Learn the keys to achieving financial independence and early retirement through smart saving, investing, and lifestyle choices in our comprehensive guide.

Understanding Financial Independence

Financial independence is often touted as the key to a happy and fulfilling life, and for good reason. It represents the coveted state where you possess enough wealth to cover your living expenses indefinitely without relying on a traditional job or income source. In essence, it’s about having the freedom to choose how you spend your time and pursue your passions without being bound by financial constraints.

True financial independence goes beyond mere financial stability. While being financially stable implies being able to meet your current financial obligations comfortably, financial independence signifies a higher level of financial well-being. It means having the resources to maintain your desired lifestyle without the pressure of earning a paycheck. This typically involves building a substantial nest egg through savings, investments, and other wealth-building strategies.

The concept of financial independence is closely tied to the FIRE movement, which stands for “Financial Independence, Retire Early”. While early retirement is a common aspiration for those seeking financial independence, it’s not the sole objective. For many, it’s more about attaining the freedom to design a life on their terms, whether that involves pursuing a passion project, starting a business, traveling the world, or simply enjoying more leisure time.

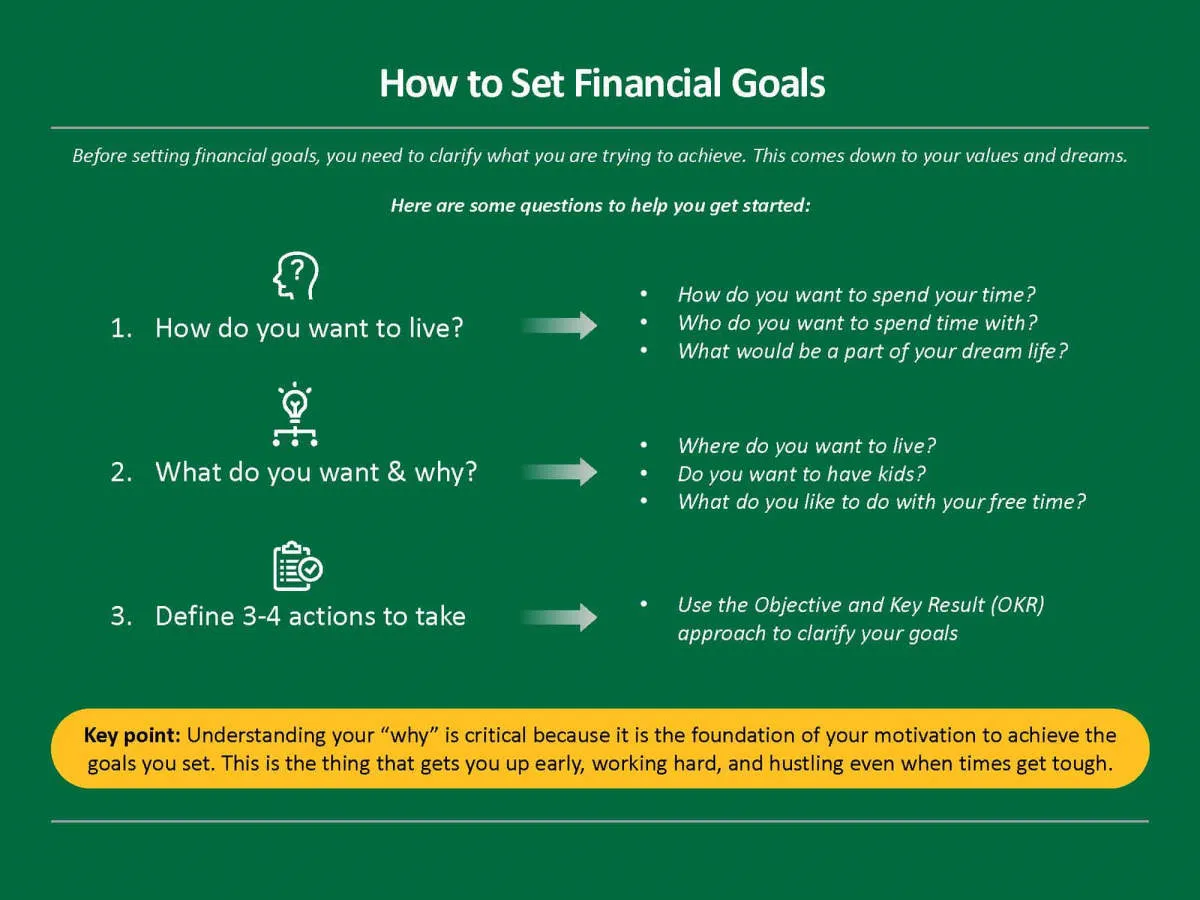

Setting Financial Goals

The journey to financial independence and early retirement begins with a clear roadmap. Setting concrete financial goals is the compass guiding you toward this destination. It’s not enough to simply desire wealth; you need to define what wealth means for you and establish a plan to achieve it.

Start by asking yourself crucial questions: What do you envision for your life after achieving financial independence? What age do you aim to retire at? What are your dream purchases or experiences? Quantify these aspirations with estimated costs. Having specific figures in mind transforms vague desires into tangible, achievable objectives.

Next, prioritize your financial goals. Separate short-term goals (achievable within a year), mid-term goals (one to five years), and long-term goals (five years and beyond). This segmentation allows for a structured approach to saving and investing. For instance, a short-term goal could be paying off credit card debt, while a long-term goal might be purchasing a rental property.

Remember to set SMART goals: Specific, Measurable, Achievable, Relevant, and Time-bound. This framework ensures your goals are well-defined and provide a clear path for tracking progress.

Creating a Savings Plan

Achieving financial independence and retiring early requires meticulous planning and unwavering commitment, especially when it comes to your finances. A robust savings plan is the bedrock of this endeavor. It’s not just about putting away whatever’s left at the end of the month; it’s about making a conscious decision to prioritize saving right from the start.

Here’s a breakdown of how to craft an effective savings plan:

1. Define Your Financial Goals

What does financial independence and early retirement look like for you? Do you dream of traveling the world, pursuing a passion project, or simply enjoying the freedom of not having to work? Defining your goals will provide clarity on how much you need to save and by when.

2. Determine Your Savings Rate

Your savings rate is the percentage of your income that you consistently set aside for savings. The higher your savings rate, the faster you can achieve your goals. Strive for a savings rate of at least 20%, but ideally aim for 50% or more if early retirement is your goal.

3. Automate Your Savings

Make saving automatic so you don’t even have to think about it. Set up regular transfers from your checking account to your savings account, ideally on your payday. This “pay yourself first” approach ensures that saving becomes a priority.

4. Explore Different Savings Vehicles

Don’t limit yourself to traditional savings accounts. Explore options like high-yield savings accounts, money market accounts, certificates of deposit (CDs), and index funds to maximize your returns. Each option comes with its own risk and reward profile, so choose what aligns best with your risk tolerance and time horizon.

5. Track Your Progress and Adjust Accordingly

Regularly monitor your savings progress and make adjustments as needed. Life is dynamic, and your financial goals may evolve over time. Stay adaptable and refine your savings plan to accommodate any changes in your circumstances or aspirations.

Investing for Long-Term Growth

Investing is the cornerstone of achieving financial independence and retiring early (FIRE). It’s about putting your money to work for you, generating returns that compound over time and build lasting wealth. When aiming for long-term growth, your focus shifts from short-term market fluctuations to strategies that deliver sustainable returns over decades. Here’s what to prioritize:

1. Embrace the Power of Compounding:

Compounding is the snowball effect of earning returns on your initial investments and the accumulated earnings from previous periods. The earlier you start and the longer you stay invested, the more powerful this effect becomes. Even small contributions made consistently can grow significantly over time thanks to the magic of compounding.

2. Diversify Your Portfolio:

Don’t put all your eggs in one basket. Diversifying across different asset classes – such as stocks, bonds, and real estate – helps to manage risk. When one asset class is down, another may be up, balancing out your portfolio and reducing volatility.

3. Think Index Funds and ETFs:

Index funds and Exchange-Traded Funds (ETFs) are excellent tools for long-term growth. They offer a low-cost way to passively track a specific market index, like the S&P 500. This strategy allows you to capture broad market returns without the complexities and fees associated with actively managed funds.

4. Invest in What You Understand:

While diversification is key, it’s also important to invest in what you understand. If you’re passionate about a particular industry or sector, research and consider investing in companies within that space. Having knowledge about your investments can make you a more informed and confident investor.

5. Take a Long-Term Perspective:

The market will have its ups and downs, but it’s essential to stay focused on the long game. Don’t panic sell during market corrections or try to time the market. Instead, ride out the fluctuations, knowing that your investments are strategically positioned for growth over the long haul.

Reducing Living Expenses

One of the most effective ways to accelerate your path to financial independence and early retirement is to reduce your living expenses. By spending less, you free up more cash flow to invest and grow your wealth. Here are some strategies to consider:

Housing

Housing often constitutes the largest portion of our monthly expenses. Consider these options for lowering costs:

- Downsize: Could you live comfortably in a smaller home or apartment? Downsizing can significantly reduce your rent or mortgage payments.

- Relocate: Explore moving to a more affordable city or town. The cost of living can vary greatly depending on location.

- Rent out a room: Taking in a roommate or utilizing a platform like Airbnb can provide an extra income stream to offset housing costs.

Transportation

After housing, transportation is another significant expense. Here are some cost-cutting strategies:

- Drive less: Explore alternatives like biking, walking, or using public transportation whenever feasible.

- Downsize your vehicle: Consider selling your car if you rarely use it or opt for a more fuel-efficient model.

- Explore carpooling: Check for carpool options for your commute or errands.

Food

Food expenses can quickly add up. Here are some tips for reducing this cost:

- Cook more meals at home: Eating out less frequently can lead to substantial savings.

- Plan your meals: Meal planning helps prevent impulse purchases and reduces food waste.

- Take advantage of grocery store deals: Utilize coupons, shop for sales, and consider buying in bulk for non-perishable items.

Entertainment

Entertainment is important, but there are ways to enjoy yourself without breaking the bank:

- Explore free or low-cost activities: Take advantage of parks, libraries, free concerts, and community events.

- Cut back on subscriptions: Evaluate your streaming services, magazine subscriptions, and other memberships – eliminate those you don’t use regularly.

- Set a budget: Allocate a specific amount for entertainment each month and track your spending.

Building Multiple Income Streams

One of the cornerstones of achieving financial independence and retiring early (FIRE) is creating multiple income streams. Relying solely on a single source of income can be risky, especially if that source is unstable or disappears unexpectedly. By diversifying your income, you create a safety net and accelerate your journey towards financial freedom.

Why are multiple income streams important for FIRE?

- Increased Income: More income streams obviously mean more money coming in, allowing you to save and invest at a faster rate.

- Financial Security: If one income stream dries up, you have others to fall back on, reducing your financial vulnerability.

- Faster Debt Repayment: Extra income can be channeled towards clearing high-interest debts, freeing up more money for saving and investing.

- Early Retirement Potential: With enough passive income streams, you could potentially replace your primary income and retire early.

Types of Income Streams:

Income streams can be categorized as active (requiring your direct involvement) or passive (generating income with minimal effort once set up). Here are some examples:

Active Income Streams:

- Freelancing: Offer your skills in writing, editing, graphic design, web development, or other areas.

- Consulting: Leverage your expertise to provide advice to businesses or individuals.

- Gig Economy Work: Platforms like Uber, Lyft, and TaskRabbit offer flexible ways to earn extra money.

- Teaching or Coaching: Share your knowledge and skills through online courses, workshops, or one-on-one coaching.

Passive Income Streams:

- Dividend Investing: Invest in dividend-paying stocks to receive regular payouts.

- Rental Income: Purchase and rent out real estate properties.

- Affiliate Marketing: Promote products or services on your website or social media and earn a commission on sales.

- Creating and Selling Digital Products: Develop and sell e-books, online courses, templates, or stock photos.

Remember, building multiple income streams takes time and effort. Start by identifying your skills and interests and exploring different options that align with your goals.

Planning for Early Retirement

Early retirement – the dream of leaving the workforce well before the traditional retirement age – requires meticulous planning. It’s not just about amassing wealth; it’s about strategically aligning your finances, lifestyle choices, and future goals.

1. Define Your Early Retirement Vision:

Start by painting a vivid picture of what “early retirement” means to you. What age do you envision yourself retiring at? How will you spend your days? Where do you see yourself living? This clarity will serve as your guiding light throughout the planning process.

2. Crunch the Numbers:

Early retirement demands a solid grasp of your financial landscape. Determine your retirement expenses, factoring in healthcare costs, potential travel plans, and any other anticipated expenses. Use retirement calculators to estimate how much you’ll need to accumulate to support your desired lifestyle.

3. Accelerate Savings and Investments:

Early retirement hinges on aggressive savings and smart investments. Explore high-yield savings accounts, index funds, and other investment vehicles that align with your risk tolerance. Consider increasing your savings rate gradually over time and explore opportunities for additional income streams.

4. Healthcare Considerations:

Healthcare is a significant factor in early retirement planning. Research your options for health insurance coverage before you leave your job, as you may need to bridge the gap until you qualify for Medicare or other government programs.

5. Develop a Withdrawal Strategy:

Create a plan for withdrawing funds from your savings in retirement. Determine a sustainable withdrawal rate that will ensure your money lasts throughout your golden years, considering factors like inflation and potential market fluctuations.

Staying Motivated and Focused

The journey to financial independence and early retirement (FIRE) is a marathon, not a sprint. It requires consistent effort and dedication over an extended period. Staying motivated and focused throughout this journey is crucial to achieving your goals. Here are some tips to help you stay on track:

1. Visualize Your Future

Create a clear vision of what financial independence and early retirement look like for you. Imagine the freedom, flexibility, and opportunities it will bring. Regularly visualize yourself living that life, as this will fuel your motivation and remind you why you started in the first place.

2. Set Realistic and Achievable Goals

Break down your big FIRE goal into smaller, more manageable milestones. Celebrate each milestone achieved, as this will provide a sense of progress and keep you motivated. Ensure these goals are realistic and achievable, as setting the bar too high can lead to discouragement.

3. Track Your Progress and Celebrate Milestones

Regularly monitor your finances, track your savings rate, and assess your progress toward your FIRE goals. Utilize budgeting apps or spreadsheets to visualize your journey and identify areas for improvement. Celebrating milestones, no matter how small, reinforces your commitment and provides a psychological boost.

4. Find Your Support System

Surround yourself with like-minded individuals who share similar goals. Connect with the FIRE community online or through local meetups. Sharing your journey with others who understand the challenges and rewards can provide invaluable support and motivation.

5. Focus on What You Can Control

It’s easy to get caught up in external factors like market fluctuations or economic downturns. Instead of stressing over things outside your control, focus on what you can control: your savings rate, investment strategy, and expenses. Maintaining this focus will help you stay grounded and consistent.

6. Practice Gratitude

Cultivating gratitude can significantly impact your overall well-being and motivation. Take time to appreciate your current situation, acknowledge your progress, and express gratitude for the resources you have. This positive mindset shift can help you stay focused and resilient during challenging times.

7. Embrace the Journey

Remember that the path to FIRE is not always linear. There will be setbacks, unexpected expenses, and moments of doubt. Embrace these challenges as opportunities for learning and growth. Focus on enjoying the journey and celebrating small victories along the way.

{kind=link}