In this article, discover essential steps and strategies to build a robust financial foundation. From budgeting to saving and investing, learn how to secure your financial future effectively.

Importance of a Financial Foundation

Building a strong financial foundation is crucial for achieving financial stability, security, and overall well-being. It serves as the bedrock upon which you can pursue your financial goals, weather unexpected storms, and live a more fulfilling life.

Here are key reasons why a solid financial foundation is essential:

1. Reduced Financial Stress and Anxiety

Financial instability is a major source of stress and anxiety for many individuals. When you have a strong financial foundation, you gain peace of mind knowing that you have a plan in place to manage your money effectively. This reduces financial worries and allows you to focus on other important aspects of your life.

2. Increased Financial Security

Unexpected events, such as job loss, medical emergencies, or economic downturns, can have a significant impact on your finances. A solid financial foundation provides a safety net and helps you navigate these challenges with greater resilience. Emergency funds, insurance coverage, and diversified investments are key components of financial security.

3. Goal Attainment

Whether your goals involve buying a home, starting a business, or retiring comfortably, a strong financial foundation provides the means to pursue them. By managing your money wisely, saving diligently, and investing strategically, you can turn your aspirations into reality.

4. Greater Financial Freedom

Financial freedom is about having choices and options in life. When you are not burdened by debt and have a solid financial foundation, you have the flexibility to make decisions that align with your values and priorities. This might include pursuing a passion project, taking a career break, or traveling the world.

5. A Legacy for the Future

Building a strong financial foundation is not just about the present; it’s also about securing your future and potentially leaving a positive legacy for your loved ones. By making sound financial decisions today, you can create a brighter tomorrow for yourself and generations to come.

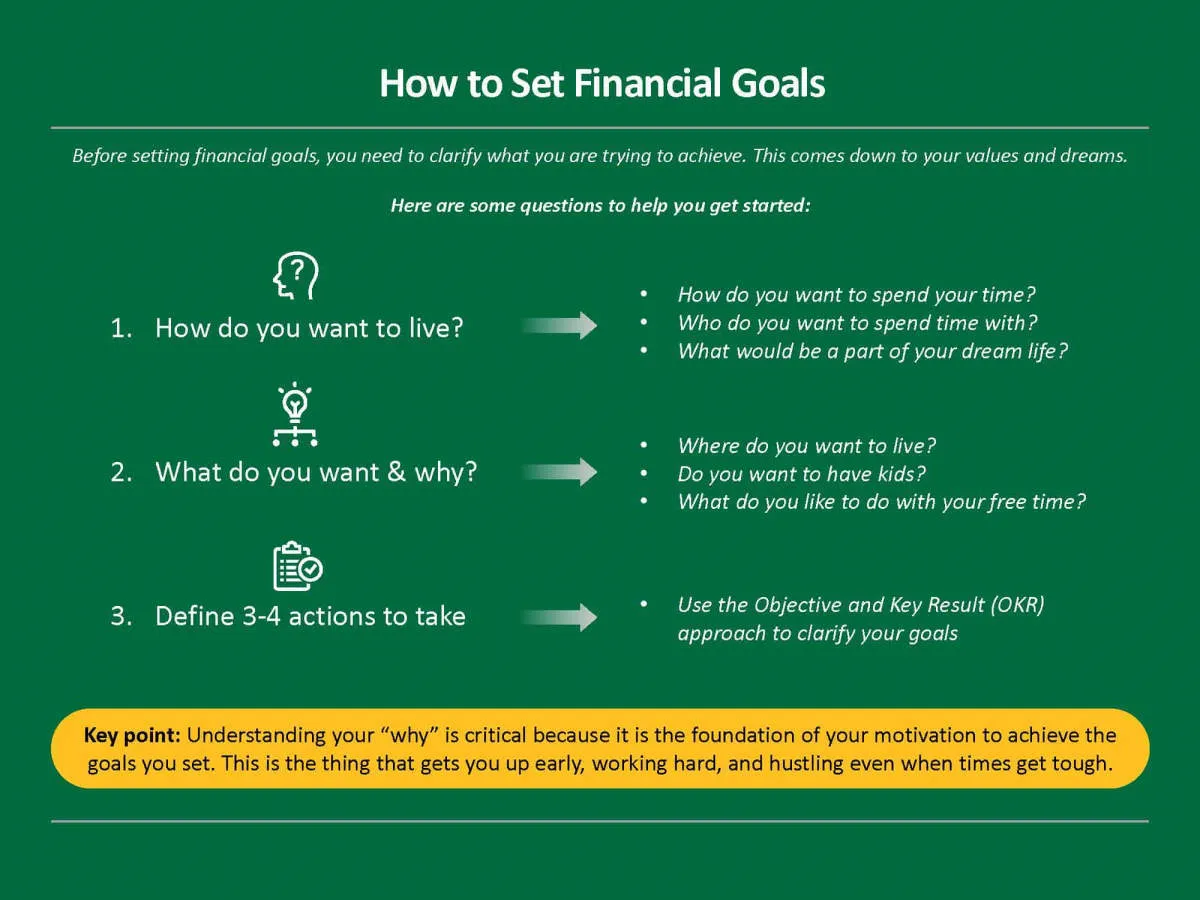

Setting Financial Goals

Building a strong financial foundation starts with knowing what you want to achieve with your money. Setting clear and specific financial goals gives you direction and motivation to manage your finances effectively.

Identify Your Goals: Think about what you want to accomplish financially in the short-term (within a year), mid-term (1-5 years), and long-term (5+ years). This could include anything from paying off debt and building an emergency fund to buying a home, investing for retirement, or funding your children’s education.

Make Your Goals SMART: Ensure your goals are:

- Specific: Clearly define what you want to achieve (e.g., “Save $5,000 for a down payment on a car”).

- Measurable: Quantify your goals so you can track your progress (e.g., “Save $500 per month”).

- Attainable: Set realistic goals that are achievable within your means.

- Relevant: Align your goals with your values and aspirations.

- Time-bound: Establish a timeframe for achieving each goal to create a sense of urgency.

Prioritize Your Goals: You may have multiple financial goals, so it’s essential to prioritize them based on their importance and urgency. This will help you allocate your resources effectively.

Write Down Your Goals: Putting your goals in writing makes them more concrete and helps you stay committed. Consider creating a visual representation of your goals, such as a vision board, to enhance motivation.

Regularly Review and Adjust: Life circumstances change, and so do financial situations. Review your goals periodically, at least annually, and make adjustments as needed to ensure they remain relevant and achievable.

Creating a Budget and Sticking to It

A budget is the cornerstone of strong financial management. It acts as a roadmap, guiding your income flow, tracking your expenses, and helping you achieve your financial goals. Here’s how to create a budget and, most importantly, how to stick to it:

1. Track Your Income and Expenses

Start by understanding where your money goes. Track every dollar you earn and spend for a month. You can use a spreadsheet, budgeting app, or simply a notebook. Categorize your spending (housing, food, transportation, etc.) for a clear picture.

2. Distinguish Between Needs and Wants

Analyze your spending habits. Differentiate between essential expenses (needs like rent, groceries, utilities) and discretionary spending (wants like entertainment, dining out, luxury items). This step is crucial for identifying areas where you can potentially cut back.

3. Set Realistic Financial Goals

What are your short-term and long-term financial aspirations? Saving for a down payment, paying off debt, investing – having clear goals will motivate you to budget effectively. Ensure your goals are specific, measurable, attainable, relevant, and time-bound (SMART).

4. Develop Your Budget

Using your income and expense tracking, allocate funds for different categories. Prioritize needs and allocate funds for your financial goals. Consider using the 50/30/20 rule as a guideline: 50% of your income for needs, 30% for wants, and 20% for savings and debt repayment. Adjust these percentages based on your individual circumstances and goals.

5. Find a Budgeting Method That Suits You

Numerous budgeting methods exist, each with a unique approach. Some popular options include the envelope system (allocating cash for different categories), zero-based budgeting (assigning every dollar a specific purpose), and the pay-yourself-first method (prioritizing savings and debt repayment). Experiment and find a method that aligns with your personality and financial habits.

6. Monitor and Adjust Regularly

Creating a budget is just the first step; consistent monitoring and adjustment are crucial for success. Track your progress against your budget regularly (weekly or monthly). Life is dynamic, and your income and expenses will fluctuate. Adjust your budget accordingly to stay on track.

7. Embrace Technology and Tools

Leverage budgeting apps and online tools to simplify the process. These tools can help you track expenses automatically, categorize spending, set financial goals, and receive personalized insights. Find a tool that suits your needs and integrates seamlessly with your lifestyle.

8. Practice Patience and Persistence

Mastering your finances is a journey, not a sprint. Be patient with yourself, embrace setbacks as learning experiences, and celebrate small victories along the way. Building a strong financial foundation requires ongoing effort, discipline, and a commitment to your financial well-being.

Building an Emergency Fund

A crucial pillar of a strong financial foundation is a well-stocked emergency fund. This fund acts as a financial safety net, providing you with a cushion to cover unexpected expenses without derailing your financial stability. Imagine facing a sudden job loss, medical emergency, or urgent car repairs – without an emergency fund, these situations could quickly spiral into debt and financial stress.

How Much Should You Save?

A common rule of thumb is to save three to six months’ worth of living expenses in your emergency fund. This means having enough money saved to cover your essential costs like rent/mortgage payments, utilities, groceries, and transportation for that duration.

Where to Keep Your Emergency Fund

Accessibility and security are paramount when choosing where to keep your emergency fund. A high-yield savings account or a money market account are excellent options. These accounts typically offer higher interest rates than traditional checking accounts while still allowing for easy access to your funds when needed.

Tips for Building Your Fund

- Start small: Even if you can only spare a small amount each month, it’s important to start somewhere. As you make progress, gradually increase your contributions.

- Automate your savings: Set up automatic transfers from your checking account to your emergency fund each month. This “set it and forget it” approach helps ensure consistent saving.

- Treat it as a non-negotiable expense: Just like you prioritize paying your rent or mortgage, make saving for your emergency fund a non-negotiable part of your budget.

- Replenish your fund after use: If you need to dip into your emergency fund, make a plan to replenish it as soon as possible.

Saving and Investing Wisely

Building a strong financial foundation goes hand-in-hand with smart saving and investing habits. These two practices, while distinct, work together to secure your financial future.

Saving: Your Financial Cushion

Saving involves setting aside a portion of your income regularly, typically in low-risk accounts like high-yield savings accounts or money market accounts. This forms your financial safety net, crucial for:

- Emergency Funds: Life is full of surprises, and not all of them are pleasant. A robust emergency fund (3-6 months of living expenses) cushions you from unexpected job loss, medical bills, or car repairs, preventing you from falling into debt.

- Short-Term Goals: Saving diligently helps you achieve short-term financial goals, such as buying a new car, going on a vacation, or making a down payment on a house.

Investing: Growing Your Wealth

Investing, on the other hand, focuses on growing your wealth over the long term. This involves putting your money into assets like stocks, bonds, or real estate, with the understanding that your investment will fluctuate but has the potential to generate returns higher than traditional savings accounts. Key aspects of investing include:

- Long-Term Growth: Investing aligns with goals like retirement planning or funding a child’s education, where your money has time to potentially grow significantly.

- Outpacing Inflation: Investing aims to outpace inflation, ensuring your money retains its purchasing power over time.

Aligning your saving and investing strategies with your financial goals, risk tolerance, and time horizon is essential. Consider seeking advice from a qualified financial advisor to create a personalized plan that puts you on a path to lasting financial well-being.

Managing Debt Effectively

Building a strong financial foundation requires careful management of debt. Debt, when used strategically, can be a tool for building wealth. However, mismanaged debt can quickly spiral out of control, leading to financial stress and instability. Here are key strategies for effective debt management:

1. Understand Your Debt

The first step to effectively managing debt is to understand what you owe. Create a list of all your debts, including credit cards, student loans, personal loans, and any other outstanding balances. Note down the interest rates, minimum monthly payments, and loan terms for each debt. This clear picture of your debt landscape will help you prioritize and strategize repayment.

2. Create a Budget and Track Your Spending

A detailed budget is crucial for effective debt management. Track your income and expenses to identify areas where you can cut back and allocate more money towards debt repayment. Look for non-essential spending that can be temporarily reduced or eliminated.

3. Prioritize Debt Repayment

Not all debt is created equal. Prioritize paying down high-interest debt, such as credit cards, first. Consider using the debt snowball or debt avalanche method to accelerate your repayment.

4. Negotiate with Creditors

Don’t hesitate to contact your creditors and explore options for lowering interest rates, negotiating lower monthly payments, or setting up a payment plan. They may be more willing to work with you than you realize, especially if you’re proactive and demonstrate a commitment to repayment.

5. Consider Debt Consolidation or Refinancing

If you have multiple debts with high interest rates, explore options like debt consolidation or refinancing. Consolidating your debts into a single loan with a lower interest rate can simplify payments and potentially save you money in the long run.

6. Build Emergency Savings

While focusing on debt repayment is crucial, it’s equally important to have an emergency fund. Having 3-6 months’ worth of living expenses saved can prevent you from going further into debt when unexpected expenses arise.

7. Seek Professional Guidance

If you’re struggling to manage your debt, don’t hesitate to seek help from a certified financial advisor. They can provide personalized advice, help you create a debt management plan, and offer support throughout your journey to financial stability.

Protecting Your Financial Future

Building a strong financial foundation isn’t just about saving and investing wisely, it’s also about safeguarding what you’ve worked hard to earn. Protecting your financial future means preparing for the unexpected and ensuring your assets are secure. Here’s how:

1. Insurance: Your Safety Net

Insurance is crucial for mitigating financial risks. Consider these key types:

- Health Insurance: Protects you from crippling medical expenses.

- Life Insurance: Provides financial support to your loved ones in your absence.

- Disability Insurance: Replaces a portion of your income if you’re unable to work due to illness or injury.

- Property Insurance (Home/Renters/Auto): Safeguards against damage, theft, or loss of your belongings and dwelling.

2. Emergency Fund: Your Financial Cushion

Life throws curveballs. An emergency fund, ideally with 3-6 months’ worth of living expenses, provides a buffer for:

- Job loss

- Unexpected medical bills

- Car repairs

- Home maintenance emergencies

3. Estate Planning: Securing Your Legacy

Planning for the future involves more than just finances while you’re here. Estate planning ensures your wishes are carried out and your assets are distributed according to your desires. Key elements include:

- Will: Outlines how you want your assets to be distributed.

- Trust: Manages and protects your assets, potentially reducing estate taxes.

- Healthcare Power of Attorney: Designates someone to make medical decisions if you’re unable to.

- Financial Power of Attorney: Appoints someone to manage your finances if you become incapacitated.

4. Cybersecurity: Protecting Your Digital Assets

In an increasingly digital world, safeguarding your financial information online is paramount:

- Strong Passwords: Use unique and complex passwords for all financial accounts.

- Two-Factor Authentication: Add an extra layer of security to prevent unauthorized access.

- Beware of Phishing Scams: Don’t click on suspicious links or provide personal information via email or phone.

- Regularly Monitor Accounts: Check for any unauthorized transactions and report them immediately.

Regularly Reviewing Your Finances

Building a strong financial foundation isn’t a “set it and forget it” endeavor. It requires consistent attention and adjustment along the way. That’s where regular financial reviews come in. Think of these reviews as financial “check-ups,” where you assess your progress, identify areas for improvement, and make necessary adjustments to stay on track.

How Often Should You Review?

The frequency of your reviews depends on your individual circumstances and comfort level. Some people benefit from monthly reviews, while others may find quarterly or even semi-annual reviews sufficient. The key is to find a cadence that keeps you engaged without feeling overwhelmed.

What to Review:

During each review, consider these key areas:

- Budget: Analyze your income and expenses. Are you sticking to your budget? Are there any areas where you’re overspending?

- Debt: Track your progress on paying down any debts. Are you making consistent payments? Can you explore options for consolidation or refinancing to lower interest rates?

- Savings: Evaluate your savings goals. Are you contributing enough to reach your targets? Are there opportunities to increase your savings rate?

- Investments: Review the performance of your investments and ensure they align with your risk tolerance and long-term goals. Do you need to rebalance your portfolio?

- Goals: Revisit your short-term and long-term financial goals. Have any of your priorities changed? Do your goals need adjusting based on your current financial situation?

Conclusion

Building a strong financial foundation is crucial for long-term stability and success. By emphasizing saving, budgeting, and investments, individuals can secure their financial future and achieve their goals.

{kind=link}