Preparing for the arrival of a new baby involves more than just setting up a nursery. Learn how to create a solid financial plan to ensure a secure future for your little one.

Importance of Planning for a New Baby

Bringing a new baby into the world is a joyous occasion, but it also comes with significant financial responsibility. Planning ahead for the arrival of your little one is crucial to ensuring a secure and stable financial future for your growing family.

Reduced Financial Stress: Financial planning can alleviate much of the stress associated with the costs of having a baby. By creating a budget, building an emergency fund, and exploring cost-effective options for baby essentials, you can minimize financial worries and focus on enjoying this special time.

Meeting Your Baby’s Needs: Babies come with a long list of expenses, from diapers and formula to healthcare and childcare. Planning ahead allows you to anticipate these costs and allocate funds accordingly, ensuring you’re prepared to provide for your baby’s every need.

Securing Your Family’s Future: Financial planning for a new baby isn’t just about the short-term; it’s an investment in your family’s long-term well-being. By establishing a solid financial foundation, you’re taking important steps to secure your child’s future, whether it’s saving for college or providing for their future needs.

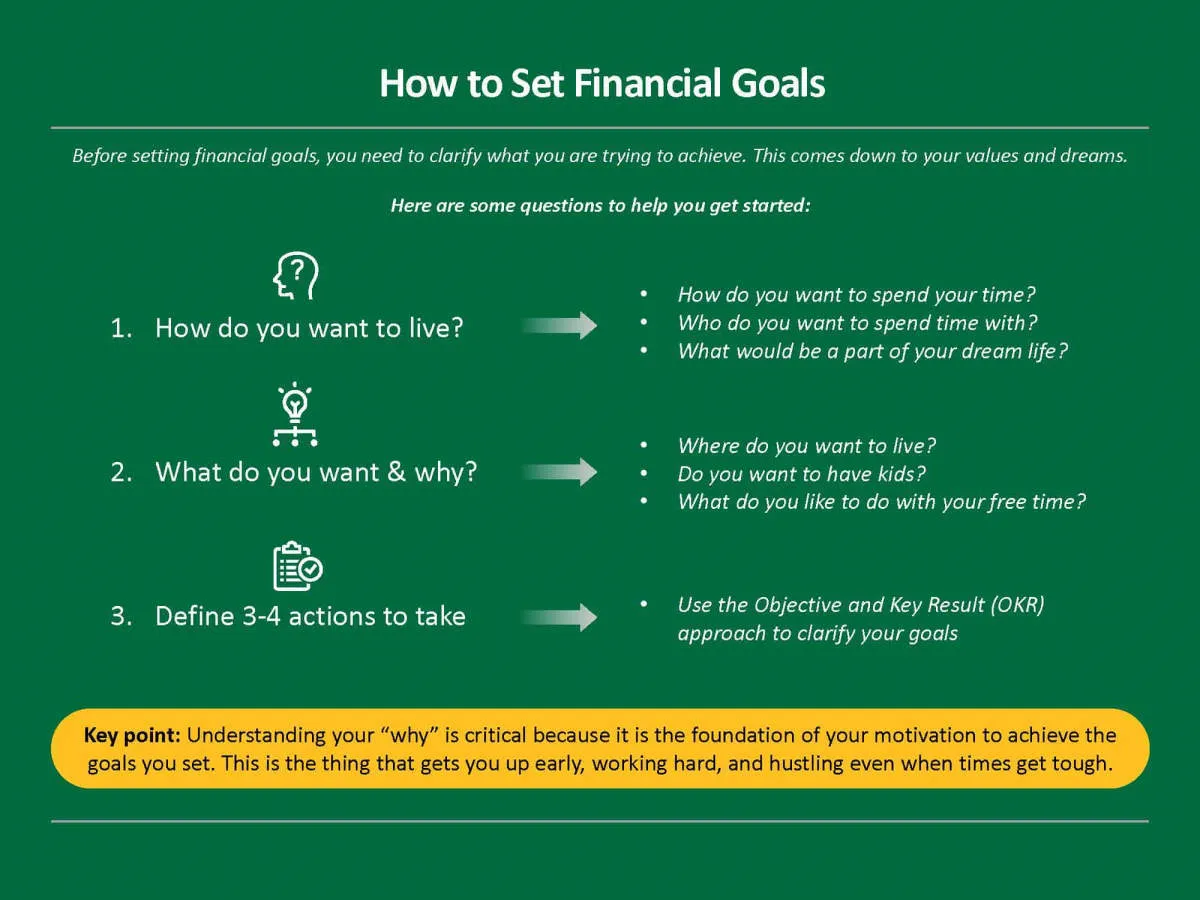

Setting Financial Goals

Welcoming a new baby is an exciting time, but it also comes with new financial responsibilities. Creating a solid financial plan will give you peace of mind and help secure your child’s future. Start by setting clear and achievable financial goals:

Short-Term Goals (0-2 Years)

- Build an Emergency Fund: Aim for 3-6 months’ worth of living expenses to cover unexpected costs like medical bills or job loss.

- Start a College Savings Plan: Even small contributions add up over time. Research options like 529 plans to maximize savings.

- Manage Day-to-Day Expenses: Create a realistic budget that accounts for the added costs of diapers, formula, and childcare.

Mid-Term Goals (2-5 Years)

- Review Life Insurance: Ensure you have adequate coverage for both parents to protect your family in case the unthinkable happens.

- Save for a Down Payment (Optional): If owning a larger home is a goal, start setting aside funds for a down payment.

- Plan for Childcare Costs: Research and budget for future childcare expenses, whether it’s daycare, a nanny, or another option.

Long-Term Goals (5+ Years)

- Continue College Savings: Regularly contribute to your child’s college fund to ease the financial burden when the time comes.

- Plan for Retirement: Don’t neglect your own financial future. Continue saving for retirement, even if it’s in smaller amounts initially.

- Estate Planning: Create or update your will to include your child and designate a guardian in case of an emergency.

Creating a Baby Budget

Welcoming a new baby into the world is a joyous occasion, but it also comes with new financial responsibilities. Creating a baby budget is crucial for managing these expenses and ensuring a financially secure future for your growing family.

1. Track Your Current Spending:

Before you can create a budget, you need to understand where your money is going. Track your spending for a few months to get a clear picture of your current financial situation.

2. Identify Essential Baby Expenses:

Make a list of all the essential expenses you’ll have for your baby, such as:

- Diapers and wipes

- Formula or breastfeeding supplies

- Clothes

- Crib, stroller, and car seat

- Healthcare

3. Estimate Monthly Costs:

Research the average costs of these essential items in your area and estimate how much you’ll need to budget each month.

4. Consider One-Time Expenses:

In addition to monthly expenses, factor in one-time costs like:

- Hospital bills

- Nursery furniture

- Baby monitor

5. Explore Potential Savings:

Look for ways to cut costs, such as buying used items, accepting hand-me-downs, or using cloth diapers.

6. Adjust Your Existing Budget:

Review your current budget and make adjustments to accommodate your new baby expenses. This may involve cutting back on discretionary spending or finding ways to increase your income.

7. Regularly Review and Adjust:

As your baby grows, their needs and expenses will change. Regularly review and adjust your budget to ensure it remains aligned with your evolving financial situation.

Saving for Baby Expenses

Having a baby is an exciting time, but it also comes with a significant financial responsibility. Creating a solid savings plan for those baby expenses is crucial to ensure you’re financially prepared for your little one’s arrival and beyond.

Start Early

The sooner you can start saving for baby expenses, the better. Even if you’re only able to put aside a small amount each month, it will add up over time. Consider setting up a dedicated savings account specifically for baby-related costs.

Estimate Expenses

Babies are expensive! Take some time to research and list out potential baby expenses. This will help you get a clearer picture of how much you’ll need to save. Some major expenses to consider include:

- Hospital Bills (even with insurance, out-of-pocket costs can be high)

- Prenatal Care

- Diapers and Wipes

- Formula or Breastfeeding Supplies

- Clothes

- Crib, Stroller, and Car Seat

Budget Adjustments

Look for areas in your current budget where you can cut back or make adjustments. Even small changes can free up extra money to put towards your baby savings goals.

Automate Savings

Make saving automatic! Set up recurring transfers from your checking account to your baby savings account. This will help ensure you consistently contribute to your savings goals without having to think about it.

Finding Ways to Cut Costs

Welcoming a new baby comes with a host of joys – and expenses. While you can’t put a price on those tiny smiles, you can certainly make smart financial choices to ease the burden. Here are some practical ways to cut costs as you prepare for your little one:

Baby Gear and Clothing

- Embrace hand-me-downs: Gently used baby clothes, toys, and gear are treasure troves of savings. Ask friends or family for hand-me-downs, or explore online marketplaces for great deals.

- Prioritize needs over wants: Focus on essential items like a crib, car seat, and stroller. You can always acquire other items as needed, preventing unnecessary purchases.

- Consider renting: For items with a short lifespan, like a bassinet or swing, consider renting instead of buying. This can save you significant money and storage space.

Feeding Your Baby

- Breastfeeding: If possible, breastfeeding is not only beneficial for your baby’s health but also the most budget-friendly option for feeding.

- Compare formula prices: If formula feeding is necessary, research and compare prices across different brands and stores. Look for coupons and loyalty programs to maximize savings.

Diapering Dilemmas

- Cloth diapering: While requiring an upfront investment, cloth diapering can lead to substantial savings in the long run.

- Bulk buying: Stock up on diapers during sales and promotions, ensuring you have a steady supply without paying a premium.

Planning for Childcare Expenses

One of the biggest expenses you’ll face as a new parent is childcare. The cost of childcare varies widely depending on where you live, the type of care you choose, and the age of your child.

Here are a few things to consider when planning for childcare expenses:

- Type of childcare. There are many different types of childcare available, including in-home care, daycare centers, and family childcare homes. Each type of care has its own costs and benefits.

- Location. Childcare costs can vary significantly from one city to the next. In general, childcare is more expensive in urban areas than in rural areas.

- Age of your child. Infant care is typically the most expensive type of childcare. As your child gets older, the cost of care will likely decrease.

- Your budget. It’s important to factor childcare costs into your budget before your baby arrives. If you’re on a tight budget, you may need to consider less expensive childcare options, such as family care or sharing a nanny with another family.

Start researching childcare options early on in your pregnancy. This will give you time to compare prices, tour facilities, and get on waiting lists. You can also start setting aside money each month to help cover the costs of childcare.

Building an Emergency Fund

The arrival of a new baby brings immense joy and, inevitably, added expenses. Diapers, formula, clothes – the costs add up quickly. That’s why establishing a solid emergency fund before your little one arrives is crucial.

An emergency fund acts as a financial safety net, offering peace of mind during unexpected events. These might include:

- Job loss

- Medical bills

- Unexpected home repairs

- Car troubles

How much should you save? Aim for 3-6 months’ worth of living expenses. This may seem daunting, but even small contributions add up over time. Consider setting up automatic transfers to your savings account each month to make saving easier.

Where should you keep your emergency fund? A high-yield savings account is generally the best option. It keeps your money safe and accessible while earning a little interest.

Reviewing and Adjusting Your Plan

Congratulations on your little bundle of joy! As your family grows, so do your financial needs and goals. That’s why it’s crucial to regularly review and adjust your financial plan to accommodate these changes. Here’s what you should consider:

1. Reassess Your Budget

With a new baby, your expenses will inevitably change. Track your spending for a few months to get a clear picture of where your money is going. Factor in new costs like diapers, formula or breastfeeding supplies, clothing, and childcare. Identify areas where you can cut back on existing expenses to make room for these new additions.

2. Review Your Emergency Fund

Life with a newborn can be unpredictable. Having a robust emergency fund is more critical than ever. Aim for at least 3-6 months’ worth of living expenses saved, taking into account potential new costs associated with your baby.

3. Evaluate Your Insurance Needs

Adequate insurance coverage is paramount with a new family member. Review your health, life, and disability insurance policies. Ensure your coverage is sufficient to protect your growing family’s financial well-being in case of unexpected events.

4. Adjust Your Savings Goals

A new baby might mean adjusting your short-term and long-term savings goals. If you’re planning for college, factor in rising education costs. Review your retirement savings plan and adjust contributions as needed. Even small adjustments can make a significant difference over time.

5. Seek Professional Advice

Navigating financial planning with a new baby can be overwhelming. Consider consulting with a financial advisor who specializes in family finances. They can provide personalized guidance tailored to your specific circumstances, helping you make informed decisions for your family’s financial future.

Remember, financial planning is an ongoing process, especially with a new baby in the picture. Regularly reviewing and adjusting your plan ensures it remains relevant to your evolving needs and goals.

Conclusion

Creating a solid financial plan for your new baby is essential for their future well-being. Start early, set clear goals, and prioritize saving and investing to secure their financial stability.

{kind=link}