Learn how to transform your financial well-being in just one year with these practical tips and strategies. From budgeting and saving to investing and debt management, discover the steps you can take to achieve financial stability and success.

Setting Financial Health Goals

Improving your financial health starts with a clear roadmap. This means setting specific, measurable, achievable, relevant, and time-bound (SMART) financial goals. Instead of vaguely aiming to “save more,” define clear targets that will guide your journey.

Here’s a breakdown of setting effective financial goals:

1. Identify Your Priorities

What matters most to you financially? Do you want to:

- Build an emergency fund?

- Pay off debt (credit cards, student loans, etc.)?

- Save for a down payment on a house?

- Invest for retirement?

Prioritize your goals based on what’s most important to you right now. You might not be able to tackle everything at once, and that’s okay.

2. Set Realistic and Specific Goals

Instead of saying “I want to save more,” get specific. For example:

- “I will build a $5,000 emergency fund within the next six months.”

- “I will pay off $10,000 of credit card debt in the next year by making extra payments of $835 per month.”

3. Break Down Larger Goals

Large goals can feel overwhelming. Break them down into smaller, manageable milestones. If your goal is to save $20,000 for a down payment in two years, break it down to saving $835 per month. This makes your goal less daunting and helps you track progress.

4. Set a Timeline

Give yourself deadlines for achieving each goal. This creates a sense of urgency and helps you stay motivated.

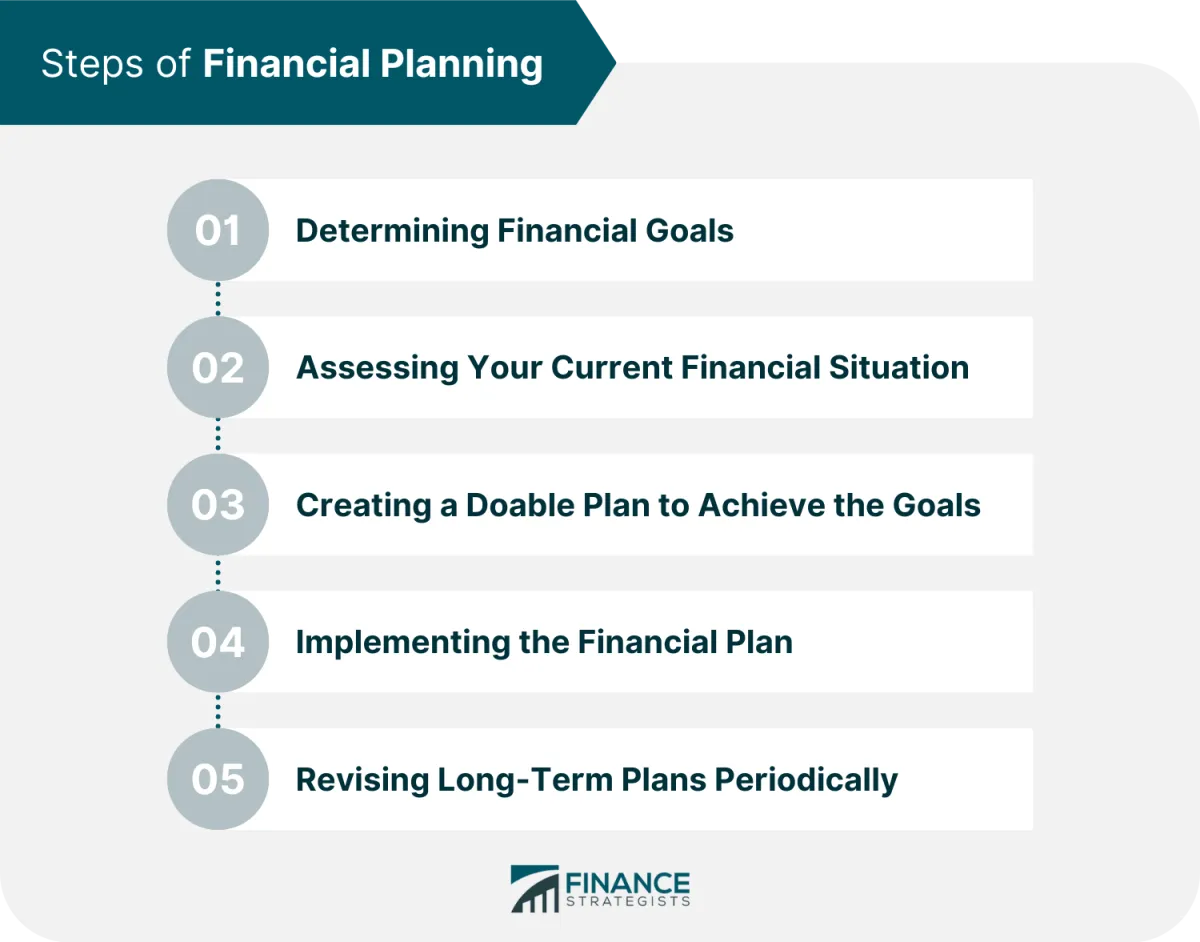

Creating a Financial Plan

A solid financial plan is the cornerstone of achieving your financial goals. It acts as a roadmap, guiding your financial decisions and helping you track your progress. Here’s how to create one:

1. Assess Your Current Financial Situation

Before you can plan for the future, you need to understand where you stand today.

- Track your income and expenses: Use a budgeting app, spreadsheet, or notebook to monitor your cash flow.

- Calculate your net worth: List your assets (what you own) and liabilities (what you owe). The difference is your net worth.

- Review your credit report: Understand your credit score and identify any areas for improvement.

2. Set SMART Financial Goals

Establish clear, specific financial goals to work towards. Use the SMART criteria:

- Specific: Define your goal clearly (e.g., “Save $5,000 for a down payment”).

- Measurable: Quantify your goal with numbers.

- Achievable: Set realistic goals you can reach.

- Relevant: Align your goals with your values and priorities.

- Time-bound: Set a deadline for achieving your goals.

3. Create a Budget

A budget is the foundation of your financial plan. It helps you allocate your income wisely and prioritize your spending.

- Track your income: Include all sources of income.

- Categorize your expenses: Identify fixed (rent, utilities) and variable (groceries, entertainment) expenses.

- Identify areas to reduce spending: Look for opportunities to cut back without sacrificing your well-being.

- Allocate funds to savings and debt repayment: Prioritize these essential financial goals.

4. Build an Emergency Fund

An emergency fund provides a financial safety net for unexpected events like job loss or medical bills.

- Aim for 3-6 months of living expenses: This amount will vary depending on your individual circumstances.

- Set up a separate savings account: Avoid dipping into these funds for non-emergency expenses.

5. Manage Debt Effectively

High debt levels can hinder your financial progress. Create a debt management plan:

- List all your debts: Include interest rates and minimum payments.

- Prioritize high-interest debt: Focus on paying down debts with the highest interest rates first.

- Consider debt consolidation or balance transfer options: Explore strategies to potentially lower interest rates.

6. Plan for the Future

Your financial plan should also address long-term goals like retirement and investments:

- Retirement planning: Start saving for retirement early to maximize compound interest.

- Investing: Consider investing to grow your wealth over time. Seek professional advice if needed.

- Estate planning: Create a will and consider other estate planning documents to protect your assets and loved ones.

Budgeting for Success

Creating and sticking to a budget is the cornerstone of financial health. It’s the roadmap that guides your income towards your financial goals, helps you control spending, and avoid debt.

Track Your Income and Expenses

Begin by understanding where your money goes. Track all income sources and every expense for a month. You can use budgeting apps, spreadsheets, or a notebook – choose a method that works best for you.

Categorize and Analyze Spending

Divide your spending into categories like housing, transportation, food, entertainment, etc. Analyze each category to identify areas of overspending or potential savings.

Set Realistic Financial Goals

Define your short-term and long-term financial goals. Do you want to save for a down payment, pay off debt, or invest? Having clear objectives will help you stay motivated and prioritize your spending.

Create a Budget That Works

Based on your income, expenses, and goals, create a realistic budget that allocates your money effectively. Popular budgeting methods include the 50/30/20 rule (50% needs, 30% wants, 20% savings) and the envelope system.

Monitor, Adjust, and Review

Budgeting isn’t a one-time task. Regularly monitor your spending, compare it to your budget, and make adjustments as needed. Life changes, and your budget should reflect those changes. Review your budget periodically to ensure it aligns with your evolving financial goals.

Saving and Investing Wisely

Saving and investing are essential aspects of achieving long-term financial health. By consistently putting money aside and investing it wisely, you can grow your wealth over time and work towards your financial goals.

Creating a Budget and Identifying Saving Opportunities

The first step towards effective saving is to create a budget. Track your income and expenses to understand where your money is going. Once you have a clear picture of your cash flow, you can identify areas where you can cut back on spending and free up more money to save.

Setting Financial Goals

Having clear financial goals can provide you with motivation and direction for your savings and investment strategies. Whether it’s saving for a down payment on a house, retirement, or your child’s education, identifying your goals will help you determine how much you need to save and what investment strategies are most appropriate.

Exploring Different Saving and Investment Options

There are numerous saving and investment options available, each with its own risk and return characteristics. Some common options include:

- High-yield savings accounts: These accounts offer higher interest rates than traditional savings accounts, allowing your money to grow faster.

- Certificates of deposit (CDs): CDs offer fixed interest rates for a set period, providing predictable returns.

- Money market accounts: These accounts offer variable interest rates and check-writing privileges, making them a flexible option.

- Stocks: Stocks represent ownership in publicly traded companies and offer the potential for high returns, but also come with higher risk.

- Bonds: Bonds are debt securities that represent loans to governments or corporations. They generally offer lower returns than stocks but are considered less risky.

- Mutual funds and exchange-traded funds (ETFs): These are investment vehicles that pool money from multiple investors to invest in a diversified portfolio of assets.

It’s essential to research and carefully consider the risks and potential returns associated with each option before making any investment decisions.

Start Small and Be Consistent

You don’t need a large sum of money to start saving and investing. Even small, consistent contributions can add up significantly over time thanks to the power of compounding. By automating your savings and investment contributions, you can make the process effortless and ensure that you’re regularly working towards your financial goals.

Reducing and Managing Debt

Debt can be a major source of stress and can make it difficult to reach your financial goals. The good news is that it’s possible to get your debt under control and improve your financial health. Here are some tips for reducing and managing debt:

Create a Budget

The first step to reducing debt is to understand where your money is going. Track your income and expenses for a month to see how much you’re spending and where you can cut back.

Create a Debt Management Plan

Once you know how much you owe, create a plan for paying it off. This plan should include a timeline for paying off each debt and a strategy for making extra payments. There are a few different debt repayment strategies you can use, such as the debt snowball method (focusing on paying off the smallest debts first) or the debt avalanche method (focusing on paying off the debts with the highest interest rates first).

Negotiate with Creditors

If you’re struggling to make payments, contact your creditors and try to negotiate a lower interest rate or a more manageable payment plan.

Look for Ways to Increase Your Income

The more money you earn, the faster you can pay off your debt. Consider taking on a side hustle or finding a higher-paying job.

Avoid Taking on New Debt

While you’re working to pay off your existing debt, avoid taking on any new debt. This means no new credit cards, loans, or financing plans.

Building an Emergency Fund

An emergency fund is a critical component of strong financial health. It acts as a safety net, protecting you from going into debt when unexpected expenses arise – think job loss, medical bills, or car repairs.

How much should you save? Ideally, aim for 3-6 months’ worth of living expenses. This may seem daunting, but remember, it’s a marathon, not a sprint. Start small and gradually increase your savings over time.

Where should you keep it? Your emergency fund should be easily accessible. A high-yield savings account or money market account are good options, offering decent interest rates while keeping your money liquid.

Tips for building your emergency fund:

- Create a budget: Understanding your income and expenses is crucial to identify areas where you can cut back and save more.

- Automate your savings: Set up automatic transfers from your checking account to your emergency fund each month.

- Find extra income: Consider a side hustle or selling unwanted items to boost your savings efforts.

- Make it a priority: Treat your emergency fund contributions like any other essential bill.

Monitoring Your Progress

Tracking your progress is crucial to staying motivated and making necessary adjustments along the way. It allows you to see how far you’ve come and identify areas that may require more attention.

Here are some tips for effectively monitoring your progress:

- Regularly review your budget and expenses. Compare your actual spending to your planned budget and see where you can make improvements.

- Track your net worth. This involves listing your assets (e.g., savings, investments, property) and subtracting your liabilities (e.g., debts, loans). Monitoring your net worth over time provides a comprehensive view of your financial health.

- Use financial tracking tools. Numerous apps and software programs can help you monitor your spending, track investments, and manage your budget effectively. Explore different options and choose tools that align with your needs and preferences.

- Set milestones and celebrate achievements. Breaking down your financial goals into smaller milestones makes them less daunting and allows you to celebrate your progress along the way. Reward yourself for reaching milestones, no matter how small, to stay motivated.

Adjusting Your Plan as Needed

While it’s great to have a financial plan set for the year, it’s important to remember that life happens! Don’t expect your initial budget or goals to be perfect. You might encounter unexpected expenses, changes in income, or shifts in your priorities.

Here’s how to adjust your plan as needed:

- Regularly Review: Set aside time each month to review your budget and track your progress towards your goals. Are you sticking to your spending limits? Are your goals still relevant?

- Identify Variations: Highlight any areas where you’re significantly off track. Is there a consistent category where you’re overspending? Did an unexpected event throw things off?

- Make Adjustments: Be flexible! Don’t be afraid to adjust your budget categories, savings targets, or even your overall financial goals. Life is unpredictable, and your plan should adapt with you.

- Celebrate Small Wins: Adjusting your plan doesn’t always mean things went wrong. You may find you’re ahead of schedule on a debt payoff or can increase your savings rate. Acknowledge and celebrate these victories!

Remember, financial health is a journey, not a destination. There will be detours and bumps along the way. By staying flexible and adapting your plan, you can stay on track towards a more secure financial future.

Conclusion

By following the strategies mentioned, you can significantly enhance your financial well-being within a year.