Managing your finances after a divorce can be challenging. Learn how to navigate this new financial chapter with expert tips and strategies to secure your financial future.

Assessing Your Financial Situation

After a divorce, your financial situation will likely look different than it did before. It’s crucial to take stock of where you stand financially to create a realistic budget and plan for the future. Here’s a breakdown of how to assess your financial situation post-divorce:

1. Gather Your Financial Documents

Start by collecting all relevant financial documents, including:

- Bank statements

- Credit card statements

- Investment account statements

- Tax returns

- Mortgage or lease agreements

- Insurance policies

- Divorce decree or settlement agreement

2. Create a List of Assets and Debts

Once you have your documents, create a comprehensive list of your:

Assets:

- Checking and savings accounts

- Retirement accounts

- Real estate

- Vehicles

- Other valuable assets

Debts:

- Mortgages

- Credit card balances

- Student loans

- Car loans

- Any other outstanding loans

3. Determine Your Income and Expenses

Calculate your post-divorce income, considering any:

- Employment income

- Spousal support (alimony)

- Child support

- Investment income

- Other sources of income

Next, track your expenses to understand where your money is going. Categorize your expenses, such as:

- Housing

- Utilities

- Food

- Transportation

- Healthcare

- Childcare

4. Review Your Credit Report

Obtain a copy of your credit report from all three credit bureaus (Equifax, Experian, and TransUnion). Review it for accuracy and address any errors immediately. Your credit score will impact your ability to secure loans or credit cards in the future.

5. Seek Professional Guidance

Consider consulting with a financial advisor, particularly one experienced in divorce proceedings. They can provide personalized advice based on your specific financial situation, helping you create a budget, manage debt, and plan for the future.

Creating a Post-Divorce Budget

After a divorce, your financial situation will likely change significantly. You may be living on one income instead of two, and you may have new expenses, such as alimony or child support payments. That’s why it’s more crucial than ever to create a post-divorce budget.

Here are some tips for creating a post-divorce budget:

- Track your income and expenses. The first step is to track your income and expenses for at least one month. This will give you a clear picture of where your money is going.

- Identify your needs and wants. Once you know where your money is going, you can start to identify your needs and wants. Needs are essential expenses, such as housing, food, and transportation. Wants are things that you would like to have but don’t necessarily need, such as entertainment and vacations.

- Make adjustments. Once you have a good understanding of your income, expenses, needs, and wants, you can start to make adjustments to your spending. Look for areas where you can cut back on your expenses, such as eating out less or canceling unnecessary subscriptions. If you’re struggling, consider downsizing your home or taking on a roommate.

- Set financial goals. Having financial goals can help you stay motivated to stick to your budget. Some examples of financial goals include saving for a down payment on a house, paying off debt, or retiring early.

Creating a post-divorce budget can be challenging, but it’s essential for getting your finances back on track. By following these tips, you can create a budget that works for you and your new financial situation.

Managing Joint Debts and Assets

Divorce not only severs emotional ties but also necessitates a division of shared finances. Managing joint debts and assets is crucial to ensure a fair and clean financial break. Here’s how to navigate this complex aspect:

1. Create a Comprehensive Inventory

Start by listing all assets acquired during the marriage, including:

- Real estate

- Vehicles

- Bank accounts (checking, savings, money market)

- Retirement funds

- Investments (stocks, bonds, mutual funds)

- Personal property of significant value

Simultaneously, detail all joint debts:

- Mortgages

- Car loans

- Credit card balances

- Personal loans

2. Determine Ownership and Responsibility

Distinguish between assets and debts classified as “joint” (owned or owed by both parties) and “separate” (owned or owed by one party before the marriage or received as inheritance/gift during the marriage). State laws regarding property division, whether “community property” or “equitable distribution,” will significantly influence this determination.

3. Negotiate a Fair Settlement

This step often involves negotiation, mediation, or legal intervention. Strive for an agreement that feels equitable to both parties. This might involve:

- Selling assets and dividing proceeds

- One party refinancing debts in their name only

- Transferring ownership of assets to offset debt responsibility

4. Update Legal Documents

Once an agreement is reached, formalize it in the divorce decree. Ensure that ownership of assets is legally transferred and financial accounts are separated. Close all joint accounts to prevent future liabilities and open new individual accounts.

5. Address Credit Report Impact

Even if a divorce decree dictates one party’s responsibility for a debt, creditors may still hold both parties accountable. Obtain individual credit reports after the divorce is finalized and take necessary steps to establish independent creditworthiness.

Building an Emergency Fund

After a divorce, having a financial safety net is more important than ever. An emergency fund can provide a much-needed cushion during times of unexpected expenses or financial instability. Here’s how to start building yours:

1. Determine Your Emergency Fund Goal

Ideally, you should aim to have three to six months’ worth of living expenses saved. However, starting with a smaller goal, such as $1,000, can give you a sense of accomplishment and motivate you to keep going.

2. Create a Budget

To free up money for your emergency fund, track your income and expenses to identify areas where you can cut back. Look for non-essential spending that you can reduce or eliminate.

3. Automate Your Savings

Set up automatic transfers from your checking account to your savings account each month. This “pay yourself first” approach ensures consistent contributions to your emergency fund.

4. Explore Additional Income Sources

If possible, consider taking on a side hustle or freelancing to supplement your income. Any extra money you earn can be directed toward your emergency fund.

5. Choose the Right Account

While a traditional savings account is a good option for an emergency fund, consider a high-yield savings account or money market account to earn more interest on your savings.

6. Make it a Priority

Remember, building an emergency fund is crucial for your financial well-being after a divorce. Make it a priority and stay committed to your savings goals.

Finding New Income Sources

Divorce often leads to significant financial changes, especially if you were previously financially dependent on your spouse. Finding new income sources is crucial to rebuilding your financial stability.

Here are some avenues to explore:

- Re-entering the workforce: If you took time off to raise a family, consider updating your resume and brushing up on your skills. Network with contacts, attend job fairs, and explore online job boards.

- Turning hobbies into income: Do you have a passion for crafting, writing, or photography? Explore ways to monetize your hobbies through online platforms, local markets, or freelance work.

- Freelancing and gig work: The gig economy offers numerous opportunities to earn income on a flexible schedule. Consider freelance writing, virtual assisting, driving for a ride-sharing service, or delivering food.

- Downsizing and selling assets: Selling a larger home or other valuable possessions can provide a significant influx of cash that you can use to cover expenses while you rebuild your income.

- Seeking financial assistance: Explore government programs or community resources that provide financial assistance or job training programs for individuals in your situation.

Planning for Financial Independence

Divorce often brings significant financial changes. Establishing your financial independence is crucial for moving forward with confidence. Here’s how to start planning:

1. Budget and Track Expenses

Understanding your income and expenses is the foundation of financial planning. Create a detailed budget that tracks all sources of income and every expense. This will give you a clear picture of your financial standing and help identify areas where you can save.

2. Emergency Fund

Having 3-6 months’ worth of living expenses saved in an easily accessible account is crucial, especially after a divorce. This fund acts as a safety net in case of unexpected events like job loss or medical emergencies.

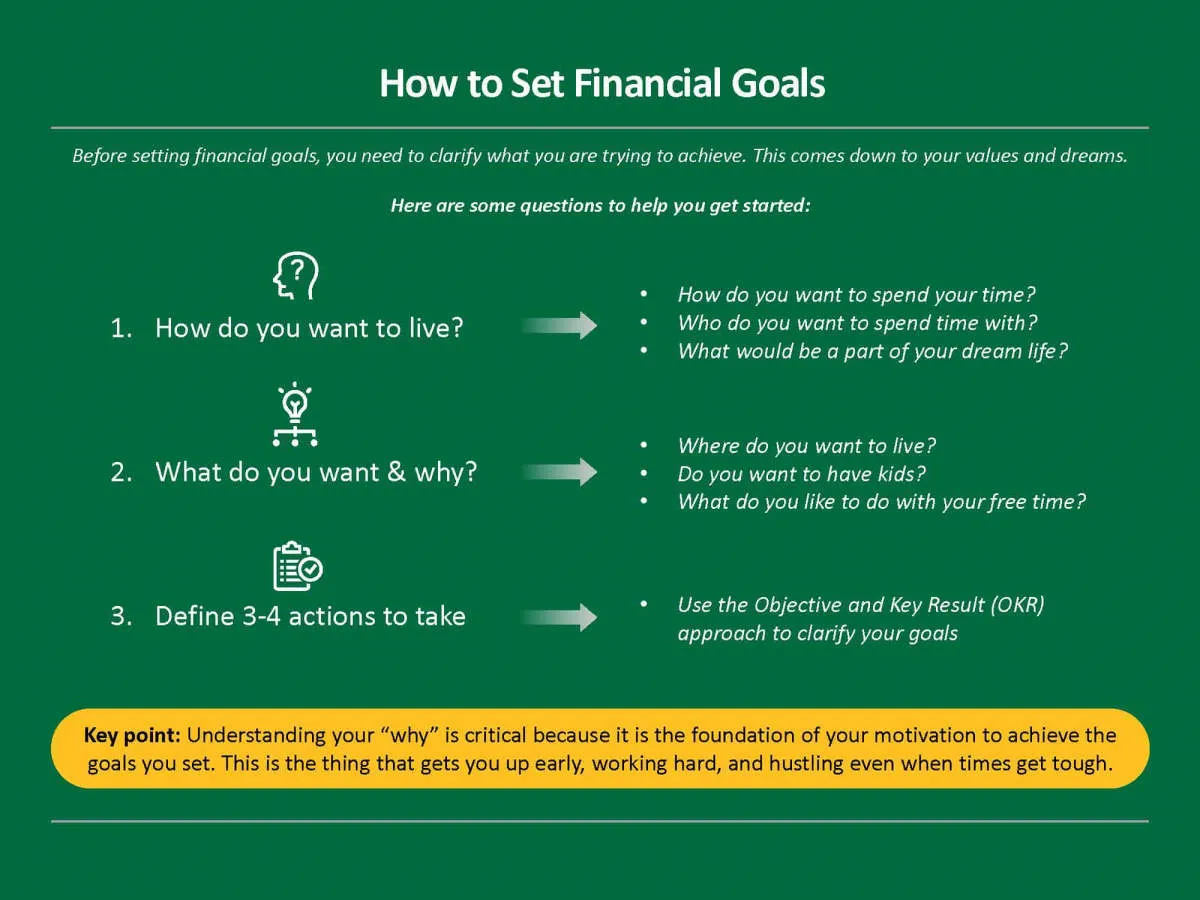

3. Review and Update Financial Goals

Life after divorce may require you to reassess and adjust your financial goals. Do you want to buy a house? Retire early? Save for your children’s education? Define your short-term and long-term goals to create a roadmap for your financial future.

4. Retirement Planning

Divorce can impact retirement savings. Review your current retirement plan and adjust contributions as needed. If you were financially dependent on your spouse, explore options like starting your own retirement account or increasing contributions to your existing one.

5. Seek Professional Guidance

Navigating finances post-divorce can be complex. Consider consulting with a financial advisor who can provide personalized guidance on budgeting, investing, and planning for your financial future. They can help you make informed decisions based on your individual circumstances.

Seeking Professional Help

Navigating the financial complexities of divorce can feel overwhelming. While this article provides helpful tips, it’s important to remember that every situation is unique. Seeking professional guidance from financial advisors, lawyers, and therapists can provide personalized support tailored to your specific needs.

Financial Advisors can assist with:

- Creating a post-divorce budget

- Managing investments and assets

- Planning for retirement

- Addressing any debt or tax implications

Lawyers can provide legal counsel on:

- Division of assets and debts

- Spousal and child support agreements

- Protecting your financial rights

Therapists can offer emotional support and guidance on:

- Coping with the emotional stress of divorce

- Communicating effectively with your ex-spouse

- Adjusting to your new financial situation

Remember, seeking professional help is a sign of strength, not weakness. It demonstrates your commitment to making sound financial decisions and building a secure future for yourself.

Adjusting Your Financial Goals

Divorce inevitably necessitates a significant financial shift. Whether you were previously a dual-income household or not, your financial landscape is forever changed. It’s time to reassess, redefine, and rebuild your financial future, and that starts with your goals.

Short-Term Adjustments:

- Establish a Budget: Understanding your new cash flow is paramount. Track your income and expenses diligently to create a realistic budget that reflects your current financial situation.

- Emergency Fund: Having 3-6 months’ worth of living expenses saved is crucial, especially now as you navigate this transition.

- Debt Management: Prioritize high-interest debts and explore options like consolidation or balance transfers to manage them effectively.

Long-Term Vision:

- Retirement Planning: Revisit your retirement goals and adjust your savings and investment strategies accordingly. Consider seeking advice from a financial advisor specializing in post-divorce planning.

- Homeownership: If owning a home is still a goal, reassess your budget and explore mortgage options for your new financial situation.

- Investing: Based on your risk tolerance and financial goals, revisit your investment portfolio and make any necessary adjustments.

Conclusion

After a divorce, managing finances is crucial. Create a new budget, update accounts, prioritize savings, and seek financial advice for a stable future.

{kind=link}