Learn how young professionals can effectively manage their finances with these essential tips for financial planning. From budgeting strategies to investment options, empower yourself to build a secure financial future.

Importance of Early Financial Planning

As a young professional, you have the advantage of time on your side when it comes to financial planning. The earlier you start, the more time your money has to grow and the better positioned you’ll be to reach your long-term financial goals. Here’s why early financial planning is crucial:

1. Power of Compounding

Compounding is essentially earning interest on interest. When you start early, even small contributions to your savings or investments can grow significantly over time. The longer your money compounds, the more substantial your returns will be.

2. Goal Achievement

Whether it’s buying a home, traveling the world, or retiring comfortably, everyone has financial goals. Early planning helps you define those goals and create a roadmap for achieving them. By starting early, you give yourself more time to save and invest, making your aspirations more attainable.

3. Debt Management

Many young professionals graduate with student loan debt or other financial obligations. Early financial planning helps you manage existing debt effectively and avoid accumulating unnecessary debt in the future. By creating a budget and sticking to it, you can prioritize debt repayment and free up more financial resources for your goals.

4. Building a Solid Foundation

Establishing good financial habits early on sets the stage for a lifetime of financial well-being. Learning about budgeting, saving, investing, and managing debt in your younger years creates a strong foundation for making informed financial decisions throughout your life.

5. Handling Unexpected Events

Life is unpredictable, and unexpected expenses can arise at any time. Having a solid financial plan in place, including an emergency fund, provides a safety net to navigate unexpected events without derailing your long-term financial stability.

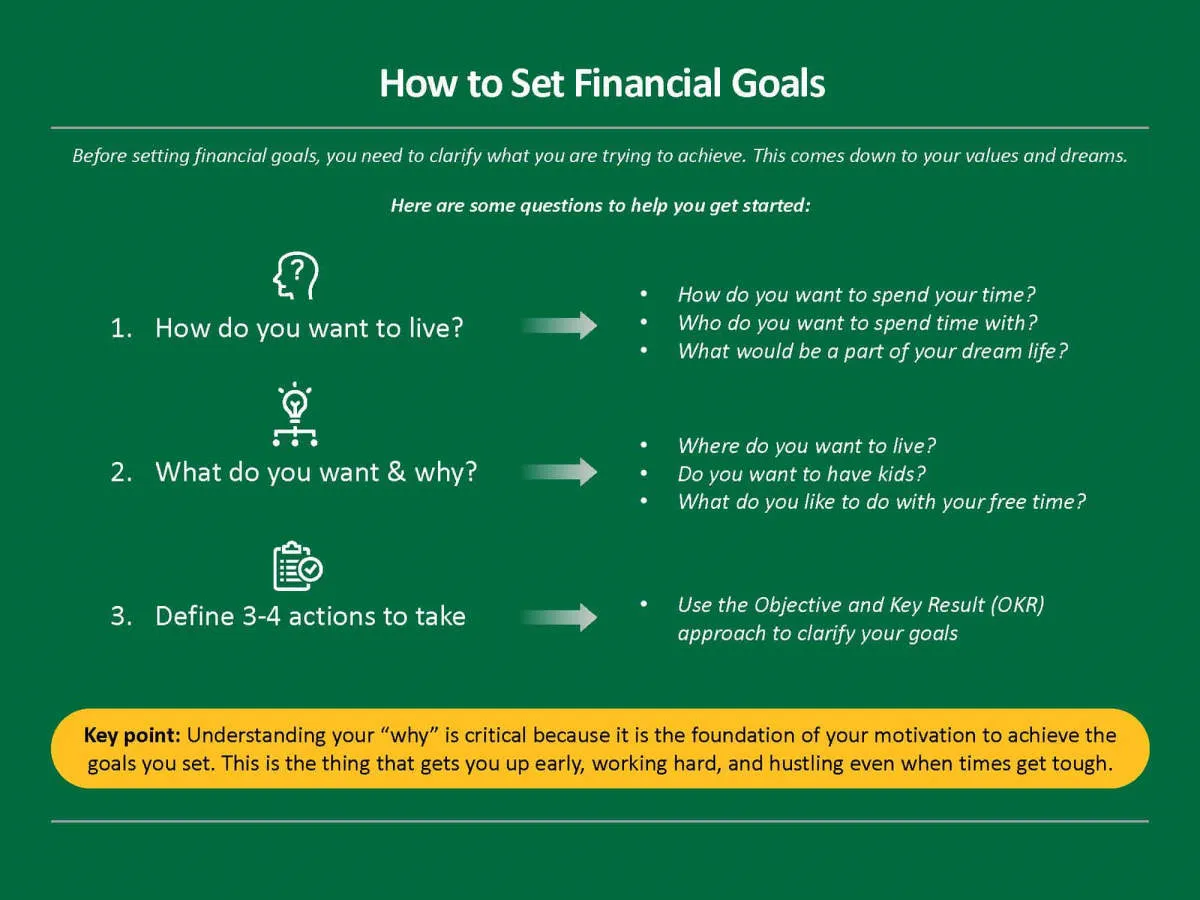

Setting Financial Goals

As a young professional, establishing clear financial goals is paramount to achieving financial stability and success. Goal setting provides a roadmap for your finances, helping you stay focused, motivated, and financially responsible.

Identify Your Short-Term and Long-Term Goals

Start by differentiating between short-term goals (achievable within a year) and long-term goals (taking several years or more).

- Short-term goals might include building an emergency fund, paying off credit card debt, or saving for a down payment on a car.

- Long-term goals could involve buying a house, investing in retirement, or achieving financial independence.

Make Your Goals SMART

To enhance your chances of success, ensure your financial goals adhere to the SMART criteria:

- Specific: Clearly define what you want to achieve. Instead of saying “save more,” specify “save $5,000 for a down payment.”

- Measurable: Quantify your goals so you can track your progress.

- Achievable: Set realistic and attainable goals based on your income and expenses.

- Relevant: Choose goals that align with your values and aspirations.

- Time-Bound: Establish deadlines for each goal to maintain focus and urgency.

Prioritize Your Goals

It’s crucial to prioritize your goals based on their importance and urgency. Determine which goals require immediate attention and allocate your resources accordingly. For example, paying off high-interest debt should take precedence over saving for a vacation.

Regularly Review and Adjust Your Goals

Life is dynamic, and your financial goals should evolve with your changing circumstances. Review your goals periodically, at least annually or whenever significant life events occur, such as a job change or marriage.

Creating a Budget and Sticking to It

Creating a budget is a fundamental step towards achieving your financial goals, and it’s crucial for young professionals just starting their careers. A budget serves as a roadmap for your money, helping you track your income and expenses, identify areas where you can save, and allocate funds towards your financial priorities.

Here’s a step-by-step guide to creating a budget:

-

Track Your Income and Expenses

Begin by listing all sources of income, including your salary, freelance work, or any other regular payments you receive. Next, track your expenses diligently. Utilize banking apps, spreadsheets, or budgeting tools to categorize and record every dollar you spend. This will provide a clear picture of your cash flow.

-

Distinguish Between Needs and Wants

Analyze your spending habits and differentiate between essential expenses (needs) and discretionary spending (wants). Needs include housing, utilities, groceries, and transportation. Wants encompass entertainment, dining out, and non-essential shopping. This distinction is vital for identifying areas where you can potentially reduce spending.

-

Set Realistic Financial Goals

Establish clear and achievable financial goals. Whether it’s saving for a down payment, paying off student loans, or investing for the future, having specific targets will keep you motivated and provide a sense of purpose for your budget.

-

Implement the 50/30/20 Rule (or Similar)

Consider using a budgeting framework like the 50/30/20 rule to allocate your income effectively. This rule suggests allocating 50% of your after-tax income to needs, 30% to wants, and 20% to savings and debt repayment. Adjust these percentages based on your individual circumstances and financial goals.

-

Automate Your Savings and Bill Payments

Leverage technology to automate your finances. Set up automatic transfers to your savings account each month. Schedule automatic bill payments to ensure you never miss a due date and avoid late fees. Automation simplifies money management and helps you stay consistent with your budget.

-

Review and Adjust Regularly

Your financial situation and goals may evolve over time. It’s essential to review your budget regularly, ideally monthly or quarterly. Make necessary adjustments based on changes in your income, expenses, or financial priorities. Flexibility is key to maintaining an effective budget.

Sticking to Your Budget

Creating a budget is the first step, but sticking to it requires discipline and consistency. Here are some tips to stay on track:

- Find a budgeting method that works for you: Experiment with different budgeting approaches, such as zero-based budgeting, envelope budgeting, or using budgeting apps, to find a system that aligns with your preferences and lifestyle.

- Track your spending regularly: Monitor your expenses closely to ensure you’re staying within your allocated budget limits. Utilize technology and budgeting tools to simplify the tracking process.

- Identify and avoid budget busters: Recognize spending patterns or habits that tend to derail your budget. Once you’ve identified these “budget busters,” find ways to minimize or eliminate them.

- Set financial goals and visualize your progress: Having clear financial objectives and visualizing your progress can be a powerful motivator. Regularly remind yourself of what you’re working towards.

- Celebrate small victories: Acknowledge and celebrate your budgeting successes, no matter how small. Rewarding yourself for staying on track can reinforce positive financial habits.

- Seek support and accountability: Share your financial goals with a trusted friend, family member, or financial advisor who can provide support and hold you accountable.

Saving for the Future

As a young professional, it’s easy to get caught up in the excitement of your first job and newfound financial independence. However, it’s crucial to prioritize saving for the future from the get-go. This might seem daunting, especially if you’re on a tight budget, but even small contributions can make a significant difference over time.

Why is saving so important?

Saving allows you to build a financial safety net for unexpected events like job loss or medical emergencies. It also provides financial security for future goals like buying a house, starting a family, or retiring comfortably. Remember, the earlier you start, the more time your money has to grow thanks to the power of compounding.

How to Start Saving:

- Create a budget: Track your income and expenses to understand where your money is going. Identify areas where you can cut back and redirect funds to savings.

- Set realistic goals: Determine what you’re saving for and how much you need. Having a clear objective makes it easier to stay motivated and track progress.

- Automate your savings: Set up automatic transfers from your checking to your savings account each month. Treat it like a non-negotiable bill.

- Explore different savings options: Look into high-yield savings accounts, money market accounts, and Certificates of Deposit (CDs) to maximize your returns.

- Start small and be consistent: Even if you can only save a small amount initially, the key is consistency. As your income grows, increase your savings rate gradually.

Investing in Your Career

As a young professional, your career is one of your most valuable assets. Investing in your career growth can lead to higher earning potential and greater job satisfaction in the long run. Here’s how:

1. Skill Development:

Continuously update your skills and knowledge. This could involve taking courses, attending workshops, pursuing certifications, or simply staying informed about industry trends through reading and networking.

2. Mentorship and Networking:

Seek out mentors in your field or professionals you admire. Their guidance and advice can be invaluable for your career progression. Actively network within and outside your organization to build connections and stay informed about opportunities.

3. Seek Growth Opportunities:

Don’t shy away from taking on new challenges and responsibilities within your current role or seeking out promotions. Embrace opportunities that push you outside your comfort zone and allow you to develop new skills.

4. Negotiate Your Worth:

Don’t be afraid to negotiate your salary and benefits when starting a new job or during performance reviews. Research industry standards and articulate your value to potential and current employers.

5. Consider Side Hustles:

Exploring side hustles or freelance work can provide additional income streams and opportunities to develop new skills that could benefit your primary career path.

Managing Student Loans

Student loans are a reality for many young professionals. Navigating repayment strategically is crucial for long-term financial health. Here’s how:

1. Understand Your Loans:

Before you graduate, or even during your grace period, know exactly what you owe. Log in to your loan servicer’s website, identify each loan (interest rates, terms, etc.), and understand the repayment options available.

2. Consider Loan Consolidation or Refinancing:

If you have multiple loans, explore if consolidation or refinancing is beneficial. Consolidation combines multiple federal loans into one, potentially simplifying payments. Refinancing, often through a private lender, might get you a lower interest rate, especially if your credit score has improved.

3. Choose a Repayment Plan that Suits You:

Federal loans offer various repayment plans, including income-driven options. These adjust your monthly payments based on your income and family size. Explore all the options and choose the one that fits your budget and financial goals.

4. Automate Payments:

Set up automatic payments to avoid late fees and potential credit score damage. Many loan servicers offer a small interest rate reduction for enrolling in auto-pay.

5. Prioritize Extra Payments:

If possible, make more than your minimum monthly payment, even if it’s just a small amount. Target any extra payments towards the loan with the highest interest rate to save money in the long run.

6. Explore Loan Forgiveness and Repayment Assistance:

Research loan forgiveness programs, especially if you work in public service or certain professions. Some employers also offer student loan repayment assistance as an employee benefit.

7. Seek Professional Advice:

If you’re struggling with your student loan debt or need help exploring options, don’t hesitate to consult a financial advisor. They can provide personalized guidance based on your specific financial situation.

Building Good Credit

Building good credit is crucial for young professionals as it impacts various financial aspects of their lives. A good credit score can help secure favorable interest rates on loans, rent an apartment, and even land a job. Here’s how to start building good credit:

1. Get a Credit Card

One of the easiest ways to start building credit is to get a credit card and use it responsibly. Look for credit cards designed for young adults or those with limited credit history. Ensure to use the card for small purchases and pay off the balance in full and on time every month.

2. Become an Authorized User

If you’re unable to get a credit card on your own, consider becoming an authorized user on a parent’s or guardian’s account. This allows you to benefit from their good credit history and start building your own.

3. Pay Bills on Time

Timely bill payments play a vital role in building good credit. Set up reminders or automate payments to avoid late fees and negative marks on your credit report. This includes rent, utilities, phone bills, and any other recurring expenses.

4. Monitor Your Credit Report

Regularly monitoring your credit report helps you track your progress and identify any errors or discrepancies. You’re entitled to a free credit report from each of the three major credit bureaus (Equifax, Experian, and TransUnion) annually.

5. Maintain a Low Credit Utilization Ratio

Your credit utilization ratio is the amount of credit you’re using compared to your total available credit. Keeping this ratio low, ideally below 30%, demonstrates responsible credit management and positively impacts your credit score.

Seeking Financial Advice

As a young professional, you might feel overwhelmed with managing your finances and planning for the future. While many resources are available to guide you, seeking personalized advice from a financial advisor can be incredibly beneficial.

Benefits of Financial Advice:

- Personalized Plan: A financial advisor will work with you to create a customized plan based on your income, expenses, goals, and risk tolerance.

- Expert Knowledge: Advisors possess in-depth knowledge of investment strategies, retirement planning, tax optimization, and more. They can guide you through complex financial decisions.

- Objective Perspective: It’s easy to get emotionally attached to financial decisions. An advisor provides an unbiased perspective and helps you make rational choices.

- Time-Saving: Managing your finances can be time-consuming. An advisor frees up your time so you can focus on your career and personal life.

Finding the Right Advisor:

Look for a Certified Financial Planner (CFP) or a similar credential. Ask for referrals from friends, family, or colleagues. During initial consultations, discuss their fees, services, and experience working with young professionals.

Seeking professional financial advice is an investment in your future. A qualified advisor can provide invaluable guidance and help you achieve your financial goals with confidence.

Conclusion

In conclusion, young professionals can set a strong financial foundation by following these tips: budgeting wisely, saving consistently, investing early, and seeking financial advice. By starting early and being disciplined, they can achieve their long-term financial goals.

{kind=link}