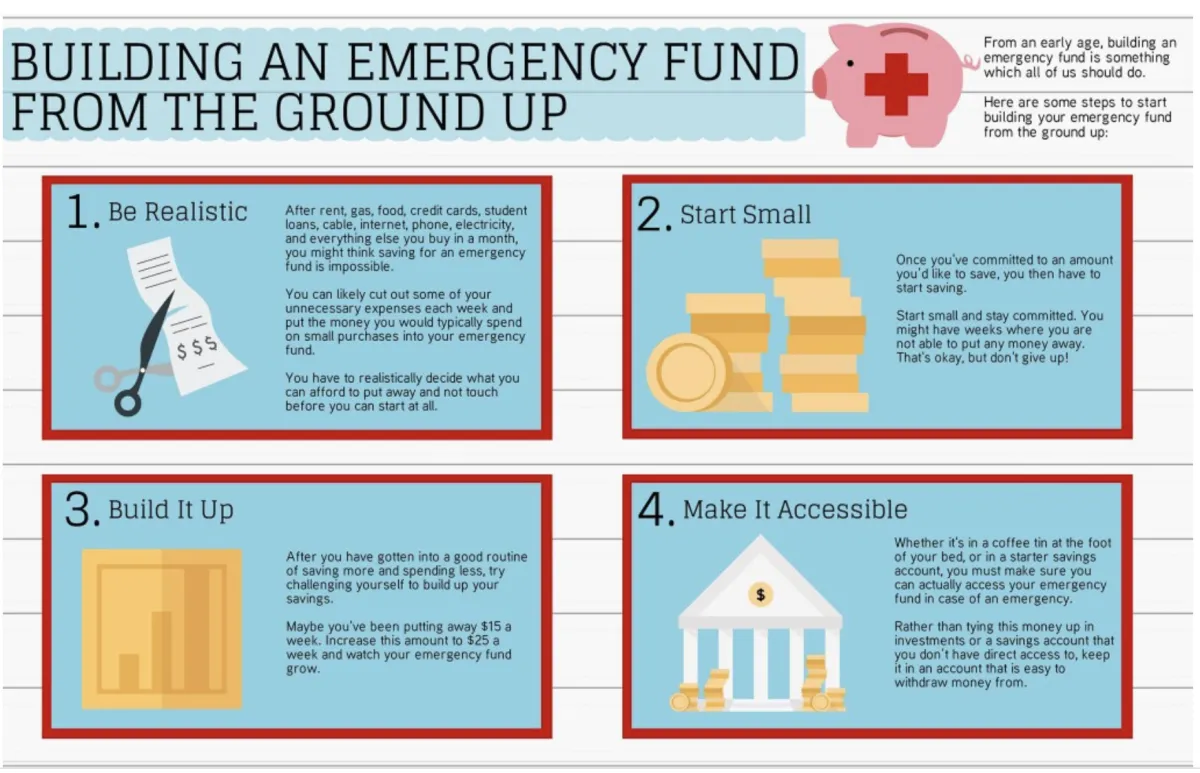

The first step to building an emergency fund, and arguably the most important, is setting a realistic savings goal. This will act as your financial target, keeping you motivated and providing a clear endpoint. But how much should you aim for?

Financial experts traditionally recommend having 3-6 months’ worth of living expenses saved. This provides a safety net to cover essential costs like rent/mortgage, utilities, groceries, and transportation in case of job loss, medical emergencies, or unexpected repairs.

However, your individual circumstances will determine the ideal amount for your emergency fund. Consider factors like:

- Job security: If your job is stable with consistent income, you may feel comfortable with a smaller emergency fund.

- Dependents: Having a family or others relying on your income means you need a larger safety net.

- Health and lifestyle: Those with pre-existing health conditions or riskier lifestyles may need a bigger cushion to cover potential expenses.

Don’t be discouraged if saving 3-6 months’ worth of expenses seems daunting. Start small and gradually work your way up. Even a $500 or $1,000 cushion is better than nothing and can provide peace of mind.

Finding Extra Money to Save

Building an emergency fund quickly requires finding extra cash in your budget. While it might seem impossible at first, there are several creative and practical strategies to uncover hidden funds:

1. Track Your Spending and Identify Leaks

You can’t fix what you don’t know. Start by tracking your expenses for a month. Utilize budgeting apps, review bank statements, or simply jot down every expenditure. Once you have a clear picture of where your money is going, identify areas where you can cut back. Those daily coffees or subscription boxes you barely use can add up quickly.

2. Reduce Non-Essential Expenses

Temporarily reduce spending on non-essential items. Consider dining out less, finding free entertainment alternatives, and postponing large purchases. This doesn’t mean living austerely, but making conscious choices to prioritize your emergency fund.

3. Increase Your Income with a Side Hustle

Explore side hustle opportunities to generate extra income. This could involve freelancing, driving for a ride-sharing service, selling crafts online, or utilizing your skills in other ways. Even dedicating a few hours a week can make a significant difference in your savings goals.

4. Sell Unused Items

Declutter your home and turn unwanted belongings into cash. List items on online marketplaces, hold a garage sale, or explore consignment options for clothing and electronics. You’ll be surprised how quickly those forgotten treasures can contribute to your emergency fund.

5. Utilize Windfalls Wisely

When you receive unexpected income, such as tax refunds, work bonuses, or monetary gifts, resist the temptation to spend it all. Instead, direct a significant portion, if not all, towards your emergency fund. This allows you to quickly boost your savings without impacting your regular budget.

Choosing the Right Savings Account

Finding the right place to store your emergency fund is crucial. While stashing cash under your mattress might seem tempting, a dedicated savings account offers several advantages:

- Security: Banks and credit unions provide insured protection for your money.

- Growth: Even a small amount of interest helps your emergency fund grow over time.

- Accessibility: You can easily access your funds in case of an emergency.

Here’s what to look for when selecting a savings account for your emergency fund:

1. High-Yield Savings Accounts

Prioritize accounts that offer competitive interest rates. A high-yield savings account, often found at online banks, can help your money grow faster.

2. Fees

Scrutinize the account for monthly maintenance fees, minimum balance requirements, or transaction limits that could eat into your savings.

3. FDIC or NCUA Insurance

Ensure the bank or credit union is federally insured (FDIC or NCUA), guaranteeing the safety of your deposits up to $250,000.

4. Accessibility

Confirm you can easily transfer funds or withdraw cash in case of an emergency. Some accounts may have limitations on withdrawals.

Cutting Expenses to Save More

Building an emergency fund quickly requires a two-pronged approach: increasing your income and decreasing your expenses. While finding ways to earn extra money is fantastic, cutting back on your spending often offers more immediate and impactful results.

Here are some practical strategies to trim your expenses and accelerate your emergency fund savings:

1. Track Your Spending:

You can’t manage what you don’t measure. Use a budgeting app, spreadsheet, or even a simple notebook to track every dollar you spend for a month. This will provide valuable insights into where your money is actually going.

2. Identify Needs vs. Wants:

Once you have a clear picture of your spending habits, categorize your expenses as either needs or wants. Needs are essential for living (housing, food, utilities) while wants are things that enhance your life but aren’t crucial (dining out, entertainment subscriptions, new clothes).

3. Reduce Non-Essential Spending:

This is where the rubber meets the road. Look for areas where you can cut back on wants. Can you reduce dining out to once a week? Downgrade your cable package? Find free or cheaper entertainment alternatives? Even small adjustments in multiple areas can add up to significant savings.

4. Negotiate Lower Bills:

Don’t be afraid to negotiate with service providers. Call your internet, phone, and insurance companies and inquire about discounts, promotions, or lower-priced plans. You might be surprised at how much you can save just by asking.

5. Shop Smart:

Embrace mindful shopping habits. Plan your meals, use grocery lists to avoid impulse purchases, and take advantage of sales and coupons. Consider buying generic brands when applicable.

6. Minimize Recurring Subscriptions:

Review all your subscriptions – streaming services, gym memberships, meal kits – and cancel anything you don’t use regularly. You can always re-subscribe later if needed.

Earning Extra Income

Building an emergency fund quickly often requires finding ways to boost your income. Here are some strategies to consider:

Short-Term Gigs

These options provide immediate income potential:

- Freelancing: Offer your skills in writing, editing, graphic design, web development, or virtual assistance.

- Gig Economy Platforms: Drive for a rideshare service, deliver food or groceries, or complete tasks on platforms like TaskRabbit.

- Selling Items: Declutter your home and sell unwanted clothes, electronics, or furniture online or at consignment shops.

Longer-Term Income Streams

Consider these options to create more consistent extra income:

- Part-Time Job: Look for a part-time position in retail, hospitality, or a field related to your skills.

- Side Hustle: Develop a service-based business like pet-sitting, house cleaning, or tutoring.

- Passive Income: Explore options like starting a blog or YouTube channel, selling online courses, or renting out a spare room on Airbnb (check local regulations).

Automating Your Savings

One of the most effective ways to build an emergency fund quickly is to automate your savings. This means setting up a system where a certain amount of money is automatically transferred from your checking account to your savings account on a regular basis.

Here are a few ways to automate your savings:

- Set up a recurring transfer with your bank. This is the easiest way to automate your savings. Simply log into your online banking account or visit your local branch and set up a recurring transfer from your checking account to your savings account. You can choose how much money you want to transfer and how often you want the transfer to occur (e.g., weekly, biweekly, or monthly).

- Use a micro-investing app. These apps round up your purchases to the nearest dollar and invest the difference. For example, if you buy a coffee for $2.50, the app will round up your purchase to $3 and invest the $0.50 difference. This is a great way to save small amounts of money without even thinking about it.

- Take advantage of employer-sponsored savings plans. If your employer offers a 401(k) or other retirement savings plan, consider contributing enough to get the full employer match. This is essentially free money that you can use to build your emergency fund.

The key to automating your savings is to make it consistent. Once you’ve set up a system, don’t touch it! The more consistent you are with your savings, the faster your emergency fund will grow.

Maintaining Your Emergency Fund

Congratulations! You’ve successfully built your emergency fund. But the work isn’t over yet. To keep your safety net strong, you’ll need to make maintaining your emergency fund an ongoing priority.

Here are key steps to maintaining your emergency fund:

- Regularly Replenish: Every time you dip into your emergency fund, make a plan to replenish those funds as soon as possible. Treat it like paying back a loan to yourself.

- Adjust for Life Changes: As your income, expenses, or dependents change, so too should your emergency fund. A promotion, a new baby, or a bigger mortgage might warrant increasing the amount you have saved.

- Account for Inflation: The cost of living goes up over time. To maintain your emergency fund’s buying power, reassess your savings goal annually and consider increasing it to outpace inflation.

- Separate Your Savings: Keep your emergency fund in a separate account from your everyday spending. This helps prevent accidental use and makes it easier to track your progress. Consider a high-yield savings account to earn interest while your money is safely stored.

- Automate Contributions: Just like building your emergency fund, maintaining it is easier with automation. Set up regular, automatic transfers from your checking account to your emergency fund. Even small amounts add up over time.

Remember, maintaining your emergency fund is a continuous process. By incorporating these tips into your financial habits, you’ll ensure that you’re always prepared for unexpected events, without derailing your financial progress.

Conclusion

Building an emergency fund promptly is crucial for financial security. By setting a realistic savings goal, cutting expenses, and prioritizing savings, you can efficiently create a safety net for unexpected situations.

{kind=link}